The impact of Trumpism and the 2020 US election outcome will be felt long after Joe Biden and Kamala Harris take over the White House. David Uren discusses what a Democrat victory means for the global economy, trade, and geopolitics.

It is tempting to see the election of veteran American congressman and former Vice-President Joe Biden as the resumption of normal transmission after the static of the past four years. Biden’s victory will certainly see an end to government-by-tweet and the revolving door of senior appointments that made President Donald Trump’s inner circle look like candidates on his reality TV show, The Apprentice.

Biden will bring a return of orthodox government, with stable staffing of key positions in the administration. He will also usher in more normal relations with the nations of the world, including stronger commitments to allies and a greater preparedness to work with multilateral institutions.

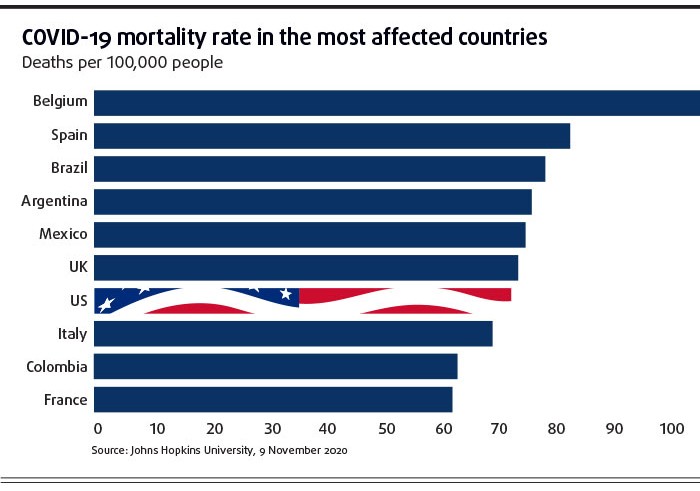

He inherits a resilient economy that is performing better than most other advanced nations, despite the continuing ravages of the coronavirus pandemic. But the forces of economic nationalism that helped propel Trump to the White House in 2016 are undiminished and the challenge of dealing with a resurgent China has become far more acute.

As Company Director went to press, Trump had yet to concede defeat, raising the possibility of a contested transition, while the Biden administration may have to deal with a hostile Senate.

Two run-off Senate elections will be held in the state of Georgia in January, but even if the Democrats were to win both — which would deliver an evenly divided chamber — it’s unlikely they would be able to legislate either Biden’s radically redistributive social program or his proposed multitrillion-dollar investments in a carbon-neutral United States.

Increases in the company tax rate from 21 to 28 per cent and additional taxes on high-income earners, intended to help pay for the promised largesse, are unlikely to gain approval from an obstructionist Senate.

Many of these policies became part of the Biden pitch after more radical presidential candidates —Bernie Sanders and Elizabeth Warren — dropped out of the race, and were calculated to keep their supporters onside.

Shorn of these ambitions, a President Biden will lead a cautious administration. He was selected as the Democrats’ presidential candidate in part because he was seen to have the best chance of recapturing the white working-class voters in the Midwest manufacturing states, who were lost to Trump in the 2016 election. His success in winning back Pennsylvania, Wisconsin and Michigan from the Republicans underlines the extent to which he will have to adhere to the same defensive approach to US manufacturing taken by Trump.

He will remain wary of trade deals and continue to prosecute a global campaign against China — like Trump’s stance, it will reflect not only the interests of American industry, but also the deep strategic concerns of the defence and national security establishment. A Biden administration will possibly also reflect more concern for human rights.

The rupture between the US and China in 2020 will echo in the years ahead. What began as a conflict over the US trade deficit has morphed into a much broader strategic contest. There is little prospect of Australia’s fractured relationship with its major trading partner being repaired while the superpower tussle continues.

One far-reaching consequence of rising economic nationalism is a loss of confidence in the ability of multilateral forums to resolve international tensions. One of the dividing lines in the US election was between Trump’s “America First” and Biden’s expressed belief that the US had to re-engage with global forums. However, Trump’s unilateralism was responding to emerging problems in key multilateral institutions.

Trade — for so long the driver of global prosperity — is vulnerable amid swelling global payments imbalances. One of the drivers of the destructive polarisation in US politics has been the impact of Chinese competition in traditional manufacturing districts where the middle political ground has disappeared.

Governments across the world have responded forcefully to the pandemic — as they did following the global financial crisis — with large spending packages to support households and business.

