Australia’s consumer price index fell by a record-breaking 1.9 per cent in the June quarter. Payroll jobs have now fallen for the last three weeks. Consumer confidence continues to erode. Dwelling approvals have fallen to an eight-year low. ABS survey data shows many businesses remain heavily reliant on government and other support measures.

This week’s readings include lessons from Australia’s government debt market during COVID-19, several reviews of this week’s Australia-United States Ministerial Consultations (AUSMIN), an argument that government bailouts and easy money are ruining capitalism, as well as an opposing case for the defence (well, for central banks anyway), a debate on forecasting, probability and the pandemic and political ideas from Hobbes to Fukuyama.

What I’ve been following in Australia . . .

What happened:

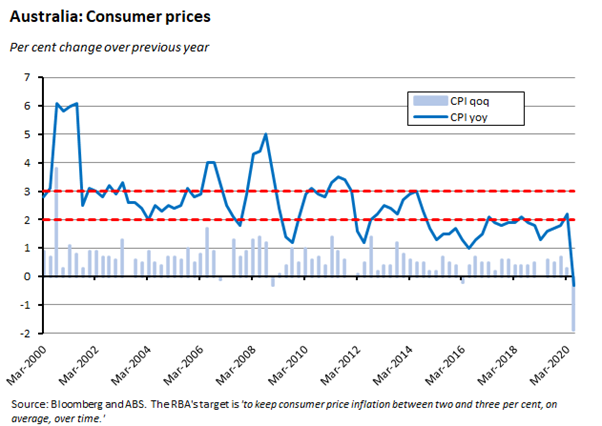

According to the Australian Bureau of Statistics (ABS), the Consumer Price Index (CPI) fell 1.9 per cent in June quarter. In annual terms, the CPI fell 0.3 per cent.

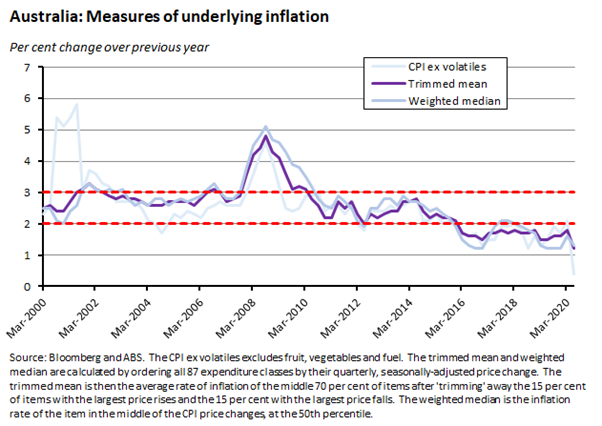

The trimmed mean – the RBA’s preferred measure of underlying inflation – fell by 0.1 per cent over the quarter and rose by 1.2 per cent over the year and other measures of underlying inflation were similarly weak, with the annual rate of increase for the weighted median sliding to 1.3 per cent.

Several factors contributed to the June quarter’s abrupt dip into deflation, including some important methodological changes. Key drivers of the quarterly fall in prices included:

- An 11.2 per cent fall in the furnishings, household equipment and services group. This was mainly driven by a 95 per cent fall in the CPI for childcare services after the government announced on 2 April that they would be free for families from 6 April to 28 June (later extended until 12 July).This had the effect of reducing childcare out-of-pocket expenses for households to zero for most of the June quarter (for a total of 62 out of 65 business days). This factor alone subtracted about 1.1 percentage points from the headline CPI.

- A 6.8 per cent fall in the transport group. This drop largely reflected a19.3 per cent fall in automotive fuel, due to low global demand resulting from COVID-19 restrictions (automotive fuel prices fell 15.9 per cent in April and then only rose 0.9 per cent in May and 9.2 per cent in June).Lower fuel prices subtracted almost 0.7 percentage points from the CPI.

- A fall of 3.7 per cent in the education group. Here the main contributor was a drop of 16.2 per cent in preschool and primary education reflecting the provision of free before- and after-school care and free preschool during term two in NSW, Victoria and Queensland.

- A one per cent fall in the recreation and culture group. This was driven by two per cent falls for domestic holiday travel and accommodation and for international holiday travel and accommodation. Note that both of these categories were imputed off the all groups CPI (that is, prices for these – and some other series including urban travel and sports participation – were treated by the ABS as having a quarterly change equal to that of the headline CPI, rather than being measured).

