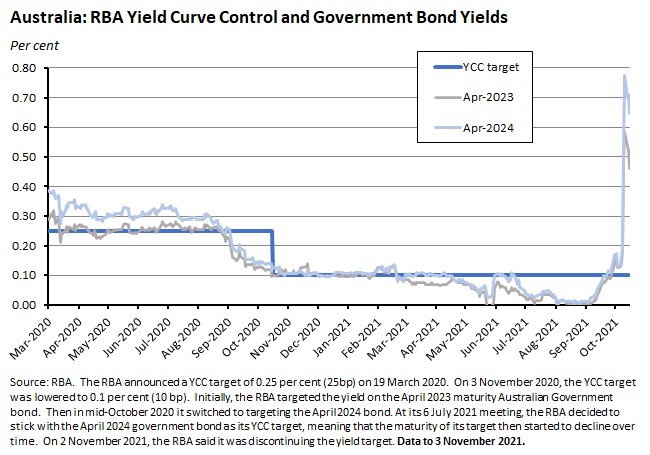

At this week’s monetary policy meeting the RBA announced an abrupt end to the policy of yield curve control that it introduced back in March last year. The RBA also changed the language around the likely timing of any future increase in the cash rate, removing the long-standing qualification that the conditions for any such move were unlikely to be met before 2024.

Both changes go some way towards validating recent market scepticism around Martin Place’s position on inflation and the timing of a hike in the cash rate. But the shift in the RBA’s views on both is a limited one. Governor Lowe was at pains to argue that the RBA had not embarked on a radical rethink on either inflation or on the probable timing of a cash rate hike, stating that Australia did not have a major inflation problem, describing market projections of early interest rate hikes as a ‘complete overreaction’ to the Q3 inflation reading, and arguing that ‘the latest data and forecasts do not warrant an increase in the cash rate in 2022.’ All of which leaves a pretty substantial gap between where markets are at and the RBA’s view of the economy.

The RBA’s decision to dump its yield target is part of a broader pattern of central bank reactions to changing economic conditions. Last week, for example, the Bank of Canada terminated its QE program. And this week, the Federal Open Market Committee (FOMC) of the US Federal Reserve announced that it would start to scale back (‘taper’) its US$120 billion monthly bond-purchase program. Beginning later this month, the Fed will reduce net asset purchases by US$15 billion / month (US$10 billion for treasury securities and US$5 billion for agency mortgage-backed securities) and then next month, purchases will fall by a further US$15 billion. The FOMC said that it ‘judges that similar reductions in the pace of net asset purchases will likely be appropriate each month, but it is prepared to adjust the pace of purchases if warranted by changes in the economic outlook’ with Fed chair Powell explaining that purchases could ‘speed up or slow down’ as needed. Powell also noted that ‘bottlenecks and supply chain disruptions’ had seen overall inflation running well above the Fed’s two per cent goal, conceding that ‘supply constraints have been larger and longer lasting than anticipated.’ But – similar to the RBA’s Lowe – he also reiterated the Fed’s view that it expects supply-side disruptions to pass and inflation to return to levels ‘much closer’ to the Fed’s goal.

Economic headlines this week were also concerned with the meeting of many (but not all – important absentees included China’s Xi Jinping and Russia’s Vladimir Putin) of the world’s leaders at COP26. To date, the Conference has seen more than 100 countries sign up to promises to halt deforestation by 2030 and to reduce methane pollution by 30 per cent from 2020 levels by the end of this decade, along with an announcement from India that it would target net zero emissions by 2070, and a headline-grabbing claim from Mark Carney that the Glasgow Financial Alliance for Net Zero (Gfanz) had up to US$130 trillion of private capital committed to hitting net zero emissions by 2050. For more background see this primer on COP26, which looks at the road to the Glasgow conference and assesses the pre-meeting state of play.

This week also brought a big download of data on Australia’s housing market, with numbers on dwelling values, lending rates, building approvals and housing credit. Although the monthly pace of growth in dwelling values continued to ease in October, the annual rate of change remains at the highest seen this century. Our updated housing market chart pack pulls together the numbers.

Other Australian data reviewed below include ANZ job ads, PMI readings, consumer confidence, international trade and retail sales.