A big change in the aftermath of the financial crisis is that governments no longer see the increase in debt as an aberration to be corrected by austerity measures as conditions improve. Instead, there is a growing belief that much larger debts can be sustained.

The break with China

The past year brought a ceasefire in the trade war between the US and China, following a trade deal struck in December 2019. However, tension has escalated, with the Trump administration defining China as a threat to freedom worldwide. “If we don’t act now, ultimately the Chinese Communist Party [CCP] will erode our freedoms and subvert the rules-based order that our societies have worked so hard to build,” declared US Secretary of State Mike Pompeo in July.

A Biden administration is less likely to press for regime change, but the national security concerns about China are bipartisan. Biden has characterised the Chinese oppression of Muslim minorities in Xinjiang as “genocide” and declared that a Biden administration would “put values back at the centre of our foreign policy, including how we approach the US-China relationship”. Democrats in Congress were responsible for legislation imposing sanctions on Chinese officials over Xinjiang and China’s security crackdown in Hong Kong.

The US has progressively tightened its restrictions on both the export of US technology to China and the use of Chinese technology on home soil. Again, there has been bipartisan support over plans to ban the popular Chinese short-video application TikTok, as well as the Chinese social media and payments platform WeChat. The US has, with some success, lobbied Western nations to ban China’s Huawei from participation in building 5G internet infrastructure.

Chinese officials have responded cautiously to the US, maintaining that the complementarity between the two economies creates opportunities on both sides. China’s government has liberalised foreign investment in the financial services sector, attracting a number of major US institutions. China has focused retaliation against what it perceives as an increasingly hostile stance in the West on US allies — notably, Australia and Canada. The Biden administration would be in a position to ease Canada’s troubles with China by abandoning the US extradition request for Huawei finance director Meng Wanzhou, but there is no obvious US reset for Australia’s problematic relationship. Chinese officials have constantly said it is up to Australia to heal the breach, while providing no clue about what a remedy would look like.

Both the US and the Australian relationships with China have been heavily influenced by emerging nation security concerns, which have outweighed economic considerations in matters such as foreign investment, infrastructure development, technology access and data integrity. These concerns will be continuing sources of aggravation in dealing with China.

US efforts to block the supply of technology to China and encourage American firms to repatriate their supply lines to the US has prompted a reciprocal stance in China. In October, the country’s leader, Xi Jinping said: “In order to ensure China’s industrial security and national security, we must build a self-developed, controllable, safe and reliable industrial and supply chain. We should strive to have at least one alternative source for important products and supply channels to form a necessary industrial back-up system.”

There is an enormous investment in global supply chains; US firms have committed around US$400b to their operations in China, employing 1.75 million staff. They are not readily unravelled, but the pressure to do so will intensify.

Multilateralism

Trump’s withdrawal from the Paris Agreement on climate change, which he’d announced in June 2017, took formal effect on the day after the brutally contested US election. It was among a series of international agreements and organisations that the Trump administration walked away from, including the Trans-Pacific Partnership trade deal, the World Health Organization, the Iran nuclear deal, UNESCO, the Intermediate-Range Nuclear Forces Treaty and the United Nations Human Rights Council (UNHRC). Trump threatened to withdraw from the World Trade Organization (WTO), drafting legislation to do so, and also considered withdrawing from NATO.

Biden — a long-time member of the US Senate Committee on Foreign Relations — has promised to re-engage with the global community. “The fates of nations are more intertwined than they ever have been,” he said during the election campaign. “Climate change, nuclear proliferation, international and transnational terrorism, cyber warfare, disruptive new technologies, mass migration... none of them can be resolved by the United States alone or any nation acting alone.”

The multilateral architecture (including the UN, WTO, G20, International Monetary Fund and the World Bank) is predominantly a US creation, though the unilateralism of the Trump administration was a response to its growing inadequacies.

Biden’s embrace of multilateralism will be welcomed around the world, but it is not a panacea for global tensions. The UN is increasingly a proxy field for the contest between the US and China, with the latter having successfully marshalled the numbers to have Chinese officials appointed to lead four of the 15 UN agencies. When Hong Kong’s national security legislation was debated in the UNHRC, China won the support of 52 nations, soundly defeating critics of the measure led by the United Kingdom, which was able to rally only 27.

The G20 was a decisive force in the immediate aftermath of the global financial crisis, but proved ineffective in providing any coordination of economic or trade policy during the pandemic beyond limited debt relief for the poorest nations.