The Bureau also provided a helpful table showing how these various developments influenced the headline rate:

| CPI exclusion-based measure, June 2020 quarter | ||

| Quarterly change (per cent) | Annual change (per cent) | |

| Headline CPI | -1.9 |

-0.3 |

| CPI ex. Childcare | -0.8 | +0.7 |

| CPI ex. Automotive fuel | -1.3 | +0.5 |

| CPI ex. Childcare & automotive fuel | -0.1 | +1.6 |

| CPI ex. Childcare, automotive fuel & preschool & primary education | +0.1 | +1.8 |

Source: ABS

Other notable declines in the June quarter included a 0.7 per cent fall for the housing group (reflecting sharply lower rents) and a 1.3 per cent drop for the communications group.

Why it matters:

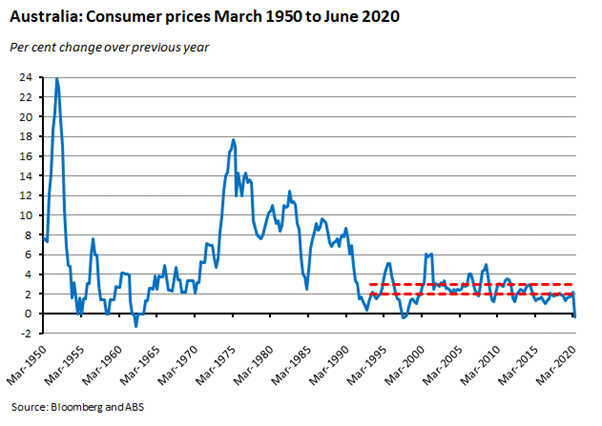

The actual outcome in June was pretty close to consensus: the median market forecast had called for a two per cent fall over the quarter and a 0.5 per cent annual decline. But the fact that it wasn’t a surprise shouldn’t take much away from what was still an historic result, with the ABS pointing out that this was the largest quarterly fall in the 72-year history of the CPI. Moreover, until now there had also only been four previous quarters since 1949 in which the annual inflation rate had been negative and none this century: once in the June quarter of 1962 and then for the three quarters between Q3:1997 and Q1:1998.

Does the drop into negative territory in the June quarter herald the onset of a new era of deflation? Not in the short run. Several factors that contributed the most to falling prices in the June quarter have been reversed in the September quarter, including the ending of free childcare and a recovery in fuel prices. That should be enough to lift the quarterly change in CPI back into positive territory next quarter.

In addition, while it’s true that underlying inflation this quarter was weaker than expected (consensus expectations were for a 0.1 per cent quarterly gain and a 1.4 per cent annual rate for the trimmed mean, for example) the weakness in underlying measures of inflation was partly driven by the ABS decision to include imputed series such as domestic and international travel in its calculations. Excluding those imputed series would have pushed the annual rate of increase for the trimmed mean measure up from 1.2 per cent to 1.5 per cent and the rate of increase for the weighted median up from 1.3 per cent to 1.5 per cent.

