Overview

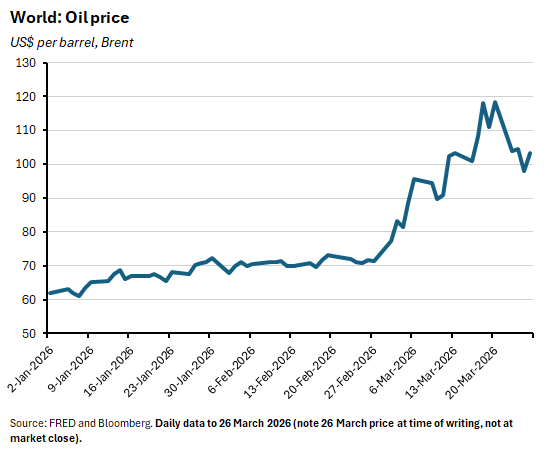

- Oil prices have been volatile over the past week as markets struggle to price the likely endgame for the war in the Persian Gulf amid conflicting claims from Washington and Tehran.

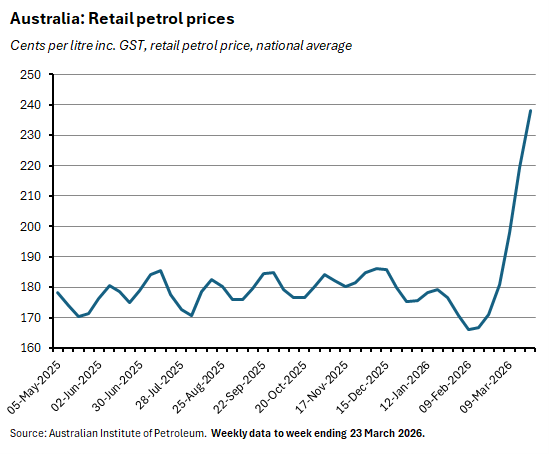

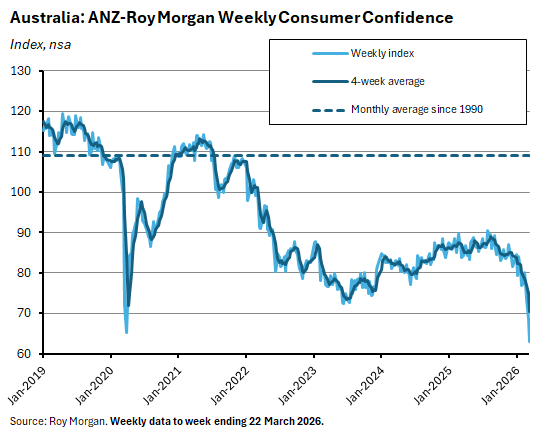

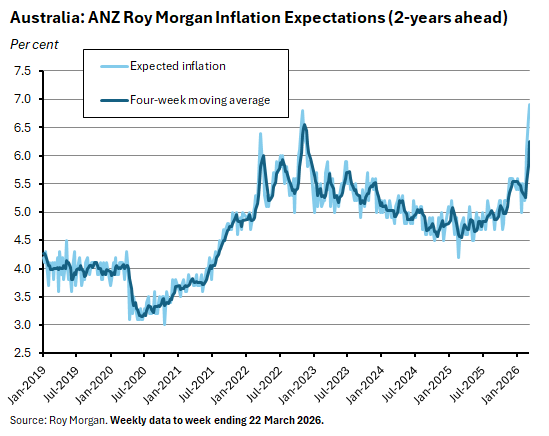

- Australian households are already feeling the pain as petrol prices continue to rise and the media runs stories about shortages and potential rationing. Consumer confidence has now fallen to its lowest level on record as households contemplate yet another element of the cost-of-living squeeze as higher prices at the pump have propelled weekly inflation expectations to a record high.

- This week’s release of February 2026 inflation data offered only limited comfort. While the outcomes proved to be slightly softer than the market had expected, pre-war headline and underlying inflation remained above the RBA’s inflation target, reminding us of the awkward starting point for any monetary policy response.

