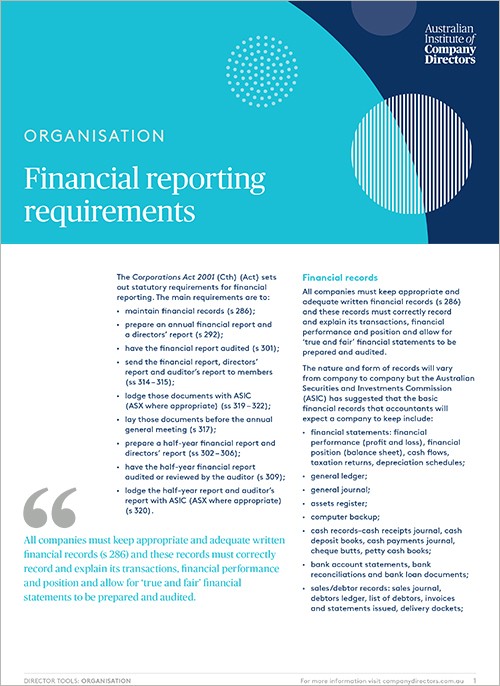

The Corporations Act 2001 (Cth) (Act) sets out statutory requirements for financial reporting.

All companies must keep appropriate and adequate financial records (s 286) but only some need to produce a financial report. Financial reports and directors’ reports must be prepared for each financial year by:

- all disclosing entities incorporated or formed in Australia;

- all public companies, except small companies limited by guarantee, unless directed to do so under s 294A or s 294B;

- all large proprietary companies – according to s 45A, a large proprietary company is defined as meeting two out of three of the following criteria: - consolidated gross operating revenue of more than $50 million; and/or - consolidated gross assets of over $25 million; and/or - more than 100 employees;

- all registered schemes (s 292).

Financial reports must comply with accounting standards and regulations (s 296), however there are some exceptions for small proprietary companies and small companies limited by guarantee where there are specific member or shareholder directions (s 296 (1A) and s 296 (1B)).

For an examination of the financial literacy directors need to have in order to implement sound financial governance practices, refer to Dianne Azoor Hughes’ Financial Fundamentals for Directors.

Latest Director Tools

This is of of your complimentary pieces of content

Already a member?

Login to view this content