Rising unemployment, falling oil prices and disruption to international trade — the coronavirus is likely to trigger a reset in the world economy.

Several months into the coronavirus crisis and the pandemic has ushered in a new world of economic extremes as economic indicators emphasise the historic nature of the shock underway. Granted, the world economy was sending extreme signals even before COVID-19. Several of the world’s major central banks had already driven policy rates below zero and a surprisingly large number of bonds had been trading with a negative yield. Even so, the pandemic has produced some jaw-dropping developments as it generates an economic dislocation unprecedented in peacetime.

In an astounding statistic from the International Energy Agency (IEA), about 4.2 billion people, or 54 per cent of the global population, together representing almost 60 per cent of global GDP, were subject to complete or partial lockdowns as of 28 April, and nearly all the global population was affected by some form of containment measures.

That mass shutdown has had profound effects. As the first country to suffer from COVID-19, China has been an early warning indicator for the rest of the world. So, a 6.8 per cent annual slump in Chinese GDP in Q1 was a troubling sign of things to come. This was the first reported contraction in output since China started producing quarterly data in 1992. Official Chinese numbers have described an economy that grew relentlessly though the Asian financial crisis, dot-com boom/bust, global financial crisis (GFC) and US-China trade war. But this pandemic has brought the hitherto unstoppable juggernaut to an abrupt halt.

The world’s developed economies are expected to endure their own severe economic shocks in the second quarter of 2020, but the preceding quarter has already been incredibly painful for them. Q1 US GDP suffered its biggest decline since the GFC, falling at an annualised rate of 4.8 per cent (or about 1.2 per cent in unadjusted quarterly terms) with total personal consumption undergoing its biggest fall since 1980 and consumption on services falling by the most on record.

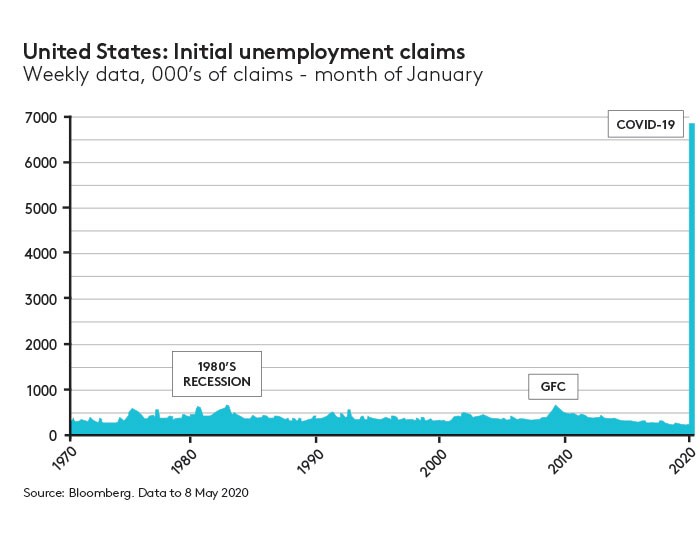

In an astonishing bout of job destruction unlike anything experienced in recent US economic history, the unemployment rate jumped to 14.7 per cent in April, a post WWII record. More than 20 million Americans lost their jobs that month, including more than 18 million (hopefully) temporary layoffs.

Eurozone GDP likewise slumped 3.8 per cent in the March quarter in what was the largest fall since that series began in 1995, with France, Spain and Italy all reporting quarterly contractions. Some estimates suggest that more than 35 million workers, more than one in five of the workforce, in Europe’s five biggest economies (Germany, France, the UK, Italy and Spain) have already applied to have their wages subsidised by the state.

Even before the March lockdowns, global trade was falling at the fastest pace since the GFC, with goods trade shrinking 2.6 per cent over the year. Worse lies ahead: the World Trade Organization has warned that cross-border trade could shrink by up to a third this year, a bigger drop than the trade meltdown during the GFC.