- As higher fuel prices drive up the headline inflation rate over coming months, the RBA will be watching closely as to how prices, wages, business margins, and inflation expectations adjust in an economy that it judges was already grappling with binding supply constraints.

This week we review the unfolding impact of the war-driven global energy shock on Australian consumer sentiment and household inflation expectations before checking in on Australia’s final pre-war (February 2026) inflation reading. There will be no update next week as the Economic Weekly takes an Easter break but, to keep readers occupied over the long weekend, we will share a piece on early messages from the war for Australian supply chain risk on the LinkedIn version of this newsletter. You can follow along here.

Markets swing and consumers cower

Once again, the financial headlines this week were dominated by the war in the Middle East, as market prices swung in response to shifting assessments about the likely duration of the conflict. Claims of productive peace talks and an imminent resolution to the conflict sent the oil price back below US$100/b as traders hoped that President Trump had found his exit strategy. Only for prices to then head higher as Tehran rejected the idea of an imminent deal. This pattern of fluctuating presidential rhetoric driving market sentiment has become a familiar feature of the Trump presidency by now, and the lesson is that daily commentary usually leaves us little the wiser about the longer-term outlook.

In the current case, that is because two competing narratives remain in play. One is a variant on the TACO trade, which assumes that the White House has no appetite for the accumulating economic and political pain that a drawn-out conflict will entail, and that this rules out a long war. In this view, it’s still just a question of finding the right off-ramp. The opposing view warns that it takes two (or counting Israel, three) to TACO, and that the United States is at risk of being pulled into a kind of escalation trap, not least because it is difficult to see Washington now acquiesing to effective Iranian control of 20 per cent of global oil and gas flows and accepting the subsequent loss of prestige. Meanwhile, the greater the damage inflicted on regional energy infrastructure as the conflict unfolds, the longer-lasting the disruption to global energy markets. The IEA reckons that 40 energy assets in the region have now been either damaged or destroyed as a result of the war.

While markets fluctuate, Australian households are signalling their discomfort with the early impact of the conflict. In particular, higher petrol prices and reports of localised shortages are already taking a toll on sentiment. According to the latest reading from the ANZ-Roy Morgan Consumer Confidence Index, for example, confidence fell 5.4 points to an index reading of 63.1 in the week ending 22 March 2026. That drop also followed last week’s 25bp rate hike by the RBA and sent confidence slumping to its lowest level in the history of the series, exceeding its pandemic-era low.

Consumers are also pessimistic about the inflationary consequences, with the accompanying survey measure of weekly inflation expectations climbing another 0.2 percentage points last week to hit 6.9 per cent and a record high.

What will policymakers do next?

The ongoing uncertainty about the future course of the war is also a headache for policymakers.

For now, Canberra’s focus has been on managing the near-term supply implications. The disruption to domestic supply chains has prompted the government to announce a range of measures including a temporary reduction in the Minimum Stockholding Obligation and a temporary easing of fuel standards in order to boost domestic supply. But with the Budget looming, questions as to the government’s fiscal policy response will become increasingly pressing, and potentially uncomfortable.

Recall that, pre-war, the talk had been of a budget that would seek to combine more efforts to boost Australia’s flagging productivity performance with tax and savings measures that would also be targeted at both budget repair and intergenerational equity. To that list we can now add pressure for Budget 2026 to deliver another round of cost-of-living relief to households, giving the Treasurer another ball to juggle on Budget night.

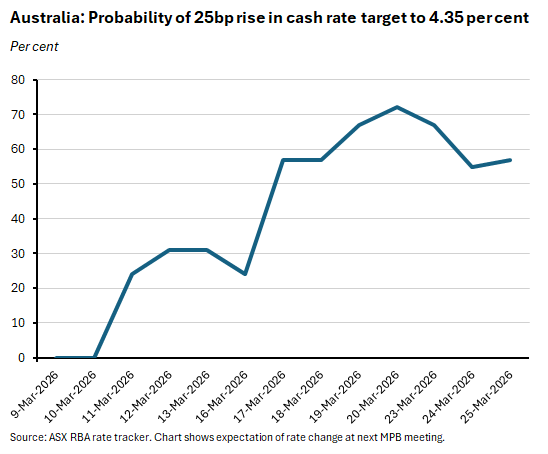

At Martin Place, meanwhile, the challenge is how to adjust an already-underway tightening of monetary policy given the war shock. So far, that adjustment has involved bringing forward an anticipated rate hike from May to March. But the Monetary Policy Board (MPB)’s split vote indicates some uncertainty as to the correct course of action. Markets have also become a little less gung-ho in recent days, as the probability of a third consecutive rate hike at the May MPB meeting has retreated a little from recent highs (but remains above 50 per cent).