This week’s roundup of linkages includes the vulnerability of Australia’s export base to climate action, good news and bad news on the budget, a ‘practical plan’ for Australian governments to target net zero, the ongoing dominance of the US dollar as a trade invoice currency for Australia, the global supply chain crisis, why US CEOs are rethinking offshoring and outsourcing, tracking trade from space, and how China avoided a Soviet-style collapse.

What I’ve been following in Australia . . .

What happened:

At its 2 November 2021 monetary policy meeting, the RBA Board decided to discontinue the target of 10bp for the April 2024 Australian Government bond, exiting from the yield curve control (YCC) policy the RBA had announced on 19 March 2020. The Board left the other key settings of monetary policy unchanged, maintaining the cash rate target at 10bp and continuing with its program of purchasing government securities ‘until at least mid-February 2020.’

The Board also changed the language around the likely timing of any future change in the cash rate. As an example of the previous wording, consider the statement following the 5 October monetary policy meeting, which said that the Board would not ‘increase the cash rate until actual inflation is sustainably within the two to three per cent target range. The central scenario is that this condition will not be met before 2024 [emphasis added].’ That 2024 reference was also used following the 7 September meeting and slight variants on it appeared following the 3 August meeting and the 6 July meeting. Indeed, the general guidance around the conditions for a change in the cash rate being unlikely to be met ‘until 2024 at the earliest’ has been deployed since the February meeting of this year. But this month saw the statement drop any mention of 2024, saying instead:

‘The Board will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range. This will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently. This is likely to take some time. The Board is prepared to be patient, with the central forecast being for underlying inflation to be no higher than 2½ per cent at the end of 2023 and for only a gradual increase in wages growth.’

The statement also previewed the RBA’s new forecasts that will appear in more detail in Friday’s release of the November 2021 Statement on Monetary Policy (SOMP), reporting:

- ‘The central forecast is for GDP growth of 3 per cent over 2021 and 5½ per cent and 2½ per cent over the following two years.’

- ‘The central forecast is for the unemployment rate to trend lower over the next couple of years, reaching 4¼ per cent at the end of 2022 and 4 per cent at the end of 2023.’

- ‘The central forecast is for underlying inflation of around 2¼ per cent over 2021 and 2022 and 2½ per cent over 2023. Wages growth is expected to pick up gradually as the labour market tightens, with the Wage Price Index forecast to increase by 2½ per cent over 2022 and 3 per cent over 2023.’

The RBA also welcomed APRA’s recent move to increase the interest rate serviceability buffer on home loans.

In addition to the regular statement following the monetary policy meeting, RBA Governor Philip Lowe also delivered an online webinar a few hours later in which he provided a more detailed discussion of the decision to dump the central bank’s YCC program.

The yield target, he explained, had originally had two motivations. ‘The first was to directly anchor the short end of the yield curve so that funding costs were low across the economy…second…was to reinforce the Board's forward guidance that the cash rate was very unlikely to be increased for three years, which at the time ran until March 2023.’ In Lowe’s view, while the policy had been effective on both counts, this effectiveness had declined over time as expectations about future interest rates shifted in response to changes in economic circumstances. Those same changes in circumstances had also led the RBA to adjust its own views on the probabilities regarding a likely increase in the cash rate. When YCC was introduced, the RBA Board ‘assigned a very low probability to an increase in the cash rate over the three-year horizon of the target’. But now, according to Lowe:

‘the balance of probabilities is a little different. Given our forecasts, it is still entirely plausible that the first increase in the cash rate will not be before the maturity of the current target bond – that is, the bond with a maturity date of April 2024. But it is now also plausible that a lift in the cash rate could be appropriate in 2023.’

He continued:

‘I want to make it clear that this decision does not reflect a view that the cash rate will be increased before 2024…there is genuine uncertainty as to the timing of future adjustments in the cash rate…it is still entirely possible that the cash rate will remain at its current level until 2024. But it is also possible that an earlier move will be appropriate. Given this, the Board judged that there were more costs than benefits in seeking to anchor the yield on the April 2024 bond at 10 basis points.’

There was also an operational reason for the decision:

‘If we had sought to pin the yield on the April 2024 bond at 10 basis points…we would have ended up holding all the freely tradable bonds in the bond line, so that trading in that bond would cease. This would have further diminished the usefulness of the target.’

