Back on the 20th of March, with the economy reeling under the initial impact of COVID-19, the government announced it would ‘defer the 2020-21 Budget until 6 October 2020.’

Overview: An historic budget in prospect

Doing so, it said, would ‘provide more time for the economic and fiscal impacts of the coronavirus, both in Australia and around the world, to be better understood.’ Since then, the Treasurer has delivered a July 2020 Economic and Fiscal Update which provided a short-term take on developments and prospects and which sketched out some early estimates of the magnitude of the pandemic’s hit to the government accounts. Budget 2020-21 now offers the opportunity to go beyond that initial take to provide the government’s detailed and considered fiscal response to the pandemic. It should see Canberra set out a detailed plan for recovery while also presenting a first, best guess for the shape of the medium-term trajectory of the Australian economy in a post-pandemic world.

The Prime Minister has described next week’s budget as ‘arguably one of the most important, if not the most important since the end of the Second World War.’ He makes a fair point. Budget 2020-21 will deliver a huge, multi-billion-dollar deficit on a scale not seen since the end of that global conflict. July’s update predicted an underlying cash deficit of more than $184 billion for this financial year (see below) and it would not be a surprise if the revised estimate were to be around $200 billion, or even higher. That deficit will be accompanied by an expansion in the public debt burden as a share of GDP to levels we haven’t witnessed in Australia in much more than half a century.

This will be an historic budget in other ways too, taking place as it does against the backdrop of Australia’s first recession in almost three decades and its deepest downturn in the post-war period, and during a global slump worse than any suffered since the 1930s.

It will also be the first budget to be implemented under the government’s new fiscal strategy, which (at least temporarily) abandons the previous orthodoxy with its overriding focus on returning the budget to surplus and replaces that with an emphasis on restoring growth and employment. The new strategy also introduces a form of forward guidance that rules out significant fiscal tightening until there has been significant progress in lowering unemployment alongside a rather more relaxed attitude towards the impact of public debt. Much of this, of course, reflects the unavoidable consequences of the way that the pandemic has transformed the state of our public finances. But it also comes at a time when the near exhaustion of conventional monetary policy and the prevalence of extremely low interest rates have prompted much of the economics profession to rethink old orthodoxies around fiscal policy and debt sustainability.

Set in this context, the budget has to accomplish three main tasks.

Firstly, it needs to continue the government’s impressive work in supporting the economy and offsetting the large, negative demand shock that crushed economic activity and drove up unemployment earlier this year. Canberra has already deployed a huge amount of fiscal firepower to this end and has done so in creative ways, led by more than $100 billion of spending on the JobKeeper program and supported by the Boosting cash flow for employers measure and the Coronavirus Supplement to JobSeeker, among other policies (see below). But with a significant amount of existing financial support due to wind down as we move towards year-end and into Q1:2021 (exacerbated by the looming end of private mortgage and rent deferrals), more income support is going to be required to sustain the momentum of economic recovery. This is the immediate priority.

Secondly, as well as a profound demand shock, the pandemic also represents a major supply shock. COVID-19 has inflicted large-scale disruptions to national and international supply chains, while triggering dramatic relative shifts in performance and short- and longer-term prospects across industries, regions and individuals as the differential impact of adjustment to the pandemic has played out. Helping the economy adapt to these changes has to be part of any medium-term strategy intended to nurture the recovery beyond the initial impetus provided by Canberra’s fiscal largesse. That task is complicated by the fact that economic performance pre-COVID was fairly lacklustre, marked by disappointing productivity growth and low rates of (non-mining) business investment. A return to solid medium-term growth, therefore, requires a productivity repair job.

Thirdly, as already noted, there has been a serious shock to the nation’s public finances. Some of that shock is set to persist into the medium term, carried forward by lower tax receipts and a higher debt burden (see the PBO scenarios described below), albeit with the latter tempered by record-low interest rates and supportive monetary policy. The government’s new fiscal strategy correctly prioritises restoring growth over fiscal repair, but by getting the growth framework right and supporting higher levels of economic activity, the so-called ‘first phase’ of the fiscal strategy can have already made an important contribution to restoring fiscal health before Canberra’s mind turns to issues of debt stabilisation in the ‘second phase’.

The economic backdrop

At the time of the July 2020 Economic and Financial Update, the government was expecting GDP to suffer its largest quarterly fall on record in the June quarter of this year, predicting a seven per cent drop.

Activity was then expected to pick up in Q3, rising by 1.5 per cent, while for 2020 overall, real GDP was forecast to contract by 3.75 per cent in the largest annual decline in GDP on official record, before growing by 2.5 per cent in 2021.