A key complication for the MPB and the RBA is that the starting conditions are far from ideal. Inflation was already above target, growth (demand) towards the end of last year had been running a bit faster than Martin Place expected, the RBA thinks that labour market conditions are on the tight side, and the economy’s supply capacity has disappointed. That reduces the scope for the central bank to look through the energy shock, even as uncertainties about the relative size of the incoming hit to growth and boost to inflation persist.

A (slightly) softer pre-war inflation reading offers limited comfort

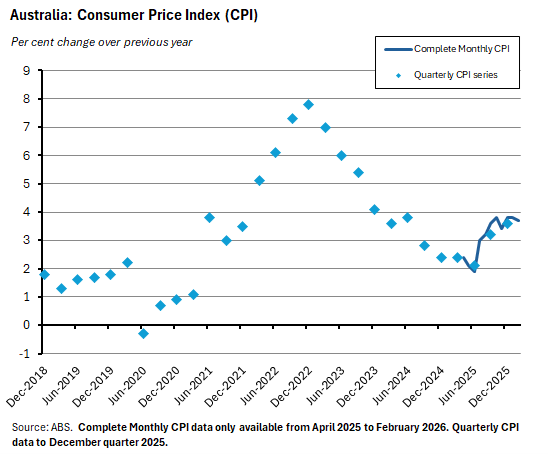

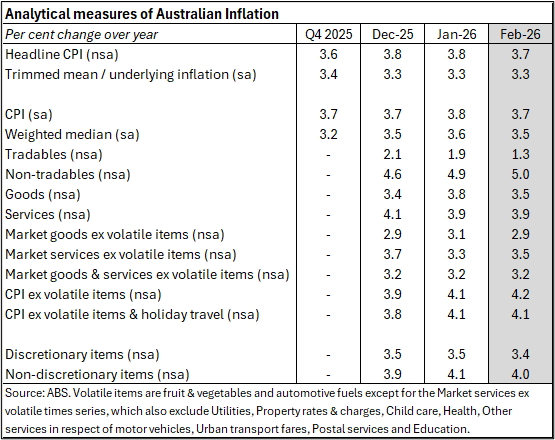

In that context, the ABS reported this week that Australia’s headline Consumer Price Index (CPI) was flat over the month in February 2026 to be up 3.7 per cent over the year. The good news was that this was a little below the January 2026 result of 3.8 per cent and was also slightly softer than the consensus forecast, which had expected headline inflation to be unchanged at 3.8 per cent.

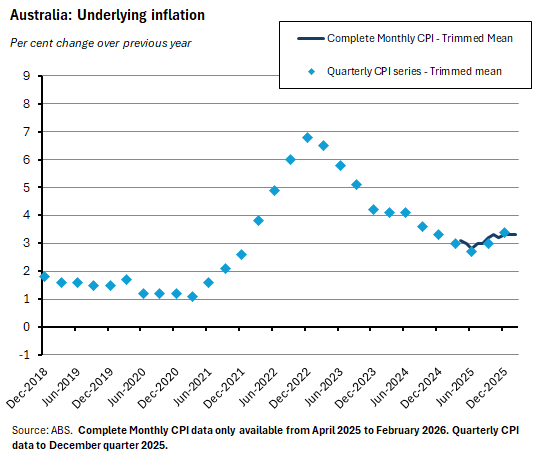

Underlying inflation as measured by the trimmed mean rose 0.2 per cent over the month to be up 3.3 per cent over the year. That was unchanged from the (downwardly revised) January and December annual rate. It too was a little below the consensus forecast, which had anticipated a 3.4 per cent print.