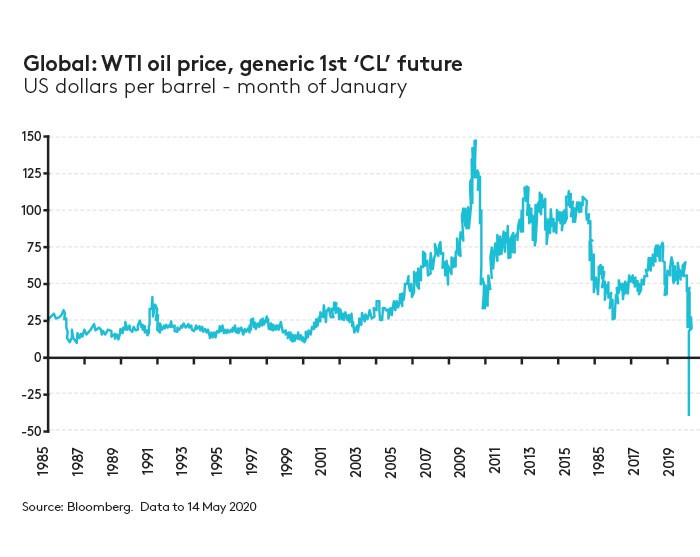

Arguably the most striking development to date has been the collapse in global oil demand. The IEA has estimated that it could drop by 9.3 million barrels per day (mb/d) this year after April alone saw oil consumption fall an incredible 29 million mb/d below corresponding 2019 levels. That enormous demand destruction saw US oil price futures plunge over the month, and in another unprecedented development, turn negative on 20 April.

The crisis has also taken a toll closer to home. Australian business conditions and confidence both experienced their largest monthly falls on record in March, while in April, consumer sentiment suffered its steepest decline in the history of the monthly index. Experimental payroll data from the Australian Bureau of Statistics (ABS) suggest that in the five weeks to 18 April, Australia lost about 7.5 per cent of all jobs across the economy, including about a third of all jobs in accommodation and food services, and more than a quarter of jobs in arts and recreational services. Another ABS survey, covering 22–28 April, reported that seven in 10 businesses are experiencing reduced cashflow, and a similar proportion expect that reduced demand for their goods and services will have an adverse impact over the next two months.

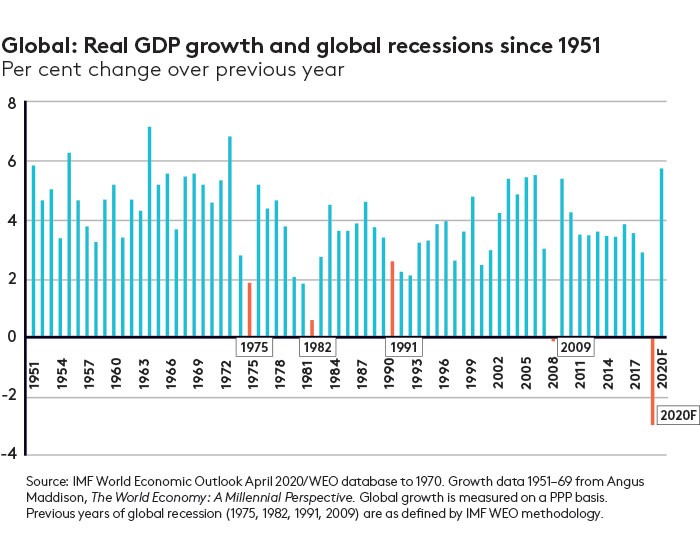

Forecasting is much more challenging than usual in this environment. Many forecasting models rely on some refined version of extrapolation or trend-fitting. That approach is particularly problematic when the shifts they are trying to model are so dramatic — at times, unprecedented — that the relationships captured by the back data may tell us very little about what to expect. With those qualifications in mind, the latest International Monetary Fund (IMF) forecasts tell a dramatic story, predicting the world economy shrinking by at least three per cent this year. That “optimistic” scenario would dwarf the 0.1 per cent fall in world output suffered in 2009 during the GFC, which currently holds the title for the biggest annual GDP decline since 1950.

Likewise, the IMF foresees the Australian economy shrinking by 6.7 per cent this year. Even the conservative RBA, expecting a 10 per cent decline in output in the first half of 2020, has pencilled in a five per cent drop in output for the year. Both forecasts assume we are in for the biggest annual contraction in Australian output since the 1930s depression.

The scale of current economic events and projections cautions against any temptation to model the COVID-19 crisis as a straightforward economic shock — to be swiftly followed by some form of reversion to the mean. Current developments look more like a turning point for the world economy, and possibly the trigger for a significant regime shift. Our current world of extremes could now prove to be the herald of some extreme changes.

Latest news

Already a member?

Login to view this content