When the Q2 GDP numbers were released on 2 September, they showed output falling seven per cent over the quarter, exactly in line with Treasury’s forecasts in the Update. The median estimates from the latest (September 2020) set of consensus forecasts see real GDP falling by 3.9 per cent this year, before growing by 2.7 per cent in 2021, numbers which are not too different from Treasury’s July projections.

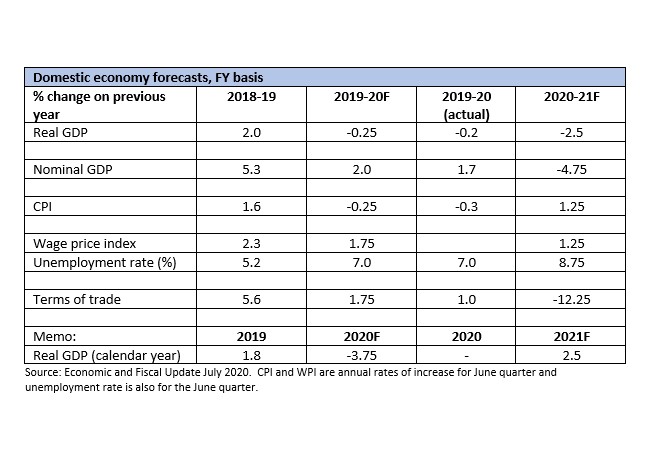

Source: Economic and Fiscal Update July 2020. CPI and WPI are annual rates of increase for June quarter and unemployment rate is also for the June quarter.

On a financial year (FY) basis, the Update said GDP growth would have contracted by 0.25 per cent in 2019-20 and output was then forecast to fall again by 2.5 per cent in 2020-21, in what would be the worst result since the 1940s. Sitting behind those numbers, lower net overseas migration was expected to contribute to a marked slowdown in population growth, down to 1.2 per cent in 2019-20 and to just 0.6 per cent in 2020-21, the weakest pace of growth since 1916-17. Nominal GDP growth – which is particularly important for the budget as it sets the size of the tax base – was predicted to grow by two per cent in 2019-20, before shrinking by 4.75 per cent in 2020-21.

Again, the actual outcome for 2019-20 was largely in line with expectations (perhaps not too surprising as by the time of the Update we already had data for three of the four quarters), with a 0.2 per cent fall in real GDP and a 1.7 per cent rise in nominal output.

After averaging seven per cent in the June quarter of 2020, the unemployment rate was expected to rise to a peak of around 9.25 per cent in the final quarter 2020 and be at 8.75 per cent in the June quarter of 2021. Here, there are some signs that the labour market may be doing better than expected, with the unemployment rate having fallen to 6.8 per cent as of August this year (although as we have noted in the Weekly, the payroll numbers have been telling a less positive story than the labour force survey results).

The fiscal starting point (1): payments, receipts, and deficits

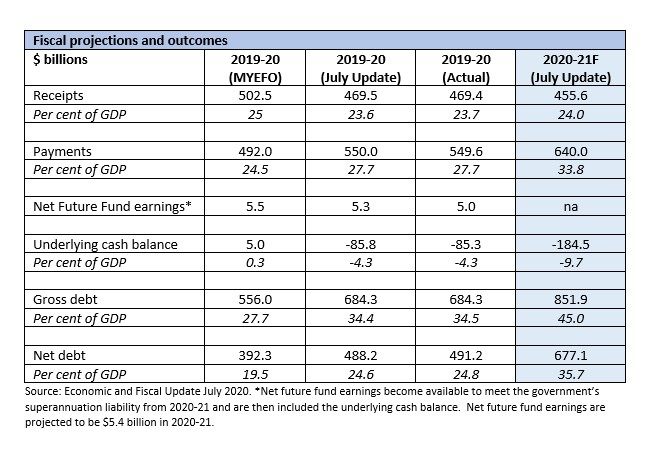

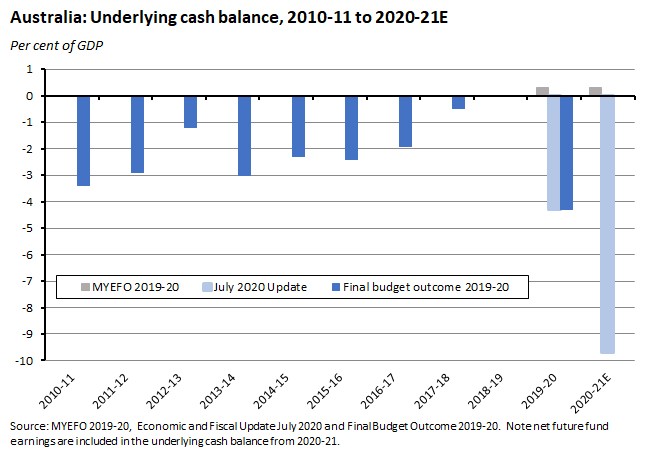

The July Economic and Fiscal Update also predicted an underlying cash balance in deficit to the tune of $85.8 billion (4.3 per cent of GDP) in 2019-20, with that deficit then expected to blow out to $184.5 billion (9.7 per cent of GDP) in 2020-2021.