The Bureau said that the largest contributor to annual inflation last month was the Housing group, which rose by a strong 7.2 per cent over the year, up from 6.8 per cent in January. That reflected robust increases for Electricity (up 37 per cent year-on-year, with the outsized rise once again a function of households exhausting the extended Commonwealth Energy Bill Relief Fund and related State Government electricity rebates), New dwellings (up 3.7 per cent) and Rents (up 3.8 per cent).

Other groups to see large annual rises included the Clothing and footwear group (up five per cent over the year led by higher prices for gold jewellery), the Education group (up 4.8 per cent as school fees increased at the start of the year), the Recreation and culture group (up 4.1 per cent due to strong rises for Domestic travel and accommodation and for Audio visual and media services) and the Food and non-alcoholic beverages group (with lamb and beef prices both up 13 per cent and Meals out and takeaway prices rising 3.7 per cent).

In a reminder that the February data are capturing the situation before the outbreak of the conflict in the Middle East, the Transport group recorded a 0.2 per cent decline in prices over the year, as Automotive fuel prices fell 3.4 per cent over the month to be down 7.2 per cent year-on-year. That monthly decline will, of course, go into sharp reverse in the March data.

Analytical measures of inflation showed slowdowns in the annual rate of increase across a range of measures including the Weighted median, tradables, goods, and market goods ex volatile items, as well as for discretionary and non-discretionary items. At the same time, however, there were modest upticks in the inflation rate for non-tradables, market services ex volatile items, and the CPI ex volatile items (see table for details).

Taken overall, the February reading represented a slight softening in the inflation picture. Even so, that still left both headline and underlying inflation above the top of the RBA’s target band. And with the energy price shock and other disruptions originating in the conflict in the Middle East set to start influencing the inflation numbers from next month’s reading onwards, February’s result will have strictly limited implications for the future trajectory of monetary policy.

That energy price shock is set to unfold in stages, with the initial direct impact being felt via an increase in automotive fuel prices (3.35 per cent of the CPI basket), which will drive up the headline rate starting with the March result. This will filter into other categories over time as input costs adjust, leading to higher underlying inflation readings. And after that, the net inflationary impact will depend on how other prices, wages and inflation expectations respond plus any offsetting effects on demand arising from the squeeze from higher prices on disposable income and higher costs on business margins.

Other Australian data points to note

The ABS said that Engineering Construction work done fell 1.8 per cent (seasonally adjusted) over the December quarter 2025 to be three per cent lower over the year. Private sector work done was up 0.3 per cent quarter-on-quarter and rose 1.3 per cent year-on-year, while public sector work done fell 4.2 per cent quarter-on-quarter and dropped 7.9 per cent year-on-year.

According to National Accounts data on Finance and Wealth, Australian household wealth rose by $453.7 billion in the December quarter 2025 to $18.8 trillion. The ABS said that a $368.6 billion gain in the value of residential land and dwellings accounted for the bulk of that increase.

The ABS published new Input-Output tables for 2023-24.

Further reading and listening·

- On Australia’s reliance on diesel.

- Christopher Kent, RBA Assistant Governor (Financial Markets) spoke this week on reassessing Australian financial conditions. According to Kent, ‘A broad range of evidence suggested that cash rate increases through 2022 and 2023 had taken the stance of policy into restrictive territory…by early 2025…the Board determined that it was appropriate to reduce the level of restrictiveness somewhat. From around September 2025…the weight of evidence began to shift, suggesting that financial conditions were no longer restrictive enough to return inflation to target in a reasonable time…policy was tightened in February and March to help bring down inflation.’ More recently, the financial market consequences of the conflict in the Middle East ‘have led to some tightening in financial conditions. All else equal, that implies a decline in short-run neutral rates here and offshore – that is, a tighter stance of monetary policy for a given cash rate. However, the supply shock also poses a risk to inflation and longer-term inflation expectations at a time when there are ongoing capacity pressures in Australia...This could both push short-run neutral rates higher and necessitate a more restrictive stance of policy…The longer the conflict persists, the larger the economic impact will be…A negative supply shock pushes up prices and leads to weaker economic activity, making us all poorer. Central banks cannot change that. But they can ensure that the initial rise in prices does not lead to a rise in longer term inflationary expectations and extended inflationary pressures.’