Governor Lowe also stressed that the RBA’s forward guidance was ‘based on the state of the economy, not the calendar.’

Why it matters:

The RBA’s decision to exit from YCC is an important one as it fulfills a key precondition for any subsequent move in the cash rate. In that sense, this is clearly something of a validation for the market view that the central bank may have to move up its timetable for increases in the cash rate. Quitting YCC also comes – as discussed in the previous two weekly notes – after a period of sustained market pressure on the yield target. Indeed, when the RBA had failed to step in and defend the target through the end of last week, markets had judged that YCC was over. They were right.

Governor Lowe acknowledged in his comments that one consequence of the RBA’s recent inaction on this front had been some turbulent days in the bond market, conceding that the decision to stand out of the market ‘did result in uncertainty as to our policy and affected market pricing and liquidity.’ His explanation was that it was better to wait for the Board to review the situation and decide on the future of the yield target than to ‘enter a thin market in an effort to defend a target that was losing credibility.’

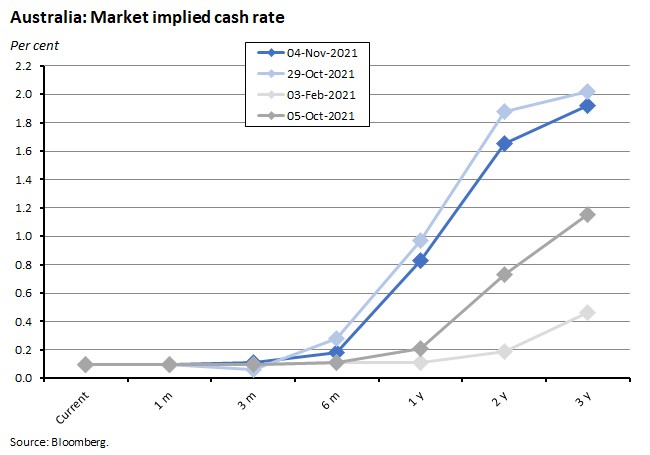

What of the broader debate over the likely timing of a first increase in the cash rate? There is no doubt that the RBA has conceded some significant ground this week. As well as discontinuing the yield target, the explicit reference to the conditions for rate hikes being unlikely to be met before 2024 has now been banished; the Governor has conceded that ‘it is now…plausible that a lift in the cash rate could be appropriate in 2023’; and he has acknowledged both that the global inflation shock currently underway could yet prove to be more persistent than the RBA expects and be transmitted to Australia, and that there is also some significant uncertainty around the way domestic wage growth will respond to an unemployment rate near four per cent.

Even so, it’s also clear that there has not – yet – been a radical shift in the main elements of the central bank’s view. Governor Lowe’s comments were quite clear on this point:

- While noting that the RBA had upgraded its inflation forecasts, he also stressed that ‘we are not expecting the surge in inflation that has been experienced in some other countries. The situation in Australia is different.’

- He emphasised that the RBA still sees the bar for an interest rate hike as quite high: ‘In our central scenario, underlying inflation reaches the midpoint of the two to three per cent range only in late 2023. Having underlying inflation reach the midpoint of the target range for the first time in seven years does not, by itself, warrant an increase in the cash rate. It is also relevant that wages growth at the end of 2023 is expected to be running at three per cent. While this is higher than it is now, it is still below the average over the two decades to 2015. This expected configuration of inflation and wages growth allows the Board to be patient in considering a lift in interest rates.’

- And he continued to (mostly) dismiss the case for a rate hike next year: ‘the latest data and forecasts do not warrant an increase in the cash rate in 2022…some other central banks are raising rates, but our situation is different. The Board will not increase the cash rate until inflation is sustainably in the target range. We are prepared to look through spikes in the inflation rate, as we have done with headline CPI inflation this year. For inflation to be sustainably in the target range, wages growth will have to be materially higher than it is now. This is likely to take time.’

In the Q&A session that followed his presentation, Lowe described current market pricing on interest rates as a ‘complete overreaction’ to recent inflation data and once again emphasised that Australia’s experience to date was unlike that of other countries, with little sign of the emergence of significant wage pressures. He also noted that in the event inflation did surprise on the upside, he anticipated that a modest rise in interest rates would be enough to slow things down given the high level of debt in the economy.