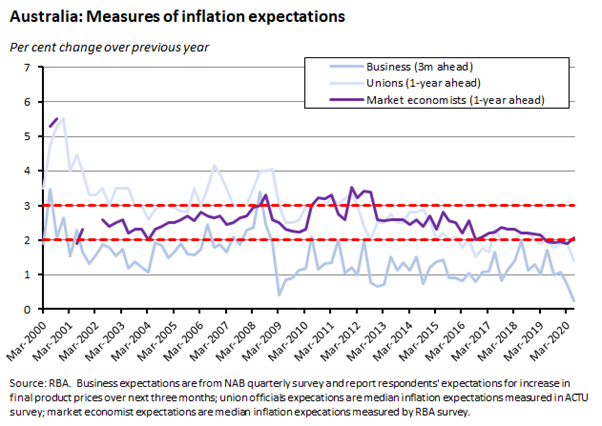

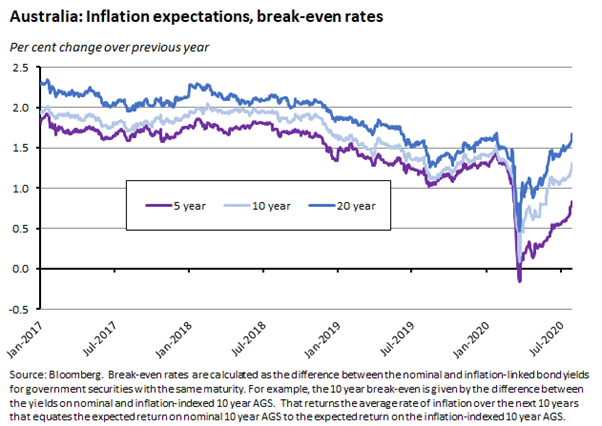

So, next quarter should see the economy back out of its brief deflationary dip. What about the quarters beyond that? For now, overall inflationary pressures look likely to remain very soft, given the large amount of labour market slack (see next story), subdued economic growth and fragile household confidence. That story of ongoing disinflationary forces is also consistent with what most of our measures of inflationary expectations are telling us. Survey-based measures, for example, see inflation at or below the bottom of the RBA’s target band.

And financial market-based measures are also predicting very low rates of inflation.

In the longer term, of course, the outlook becomes much more uncertain as the potential for an inflation regime shift (perhaps sparked by globally higher public sector debt and deficits or by increasingly radical monetary policy choices) becomes more of a consideration to set against sub-par growth and excess capacity.

Finally, this week’s readings also include a couple of interesting pieces on inflation in the time of COVID-19.

What happened:

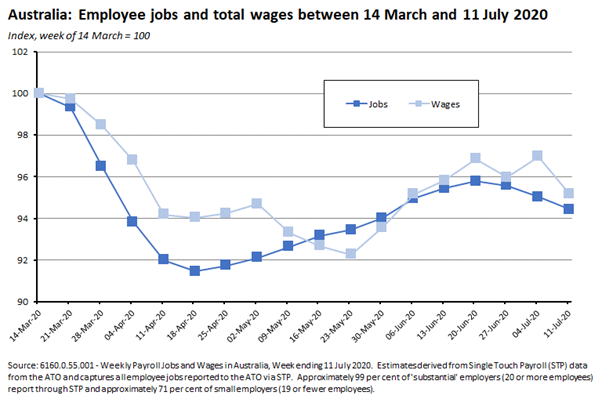

The ABS released the latest data on weekly payrolls, showing that between the week ending 14 March 2020 (the week Australia recorded its 100th confirmed COVID-19 case) and the week ending 11 July 2020, payroll jobs fell by 5.6 per cent while total wages paid declined by 4.8 per cent. Over the most recent week of data, jobs fell by 0.6 per cent and wages fell by 1.9 per cent.

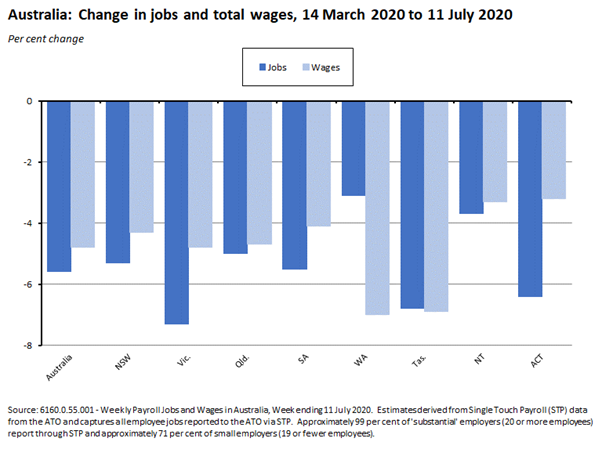

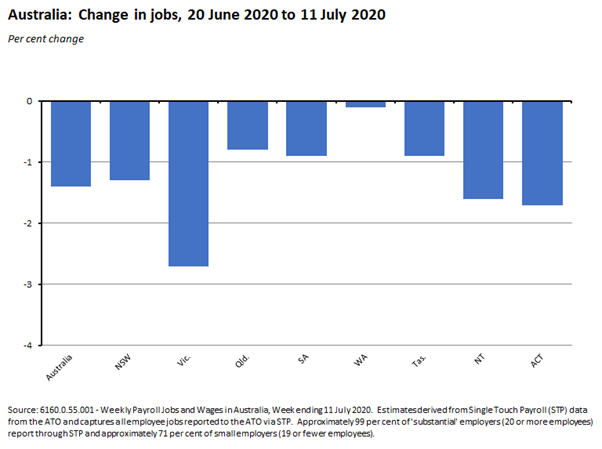

By state, the largest declines over the 14 March to 11 July period for payrolls jobs were in Victoria (down 7.3 per cent), Tasmania (down 6.8 per cent) and the ACT (down 6.4 per cent), while the largest falls in wages were suffered by Western Australia (down seven per cent), Tasmania (down 6.9 per cent) and Victoria (down 4.8 per cent).