More fundamentally, the pledge to avoid raising trade barriers, which all G20 members signed in the wake of the financial crisis, has been widely ignored. According to the Global Trade Alert database, the share of the world’s exports subject to barriers from quotas, subsidies and tariffs rose from 40 to 72 per cent over the past 10 years, before the pledge to avoid protectionism was finally jettisoned.

Biden has said he will cooperate with China in areas where there are mutual interests, such as climate change. He can rejoin the Paris Agreement by executive order, without requiring congressional assent and says he will formally take that initiative on his first day in office. However, the increasingly entrenched rivalry will make joint action of any sort difficult. Biden’s vision of multilateralism does not embrace rivals. He has proposed a global Summit for Democracy to rally US allies and friends in a concerted approach to China and Russia.

The US under Biden: What directors need to know

- A Biden-led administration has promised to re-engage with the global community and has signalled its intention to rejoin the Paris Agreement on climate change and restore relationships with the World Trade Organization, the Trans-Pacific Partnership on trade and the World Health Organization.

- Like Trump, Biden will continue to prosecute a global campaign against China around strategic concerns over defence and national security. Plus, the new president will add a concern for breaches of human rights.

- The US will battle the coronavirus pandemic well into 2021. However, its economy has proven more resilient than expected by institutions such as the International Monetary Fund and OECD, and is likely to outperform many other advanced nations.

- With world trade volumes shrinking in the wake of COVID-19, the growing trade imbalances are likely to become a heated political issue over the year ahead.

Trade tensions

While remaining a member of the WTO, the Trump administration brought its ability to resolve disputes to a standstill by vetoing all judicial appointments to its appeals panel until it lost its quorum. In a final affront to the organisation, the US responded to a WTO ruling that US tariffs on China were illegal by lodging an appeal to the non-existent panel.

Trump argued that globalisation was giving the Chinese a free ride into US markets, telling the UN in September that “for decades, the same tired voices proposed the same failed solutions, pursuing global ambitions at the expense of their own people”.

Research by eminent Massachusetts Institute of Technology economist David Autor shows Trump was at least partly correct: competition from China since its admission to the WTO in 2000 caused long-lasting job losses, lower wages and reduced labour force participation in traditional US manufacturing districts.

Autor also revealed that the economic shock had major political effects, with research released before the election showing support for extremes on both the right and left becoming greater in the affected manufacturing areas than in the rest of the country. Trump tapped the disaffection of the white working-class.

A Biden administration would be expected to re-engage with the WTO and break the impasse over the appeals panel. It is possible it may accept the WTO’s rejection of US tariffs on Chinese goods, withdrawing the Trump administration’s appeal as part of a negotiated easing of the trade war. However, dissatisfaction with the multilateral framework and its inability to deal with the dominant role of the Chinese state in its economy runs deep on both sides of US politics.

The tensions over trade are likely to be inflamed by a rise in global payments imbalances. China’s rapid recovery from the pandemic brought a return to economic growth and a surge in its exports. Council on Foreign Relations economist Brad Setser predicts a Chinese trade surplus reaching US$300b for the year — the highest since 2008.

While the US trade war with China has brought a reduction in its bilateral deficit, it has really only succeeded in pushing the imbalance to other trading partners, with the overall US deficit also the deepest since the onset of the financial crisis. With world trade volumes shrinking in the wake of the pandemic, growing trade imbalances are likely to become a heated political issue in the year ahead.

Debt and deficit

Increased government debt is one change locked in for 2021. According to consultancy Fulcrum Asset Management, gross government debt is expected to rise from a 2019 average of 114 per cent of GDP among the major advanced economies to 141 per cent in 2021 as they respond to the pandemic.

Central banks are playing an increasing role in financing that debt. The share of advanced country debt held by central banks is expected to rise from 21 per cent in 2019 to 36 per cent by 2021.

No government has formally accepted the central tenet of Modern Monetary Theory, which holds that inflation is the only constraint on spending by governments that control their own currency. However, research by former IMF chief economist Olivier Blanchard — showing economic growth has exceeded interest rates in most nations across most of the past 70 years — suggests countries can and do grow their way out of debt without necessarily burdening taxpayers. As former US Treasury Secretary Larry Summers has commented, “Countries that borrow in their own currencies and run independent monetary policies have substantial latitude on fiscal policy.” Summers adds that the latitude is not unlimited, but is far greater than conventionally thought.

David Uren is a non-resident fellow at the US Studies Centre at the University of Sydney.

Latest news

Already a member?

Login to view this content