How did markets take this message? They only sort of it bought it. There was a modest fall in the implied profile for the cash rate in the aftermath of this week’s meeting. But market pricing continues to predict a much earlier tightening in monetary policy than is implied by Lowe’s comments – roughly 73bp over the coming year at the time of writing.

All of which suggests that the tug-of-war between Martin Place and financial markets over the future trajectory of inflation and interest rates remains far from settled. Instead, it will continue to depend on the data flow and as noted last week, the upcoming 17 November Wage Price Index (WPI) release is shaping up to be an important data point to watch.

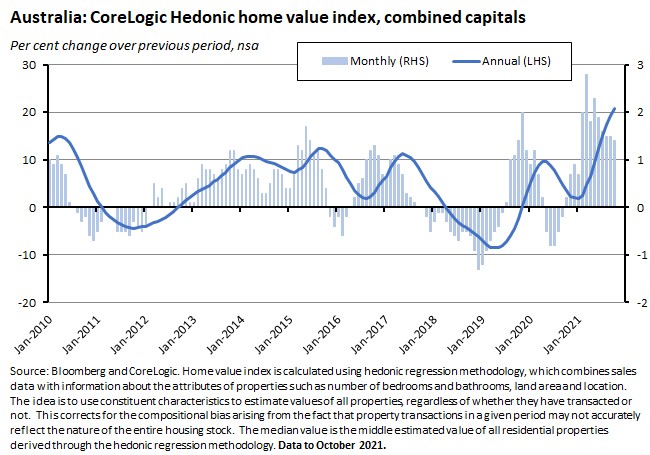

What happened:

CoreLogic’s national housing values index rose 1.5 per cent over the month in October to be up 21.6 per cent in annual terms. The combined capitals index rose 1.4 per cent month-on-month and 20.8 per cent year-on-year.

Dwelling values rose across all the capital cities in October with the exception of Perth, which saw a 0.1 per cent drop. The pace of monthly increase ranged from 0.4 per cent in Darwin to 2.5 per cent in Brisbane, with values up one per cent in Melbourne and 1.5 per cent in Sydney. Dwelling values in Sydney, Brisbane, Adelaide, Hobart and Canberra are now up more than 20 per cent over the past year.

Growth in regional dwelling values again outpaced growth in the capital cities, and growth in housing values continues to run ahead of growth in the units, with the gap particularly large in Sydney (annual rises of 34 per cent vs 13.6 per cent, respectively) and Melbourne (19.5 per cent vs 9.2 per cent).

According to CoreLogic, auction clearance rates, days on market and vendor discounting rates all remain at above average levels, while property listings are now starting to increase, albeit from a very low base and total advertised stock levels have risen above recent record lows.

National rents rose 0.7 per cent in October while gross rental yields have continued to fall, dropping to a record low of 3.27 per cent.

This week also brought a selection of other housing market-related data:

- ABS data on lending in September 2021, which showed a 1.4 per cent monthly decline in new loan commitments for housing, with lending to owner occupiers down 2.7 per cent and lending to investors up 1.4 per cent. In year-on-year terms, new loan commitments for housing were up 35.5 per cent, comprising a 20.8 per cent increase for owner occupiers and an 83.3 per cent jump for investors.

- ABS numbers on building approvals for September 2021 reported that the number of total dwellings approved fell 4.3 per cent over the month, although it was still up 12.8 per cent over the year. Approvals for private houses were down 16 per cent month-on-month and down 2.7 per cent year-on-year, while approvals for private sector dwellings excluding houses jumped 18.1 per cent over the month to be 47.2 per cent higher relative to September 2020.

- RBA data on credit growth in September 2021 showed the monthly rate of growth of housing credit unchanged at 0.6 per cent while year-on-year growth was 6.5 per cent.

For more charts on these releases and on the housing market more generally, please take a look at the updated Housing market chart pack.

Why it matters:

Growth in dwelling values is running at above average rates but month-on-month growth rates have moderated. While CoreLogic still expects values to continue to rise in the short term, it also notes that worsening affordability, rising supply, tighter credit conditions (remember, last month APRA instructed banks to increase the debt serviceability buffer by 50bp) and market expectations of higher interest rates are all now contributing to rising downside risks for the housing sector.