Source: Economic and Fiscal Update July 2020. *Net future fund earnings become available to meet the government’s superannuation liability from 2020-21 and are then included the underlying cash balance. Net future fund earnings are projected to be $5.4 billion in 2020-21

The actual budget outcome for 2019-20 was in line with the Update’s assessment, returning a 4.3 per cent of GDP deficit. Back at the time of the 2019-20 MYEFO, the government was projecting an underlying cash balance in surplus to the tune of $5 billion (about 0.3 per cent of GDP) in 2019-20, and was expecting a similar outcome (a $6.1 billion surplus, again equivalent to about 0.3 per cent of GDP) in 2020-21. Instead, COVID-19 has pushed the fiscal accounts deep into the red with a $85.3 billion deficit in the underlying cash balance, representing a more than $90 billion deterioration relative to those earlier MYEFO projections.

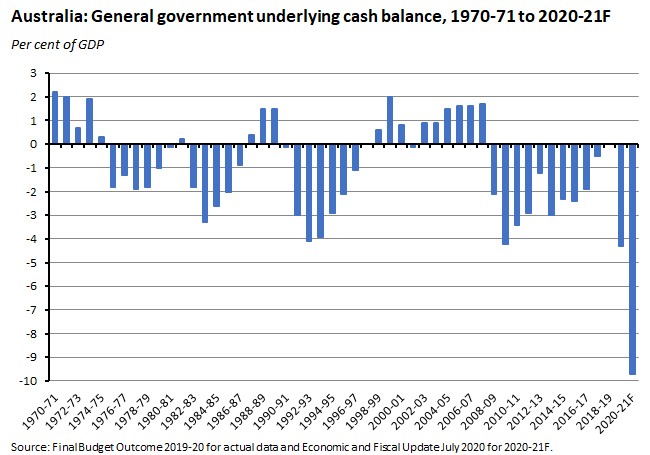

In relative terms, that means that the 2019-20 deficit was roughly the same size as the 4.2 per cent of GDP deficit that Australia ran in 2009-10 in the aftermath of the global financial crisis. But note that the Update’s projection for 2020-21 was for the deficit to more than double in size, dwarfing the scale of red ink seen in any year over the past half century and beyond, marking the biggest shortfall since 1945-46.

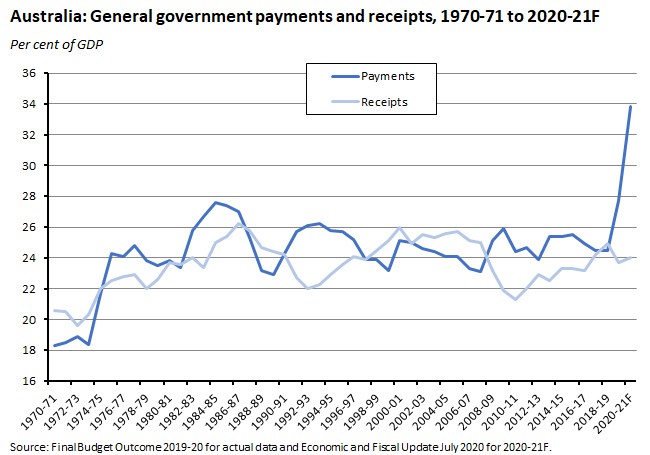

Those deficits in turn represent large increases in government payments and smaller – but still substantial – declines in receipts. In the FY just passed, government payments rose from 24.5 per cent of GDP in 2018-19 to 27.7 per cent of GDP in 2019-20. The Update assumed that they would rise further, to 33.8 per cent of GDP, in 2020-21. Receipts fell from 24.9 per cent of GDP in 2018-19 to 23.7 per cent in 2019-20, with the Update predicting a modest rise back to 24 per cent of GDP in the current FY.

The government’s COVID-19 economic support package

Those swings in receipts and payments reflect a combination of the operation of the so-called ‘automatic stabilisers’ (that is, falls in personal and company tax receipts and other government revenues as a result of lower economic activity and a parallel rise in payments such as unemployment benefits) operating alongside the active policy response to COVID-19 (initiatives such as the JobKeeper program). Most of the fall in receipts in FY2019-20 relative to the MYEFO’s projections has been due to the operation of the automatic stabilisers and other so-called parameter variations. In contrast, policy actions have driven the bulk of changes to payments.