The impact of the return of COVID-19 restrictions in Victoria is also apparent in the data: According to the ABS, while total payroll jobs decreased by 1.4 per cent across Australia between mid-June and mid-July, in Victoria the fall over the same period was 2.7 per cent.

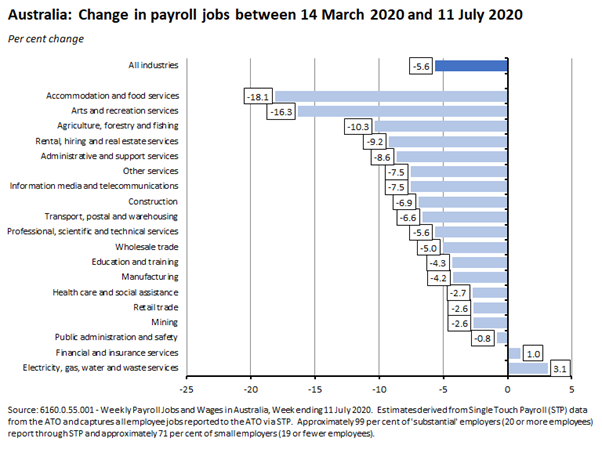

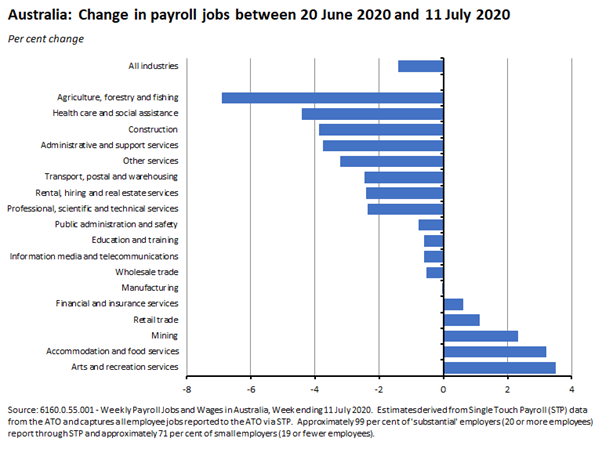

By industry, the largest job losses between 14 March 2020 and 11 July have been a more than 18 per cent fall in the accommodation and food services sector, a more than 16 per cent fall in arts and recreational services and a more than 10 per cent decline in agriculture.

Over the same period, the biggest decline in wages paid has occurred in mining (down 22.6 per cent), in accommodation and food services (down 12.2 per cent) and in rental and real estate services (down 11.8 per cent).

Why it matters:

At the time of the release of the last payroll numbers report (which covered the period up to 27 June), I noted that one potentially worrying sign was that then the most recent weekly numbers had shown payroll jobs falling, suggesting some risk that the initial recovery in employment could be running out of steam. Given the volatility of the weekly payroll numbers and the potential for large revisions, however, I also cautioned against reading too much into one week’s number. Unfortunately, this latest release provides more evidence that the job recovery is struggling.

A look at the chart showing the weekly national index above suggests that the recovery in payroll jobs seems to have reached a peak in the week ending 20 June. Since then, payroll jobs have declined by about 1.4 per cent. Across the states, predictably it is Victoria that has seen the sharpest decline, with a 2.7 per cent fall. But it’s important to note that the shift in the job market story has not been confined to Victoria: every other state has also seen payroll jobs fall over this period (although in Western Australia the decline was marginal at just 0.1 per cent).

Moreover, for the same period, a breakdown of changes by industry shows that the biggest losses were not in the sectors that we’d expect to be most impacted by COVID-related lockdowns (the big losses in accommodation and food services and arts and recreation noted above), with the largest declines instead in agriculture, health care, construction, administrative services and other sectors, suggesting that job losses have spread out to the broader economy. Again, it’s important to note that there are limitations associated with using this new payroll data (for example, the fall in agricultural jobs may be driven more by seasonal factors). Even so, the message on job growth coming from what is now the last two releases is troubling.