What happened:

ANZ job ads rose 6.2 per cent over the month in October.

Newly lodged jobs also increased over the month, up by 4.9 per cent, led by a near-17 per cent jump in New South Wales.

Why it matters:

After three consecutive monthly falls, the number of job ads is now back where it was in June this year, before the impact of Delta-driven lockdowns hit hiring intentions.

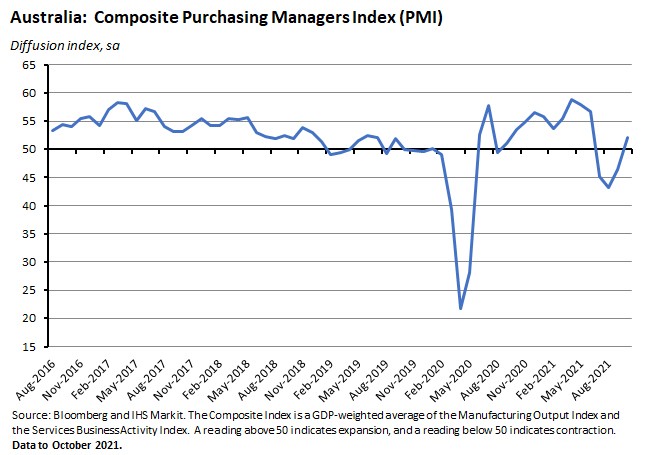

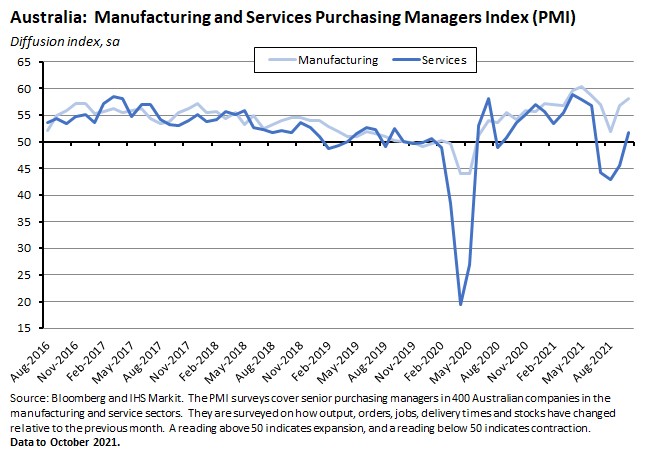

What happened:

The IHS Markit Australia Composite PMI (pdf) rose to 52.1 in October from 45.5 in September.

The marked bounce in the Composite PMI last month reflected a rise in the Services PMI from 45.5 in September to 51.8, while the Manufacturing PMI rose from 56.8 to 58.2 over the same period.

Why it matters:

After having signalled three consecutive months of contractions, the PMI is now indicating that business activity in Australia’s private sector returned to growth in October. That reflects the easing of COVID-19 restrictions on activity which allowed a resumption of service sector activity.

The PMI results also continue to report the presence of significant price pressures in the Australian economy. Manufacturing firms said that suppliers’ delivery times had again lengthened and were now at their worst in one-and-a-half years, reflecting a combination of supply shortages and shipping issues. Firms also noted the persistence of outbound shipping issues, leading to accumulating stocks of finished goods. IHS Markit also said that many firms had reported hiring difficulties as well as an impact from vaccination policies that had caused lower staffing levels. As a result, manufacturing sector input cost and output charge inflation both rose to record rates in October. Similarly, services firms reported that input cost inflation had risen to a three-month high last month, although the rate of output price increase slowed slightly relative to September. Services businesses cited continued price pressures from growth in input, transportation and labour costs.