At the time of the July Update, the government estimated that total planned expenditure on economic measures as part of its COVID-19 response package was $164.1 billion over the period 2019-20 to 2023-24 (before the additional $15.6 billion spend on JobKeeper discussed below). In addition, the government had also committed to spend a further $9.4 billion on health measures over the same period and had deployed $35 billion in balance sheet support, with the latter rising to $125 billion if the RBA’s term funding facility (or TFF) was included.

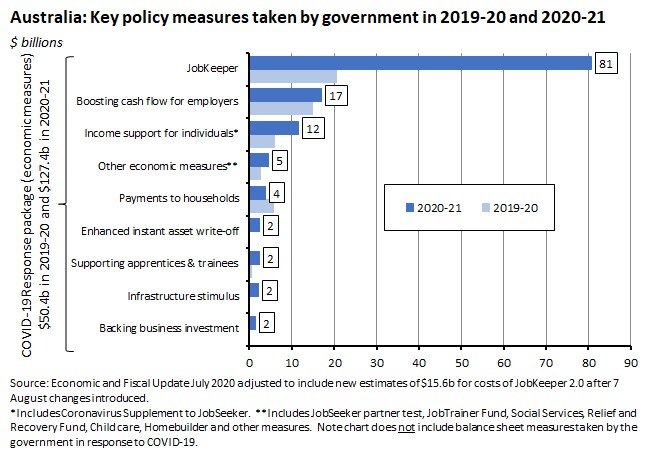

By design, the bulk of this policy support was concentrated in 2019-20 and 2020-21. As of July, of an estimated planned total expenditure of $164.1 billion on economic measures as part of the COVID-19 response package covering the period out to 2023-24, about 31 per cent ($50.4 billion) was spent in 2019-20 and a further 68 per cent ($111.8 billion) was scheduled to be spent during 2020-21. Add in the additional JobKeeper spending announced in August 2020, those figures rise to $177.9 billion in total economic support, with $50.4 billion spent in 2019-20 and a further $127.4 billion scheduled for 2020-21, mostly in the first half of the year.

As the chart above shows, the bulk of COVID-19 economic support to date is driven by three programs: JobKeeper, Boosting cash flow for employers, and Income support measures including the Coronavirus Supplement to JobSeeker. By far the biggest of these is the JobKeeper wage subsidy program. The original JobKeeper payment program ran from 30 March to 27 September and provided a government payment of $1,500 per fortnight per eligible employee for eligible businesses, with eligibility based on a turnover test. In July, the government announced changes to the program – JobKeeper 2.0 – that extended its life to 28 March 2021 but also made several significant adjustments that both reduced the generosity of the payments and tightened eligibility criteria.

The cost of JobKeeper 2.0 was initially put at an additional $16 billion, but the introduction of new public health restrictions in Victoria then prompted the government to tweak the criteria again in August to ease access to the program. As a result of these changes, plus the anticipated increase in demand for support, Treasury estimated that the new total cost of the JobKeeper program would rise by a further $15.6 billion (with $4.5 billion of that increase reflecting an increase in the number of Victorians joining the JobKeeper program and a further $11.1 billion associated with the changes to JobKeeper 2.0). That gives a new total cost for the program of $101.3 billion.

The second and final payment under the Boosting cash flow for employers program is scheduled for Q3:2020.

The original Coronavirus Supplement – an additional payment of $550 per fortnight to both existing and new recipients of Jobseeker Payment, Youth Allowance, Parenting Payment, Austudy, ABSTUDY Living Allowance, Farm Household Allowance and Special Benefit – was first paid on 27 April this year and ran until 24 September 2020. JobSeeker 2.0 then extended the payment period for the Coronavirus Supplement from 25 September 2020 to 31 December 2020, although the new supplement is now paid at a reduced rate of $250 per fortnight (the government also announced that it would increase the income free area for the JobSeeker Payment and Youth Allowance from $106 per fortnight for JobSeeker and $143 per fortnight for Youth Allowance to $300 per fortnight for both over the same period). The estimated cost of JobSeeker 2.0 is about $3.8 billion or around 0.2 per cent of GDP.

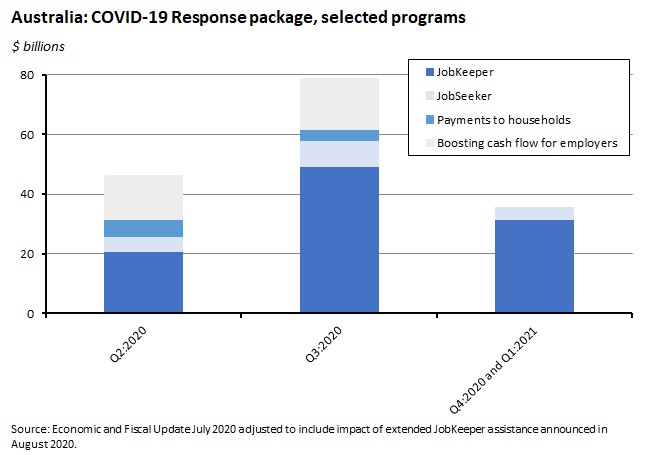

Importantly, the timing of these three initiatives means that, all else equal, there is a sharp decline in government economic support starting from the fourth quarter of 2020. One objective of the 2020-21 budget, therefore, should be to address this ‘fiscal hill’.