- Also from the RBA, Brad Jones, Assistant Governor (Financial System) gave a speech on the next era of financial system innovation.

- A Treasury submission to the Select Committee on Productivity in Australia.

- A DFAT brief on the recently signed Australia-European Union Free Trade Agreement (A-EU FTA). One cautious assessment on intellectual property implications from the ANU via the Conversation.

- Grattan’s Tony Wood says, don’t waste this energy crisis.

- The Prime Minister’s speech to the Australian Minerals Industry Dinner. According to the PM, we need to be ‘…preparing ourselves for the economic aftershocks that will follow this conflict. Because the disruption we are already seeing in the global economy is not due to arbitrary trade barriers, or sanctions tied to strategic competition. It goes deeper than that. This is about ongoing threats to the safety of global shipping routes. And the physical destruction of oil and gas infrastructure across the Middle East. So even if we were to wake up tomorrow to the welcome news that this conflict was over, there would still be a long economic tail to reckon with. All of this underlines a simple reality. The stable, predictable world of ever-expanding free trade is gone - and it will not be returning any time soon.’

- The ABS introduces the ‘u-series’ on underemployment and underutilisation.

- The e61 Institute looks at the relationship between migration and measures of fertility. Because Australia’s migrant intake is so heavily weighted toward temporary students and workers from low-fertility source countries, migration into Australia is mechanically dragging down the headline Total Fertility Rate (TFR). Since 2019, the TFR of Australian-born women has fallen from roughly 1.73 to 1.64 while over the same period the aggregate TFR has fallen more than twice as much, dropping from 1.69 to 1.48.

- The latest (March 2026) Quarterly Productivity Bulletin.

- The OECD’s Anti-Corruption and Integrity Outlook 2026. Country notes for Australia paint a mixed picture relative to OECD benchmarks.

- An Economist magazine briefing on what a battle to reopen the Strait of Hormuz might look like. And on the cognitive dissonance gripping financial markets.

- You can’t print molecules.

- The McKinsey Global Institute with a 2026 update on Geopolitics and the geometry of global trade.

- ECB President Christine Lagarde on Navigating energy shocks: ‘Small, one-off and short-lived supply shocks can be looked through. But as expected deviations from our inflation target grow larger and more persistent, the case for action become stronger… In the euro area, the historical evidence suggests that the risk of broad pass-through from energy prices is the exception rather than the rule. When shocks are small in magnitude and short in duration…their inflationary impact tends to largely stay within the energy component itself. But two factors can change that picture…first…the intensity and duration of the shock. ECB research shows that the relationship between energy price shocks and inflation can be non-linear: while small increases trigger no significant reaction in prices, larger shocks have disproportionately stronger effects…second is the propagation of the shock, which depends on the macroeconomic environment...Firms are more likely to be able to raise prices when demand is stronger, workers are more likely to be able to bargain for higher wages when labour markets are tighter, and both are more likely when inflation is already high…pass-through is measurably stronger when capacity utilisation is high and unemployment is low…wages feed into prices more forcefully when inflation is already elevated.’

- Paul Kedrosky discusses AI and the fable of the ATMs.

- Greg Ip in the WSJ looks at some of the business implications of Anthropic’s battle with the Pentagon.

- The relationship between monetary policy, household debt, and asset prices.

- The Guardian goes inside China’s robotics revolution.

- And the NY Fed considers China’s Electric Trade.

- On business investment in the era of digital transformation.

- How the world’s first electric grid was built.

- An FT Big Read on the economic impact of the US crackdown on migrant labour.

- How conventional ICBMs could transform Australia’s security position.

- The Rhodes Centre podcast talks to Eswar Prasad about the Doom Loop of global disorder.

- Ed Glaeser’s speech to the LSE on housing supply and the future of our urban planet.

- The Odd Lots podcast on the petrochemical shock now hitting global plastics and packaging.

Latest news

Already a member?

Login to view this content