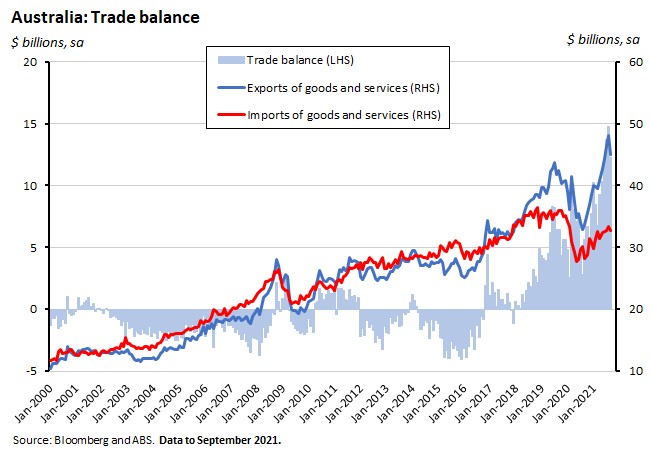

What happened:

The ABS said that Australia recorded a goods and services trade surplus of $12.2 billion (seasonally adjusted) in September this year. Exports of goods and services fell six per cent over the month to just shy of $45 billion while imports of goods and services slipped two per cent over the month to $32.7 billion.

Why it matters:

Australia’s monthly trade surplus slipped back from August’s record outcome, although it still remains substantial by historical standards – the third largest on record.

The fall in export values in September was driven by a $2.9 billion decline in the value of exports of metal ores and minerals, which in turn reflected another drop in the value of iron ore exports. After peaking at around $18.2 billion in June this year, the monthly value of iron ore exports had fallen to less than $12 billion by September. The price of iron ore has fallen from more than US$200/t at the end of June to closer to US$100/t this week.

The fall in imports over the month is further evidence of the impact of global supply chain disruptions and shortages, with the latter contributing to a 38 per cent slump in the value of imports of non-industrial transport equipment.

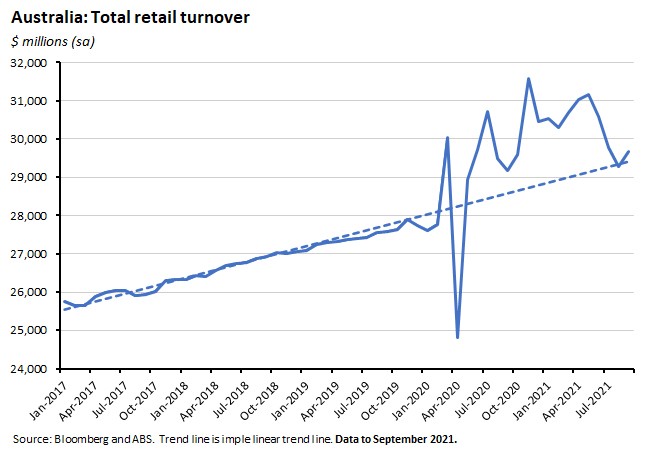

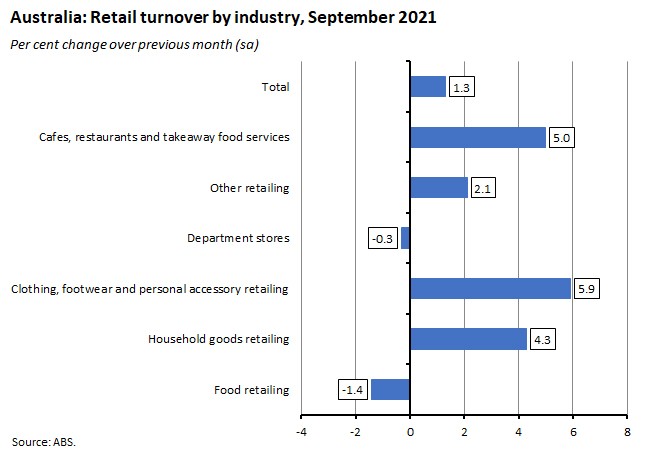

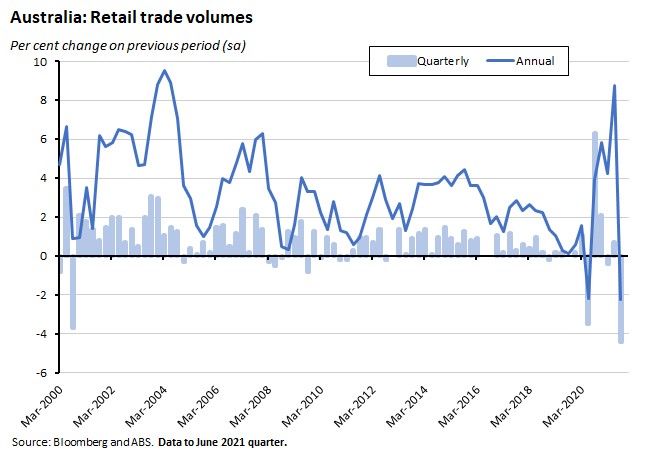

What happened:

According to the ABS, Australia’s retail turnover at current prices rose 1.3 per cent month-on month (seasonally adjusted) in September 2021 to be up 1.7 per cent year-on-year.