The fiscal starting point (2): debt and debt service

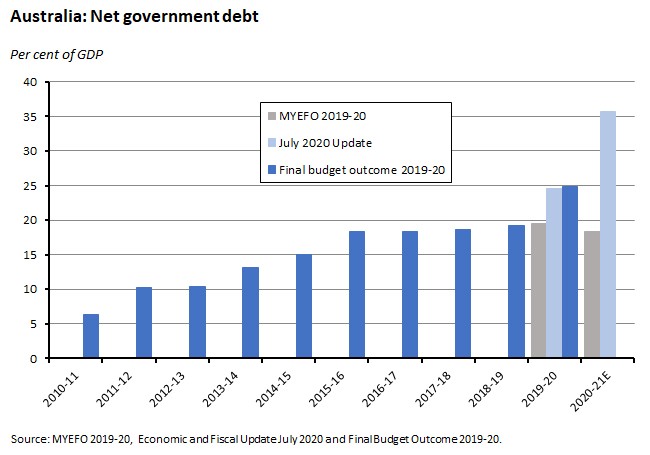

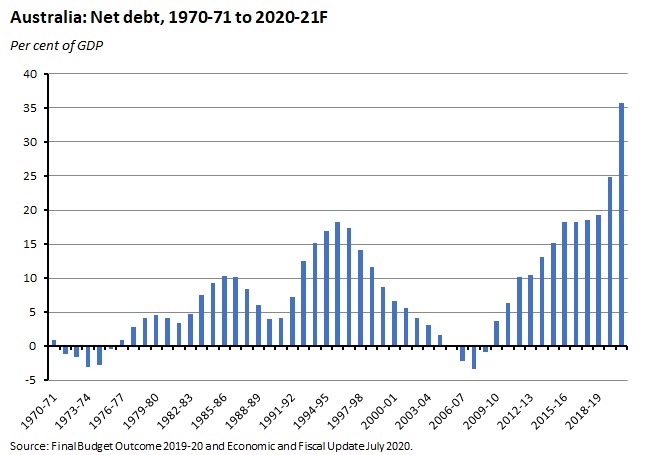

Unsurprisingly, the big jump in government deficits already underway has had significant implications for Australia’s public debt profile. By the end of 2019-20, general government net debt had risen to $491.2 billion (24.8 per cent of GDP) which was $98.9 billion more than had been estimated at the time of the 2019-20 MYEFO.

The July 2020 Economic and Fiscal Update predicted that the net debt burden would rise further to $677.1 billion (35.7 per cent of GDP) by the end of 2020-21, taking the debt ratio to its highest level in more than half a century. That’s approaching double the old MYEFO 2019-20 projections for a net debt to GDP ratio of just 18.5 per cent by end 2020-21.

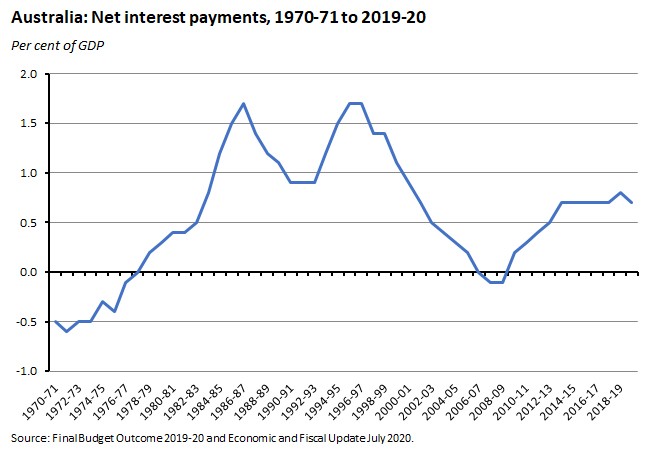

In this context, it’s important to note that a key silver lining for the public finances is the very low level of government borrowing costs that now prevails. This substantial decline in government bond yields – part a secular trend, part facilitated by the RBA’s new policy of yield curve control – means that despite the sharp increase in the stock of gross and net public debt, the burden of servicing that debt in terms of net interest payments has only risen modestly.

PBO medium-term projections

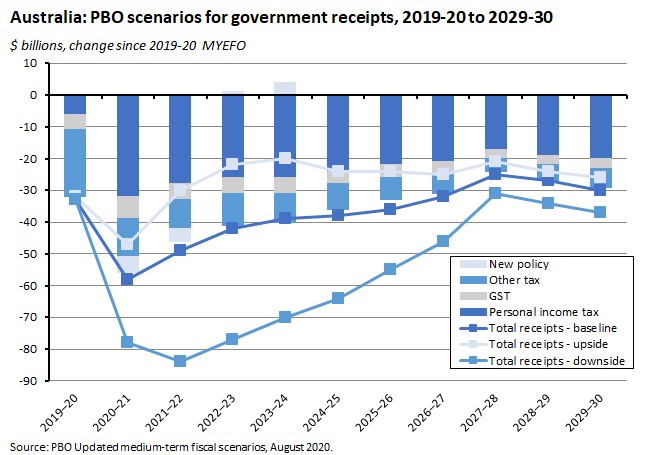

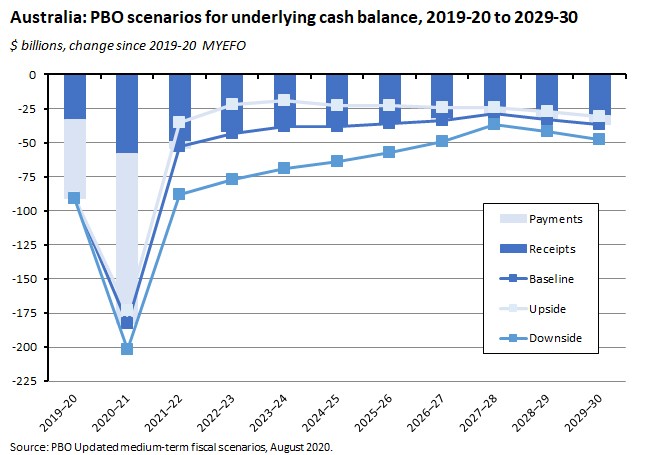

What about the longer-term implications of these changes? In late August this year, the Parliamentary Budget Office (PBO) produced updated medium-term fiscal scenarios designed to look at the impact of COVID-19 and the government policy response over the next decade. Drawing on the data presented in the July Update (and also including the $15.6 billion JobKeeper extension) and using the RBA’s August 2020 economic forecasts, the PBO constructed three scenarios based around a baseline with a gradual economic recovery, an upside scenario with a faster recovery and a downside scenario with a slower recovery. The PBO’s scenarios suggested that by 2029-30, government receipts could be between $26 billion and $37 billion lower than they would have been under the 2019-20 MYEFO assumptions. That reflects slower real GDP growth, a lower level of nominal GDP due to lower prices and wages, and a slower rate of population growth due to less net overseas migration, all of which contribute to the government’s tax base being lower than it otherwise would have been.

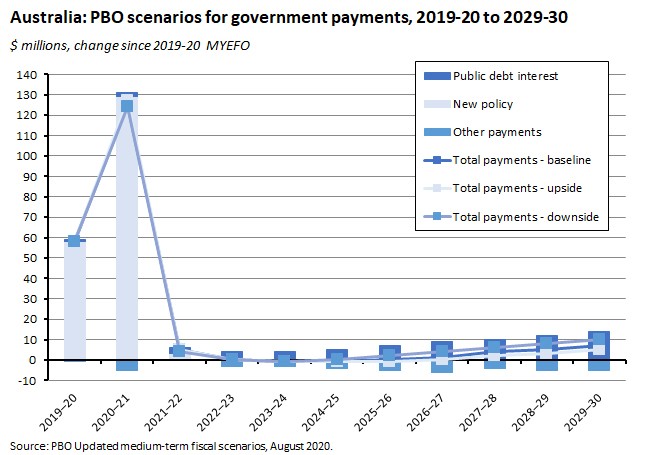

At the same time, the PBO projected that government payments would be between $5 billion and $10 billion higher in 2029-30 relative to the 2019-20 MYEFO. Initially, that reflects the impact of those big-spending government policy initiatives in 2019-20 and 2020-21. But subsequently, the deviation from the MYEFO is driven by higher public debt interest payments, due to an increased government debt stock as well as higher JobSeeker payments reflecting a larger number of unemployed Australians. (Note here that the PBO assumes that interest rates will return to their long run average over the medium term.).

The PBO calculated that the impact of these developments on the government’s underlying cash balance would be a deterioration of between $31 billion and $38 billion, relative to the MYEFO. Again, at first that reflects the higher payments associated with active government policy. But subsequently, the main driver is the impact of slower growth (including slower population growth) on government receipts.