Turnover across the month was up in five out of seven industries, with the two exceptions being food retailing (down 1.4 per cent) and department stores (down 0.3 per cent).

For the September quarter as a whole, turnover in volume terms fell 4.4 per cent to be 2.2 per cent lower than in the September 2020 quarter.

Why it matters:

The monthly and quarterly retail trade data show the varying effects of lockdowns.

The monthly numbers for September marked the first month-on-month increase since May this year. Retail sales in Queensland, for example, rose 5.2 per cent to a new record level in September with the state unaffected by lockdowns. Sales in New South Wales also rose over the month, up 2.3 per cent, as some public health restrictions were lifted. But sales fell over the month in Victoria and the ACT where restrictions remained in place.

The quarterly data showed retail sales volumes suffering a record 4.4 per cent drop in Q3:2021 with the ABS reporting that lockdowns saw sharp falls across most of the discretionary spending industries, including cafes, restaurants and takeaway food services (down 18.7 per cent), clothing, footwear and personal accessory retailing (down 25.1 per cent), department stores (down 19.5 per cent) and household goods retailing (down 4.3 per cent). Likewise, there were big falls in volumes in the states most affected by lockdowns: New South Wales (down 11.6 per cent), Victoria (down 4.5 per cent) and the ACT (down 13.9 per cent). In contrast, volumes were up across the other states and territories.

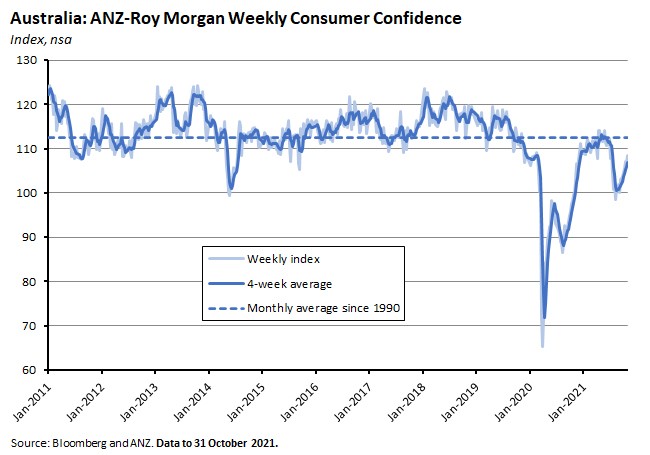

What happened:

The weekly ANZ-Roy Morgan Consumer Confidence Index rose 1.5 per cent last week.

Confidence jumped in Sydney and Melbourne but fell in Brisbane, Adelaide and Perth.

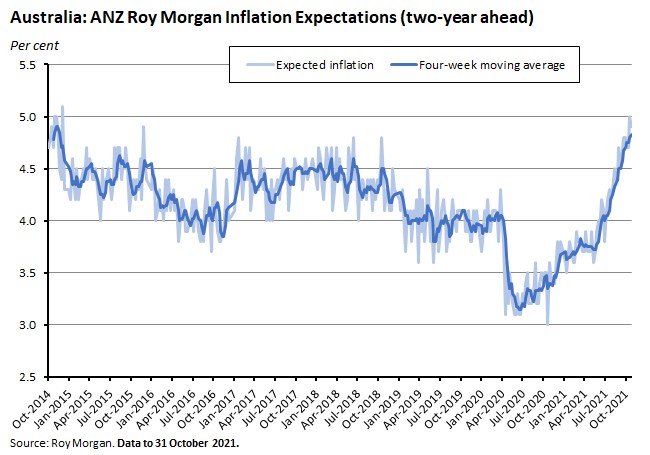

‘Weekly inflation expectations’ eased by 0.1 percentage points to 4.9 per cent.