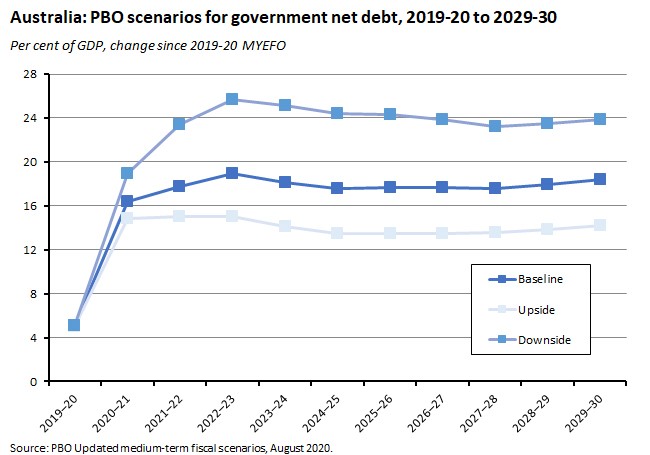

Finally, the PBO’s results suggested that the overall impact of the pandemic and the subsequent policy response could see Australian government net debt as a share of GDP in 2029-30 somewhere between 14 and 24 percentage points higher than it otherwise would have been.

Possible policy options Budget 2020-21, to bring forward phase 2 and 3 tax cuts

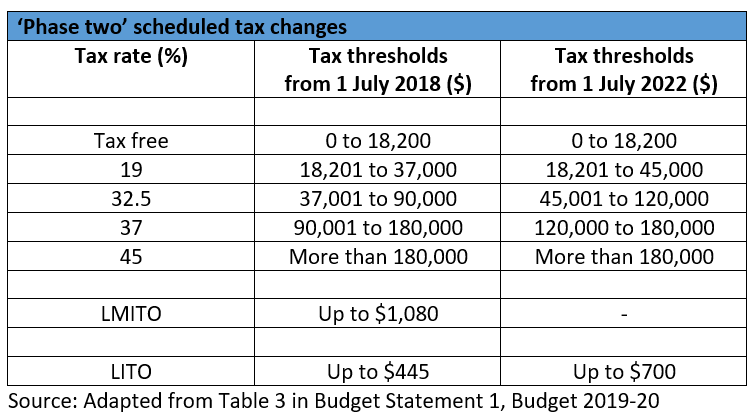

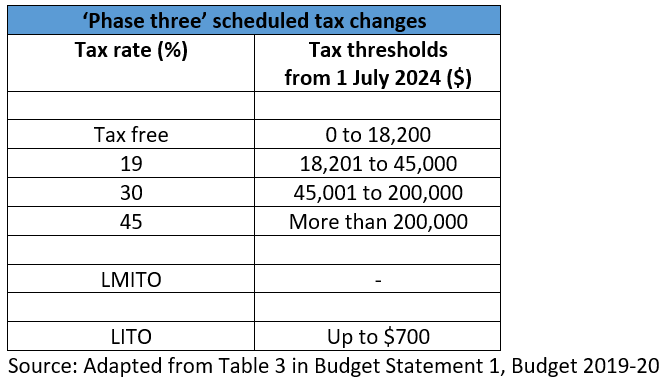

The run-up to next week’s budget has brought the usual speculation about potential budgetary measures, alongside some government announcements regarding spending and other initiatives. Prominent among the discussion to date, at least in terms of potential scale, is the possibility of the government choosing to bring forward either one or both remaining phases of its already-legislated personal tax cuts. Phase one of those tax cuts was introduced in 2018, but phases two and three are still pending.

Phase two is currently scheduled to take effect from 1 July 2022. It will increase the top threshold of the 19 per cent tax bracket from $41,000 to $45,000 (the 2018-19 budget had already introduced legislation to increase the top threshold of the 19 per cent tax bracket from $37,000 to $41,000), increase the threshold for the 37 per cent tax rate from $90,000 to $120,000 and increase the low income tax offset (LITO) to $700 (again, the 2018-19 budget had already flagged an increase in the LITO from $445 to $645 in 2022). Note that the changes to the top threshold of the 19 per cent bracket and the expansion of the LITO are also designed to lock in the previous benefits from the Low and Middle Income Tax Offset (LMITO).

Deloitte Access Economics has estimated that if the Phase two tax cuts were to be brought forward by a year, and the existing LMITO kept in place, the budget cost in 2021-22 – and therefore the amount injected back into the economy – would be around $12.4 billion in 2021-22. On the other hand, if both phases two and three were brought forward and the LMITO was removed a year early, that would cost roughly $21 billion in 2021-22, $14.8 billion in 2022-23 and $15.4 billion in 2023-24. The attraction of this approach is that it would combine fast-tracking already-planned changes with a significant boost to incomes, which as noted above, needs to be part of next week’s budget package. One possible downside, however, at least as far as treating this as a stimulus measure, is that given the high prevailing level of economic uncertainty, many recipients might choose to save at least some share of this increase in disposable income rather than spend it. Moreover, because a substantial share of the benefits will tend to go to higher income taxpayers, all else equal it’s more likely that this group will save a higher share of the increase in their disposable income relative to those on lower incomes.

Other potential policy initiatives that have been canvassed over the past couple of weeks include:

- A further increase in infrastructure investment, including in the form of new incentives for state governments to increase spending. Provided that it is well-targeted, infrastructure investment delivers both short-term demand stimulus and longer-term improvements on the supply side, with this combination making it an attractive policy option. Possible complications here are that bigger projects can take time to get up and running and so risk getting the timing wrong in terms of delivering short-term stimulus. This in turn places a premium on so-called shovel-ready projects, which might involve focussing on a large number of small projects rather than a small number of big investments.

- A subset of infrastructure investment that’s been championed by a number of economists is increased spending on social housing.

- Another popular proposal among many economists is a permanent increase in the JobSeeker payment that would lock in at least some of the benefits from the Coronavirus Supplement, before it expires at the end of this calendar year. Failing this, the government has already flagged that it is minded to extend a version of the Supplement into at least the first quarter of 2021 to provide continued additional income support.

- Policies to boost the incentives for business investment spending have also received some sustained attention, not just in the run up to this budget but in recent years more generally, particularly as the chances of a significant cut to the rate of company tax have diminished. One attractive option here could be the introduction of an investment allowance, although with business capex facing some severe headwinds in terms of high levels of uncertainty and subdued general demand conditions, there is some debate as to whether this would be enough to generate a significant increase in investment under current conditions.

- The idea of a new wage subsidy program that would replace JobKeeper with its focus on supporting the existing structure of employment with incentives to create new jobs has also been canvassed.

- Several plans aimed at stimulating particular sectors of the economy have been proposed and the government has already flagged several initiatives. On 1 October, the Prime Minister announced that the government would be investing $1.5 billion in specific manufacturing sector measures, spread across six ‘national manufacturing priorities.’ Earlier, the government launched policies about the ‘gas-fired recovery’, around investment in new and emerging energy technologies, and a digital business plan.

The government’s new fiscal strategy: To remain in the red

Finally, and as we noted in last time’s Weekly, next week’s budget also arrives in the context of the government’s new fiscal strategy. As sketched out in the PBO scenarios set out above, the pandemic is expected to lead to lower tax receipts and higher spending as a share of GDP ‘for many years to come’ and the government has already started to adapt to this new reality. Under the old, pre-COVID strategy, the ‘plan was to deliver budget surpluses of sufficient size to significantly reduce gross debt and eliminate net debt by the end of the medium term’. But now, the Treasurer has explained:

‘… in the face of this shock, this is no longer the prudent or appropriate course of action. It would now be damaging to the economy and unrealistic to target surpluses over the forward estimates — given what this would require us to do in terms of significant increases in taxes and large cuts to essential services. This would risk undermining the economic recovery we need to bring hundreds of thousands more Australians back to work and to underpin a stronger medium-term fiscal position’.

Instead, the government has adopted a new two-stage fiscal strategy ‘that emphasises jobs and growth’.

While the second stage of the new strategy is familiar in its focus, with a traditional-sounding call to rebuild Australia’s fiscal buffers and stabilise the debt burden, the first phase will see Canberra (1) continue to ‘allow the automatic stabilisers to work freely to support the economy’; (2) maintain the provision of ‘temporary, proportionate and targeted fiscal support, including through tax measures, to leverage private sector jobs and investment’; and (3) ‘push ahead with structural reforms that position the economy for the jobs of the future and which improve the ease of doing business’.

It appears the government has accepted the new consensus view that one big international macro lesson from the global financial crisis was that many countries back then turned off the fiscal tap too soon and embarked on a premature and counter-productive swing to austerity. In this context, the Treasurer noted that any early move to ‘increase taxes or reduce spending on essential services’ would only serve to ‘slow the speed of our recovery’.

An important and welcome innovation in this context is that the Treasurer has now introduced a form of ‘forward guidance’ for fiscal policy, by promising that this first phase of the fiscal strategy ‘will remain in place until unemployment is on a clear path back to pre-crisis levels’ which likely means ‘until the unemployment rate is comfortably back under 6 per cent.’ As a result, we’ve moved from a target of ‘back in the black’ to an acceptance that we’re set to ‘remain in the red’ for some time yet.

Welcome to the world of Budget 2020-21.

Latest news

Already a member?

Login to view this content