Why it matters:

Consumer confidence is now back to its highest level since early July this year, consistent with improving sentiment triggered by the economy’s emergence from lockdown.

Inflation expectations fell back slightly from the previous week’s reading of five per cent. At this level, price expectations remain quite elevated relative to recent years but are still significantly below the plus-six per cent readings recorded in 2011 and 2012 and are in line with the levels seen in late 2014.

Selected linkage . . .

- EY examines the importance of COP26 for the Australian economy. The report notes that Australia’s export base has become increasingly reliant on high emission intensity goods (about 85 per cent of the dollar value of Australian exports are in goods within the top 25 per cent of emissions intensity goods), leaving exports significantly exposed to climate actions elsewhere.

- The new Deloitte Access Economics Budget Monitor is out, with goods news and bad news on Australia’s budget position.

- Grattan wraps up its series of papers on climate change policies with a report setting out what it reckons is a practical plan for Australia’s governments to reach net zero by 2050.

- Peter Martin argues that, one way or another, Australia can’t escape a carbon tax. But it can decide whether the proceeds stay here or go overseas.

- Last Friday, the ABS published new annual estimates of key economic data for 2020-21. The Australian economy grew 1.5 per cent in real terms, real GDP per capita rose 0.9 per cent, and labour productivity rose 1.2 per cent. Nominal GDP was up 4.3 per cent and the terms of trade rose 10.3 per cent.

- Updated living cost indexes (LCIs) from the ABS. Increases in transport and housing saw all of the LCIs increase in the September quarter, with annual gains ranging between 2.6 per cent and 2.9 per cent (the CPI rose three per cent over the same period.)

- Also from the ABS, a new research article looks at export and import invoice currencies (an invoice currency is the currency in which an invoice for exported or imported products is denominated, before conversion to AUD). In 2020-21, almost 88 per cent of all merchandise exports were invoiced in US dollars and more than 53 per cent of merchandise imports. By way of contrast, just 0.2 per cent of exports and 1.3 per cent of imports were invoiced in Chinese renminbi.

- The RBA’s November 2021 chart pack is now available.

- The Treasury Secretary’s opening statement to the Economics Legislation Committee. Treasury reckons that GDP will have fallen by about three per cent in the September quarter of this year – the second largest fall in the history of the series, albeit well down on the seven per cent drop recorded in the June quarter last year. But it also thinks that economic activity and the labour market will recover quickly as restrictions are eased.

- The Productivity Commission (PC) examines Australia’s Prison Dilemma: until the pandemic, we were locking up a record number of people (our imprisonment rate was at its highest in a century) despite some evidence of falling crime rates. The PC says that’s down to a mix of changes in the nature and reporting of crime (some types of serious crimes have risen while others have fallen, and reporting of some serious crimes has also increased) as well as changes in criminal justice policy.

- ACCC chair Rod Sims argues that competition in Australia faces big challenges: merger law reform, the ‘need to prove the future’ in competition cases, and the debate over ex ante regulation of some digital platforms.

- A Lowy Interpreter piece on why businesses need to manage rising geoeconomics risks. Related working paper on how Australian export industries responded to Chinese trade restrictions.

- How differences in tax and pension policy shape cross-country patterns of home ownership and wealth: A comparison of Germany, the United States and Australia.

- Bloomberg on the global supply chain crisis.

- Related (1), a WSJ piece on how supply chain uncertainty is encouraging US CEOs to rethink offshoring and outsourcing.

- Related (2), Michael Spence explains why supply chains are blocked. Networks that are optimised to maximise efficiency and minimise waste don’t do a good job of handling major shocks.

- An Economist magazine Special Report on the agenda for this week’s COP26 summit, which has a particular focus on the importance of negative emissions.

- A new OECD report on managing climate risks. It focuses on three types of climate hazards: increasingly frequent and intense extreme weather events; more gradual changes such as rising sea levels; and the global effects of cross critical thresholds in the climate system.

- An FT Big Read on where does all the climate finance money go?

- Rapid growth in US workers wages is not keeping up with inflation.

- Tracking trade from space.

- Forecasting in abnormal times.

- Adam Tooze on how China avoided a Soviet-style collapse.

Latest news

Already a member?

Login to view this content