What happened:

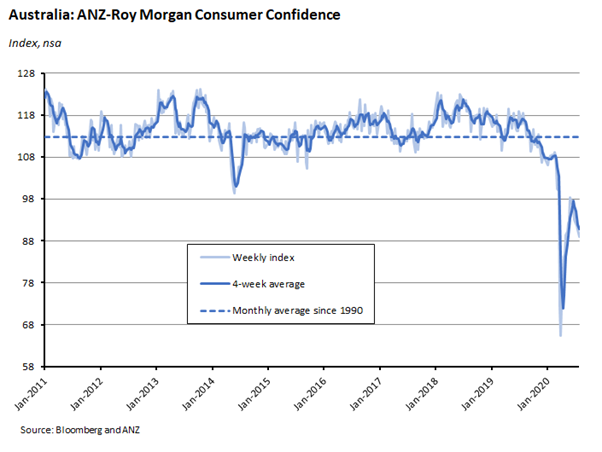

The weekly ANZ-Roy Morgan survey of consumer confidence fell 1.7 points to an index level of 89 this week.

There were weaknesses in all the subindices this week: the fall in ‘current finances’ fell following three weeks of rises, ‘future finances’ fell for a third consecutive week, ‘current economic conditions’ fell for a sixth straight week, and ‘future economic conditions’ declined, as did ‘time to buy a household item.’

Why it matters:

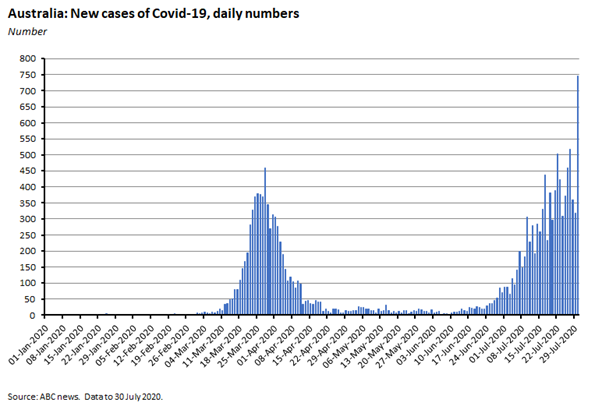

This result marks the fifth consecutive weekly decline for consumer confidence, with the index now at its lowest since late April. The high level of COVID-19 case numbers in Victoria and the rise in case numbers in NSW are the most obvious drivers of this fall, although it’s also possible that this week’s drop in the confidence regarding current economic and financial conditions may have been influenced by last week’s announcements paring back JobKeeper and JobSeeker payments.

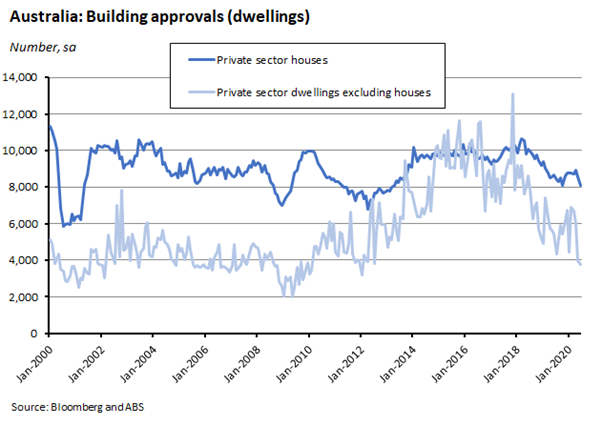

What happened:

The ABS reported that the total number of dwelling units approved in June fell 4.9 per cent over the month (seasonally adjusted) to be down 15.8 per cent over the year. Approvals for houses fell 5.7 per cent over the month and seven per cent over the year, while approvals for dwellings excluding houses fell 5.3 per cent over the month and slumped 30.5 per cent in annual terms.

Approvals fell across all states, with double-digit falls in NSW (down 14.8 per cent), Western Australia (down 11.7 per cent), Queensland (down 10.9 per cent) and Tasmania (down 10.8 per cent).

The ABS also said that the value of alterations and additions to residential building rose 11.4 per cent (seasonally adjusted) in June.

Why it matters:

Dwelling approvals are now at an eight-year low, with the Bureau noting that the impact of COVID-19 was ‘evident’ in the steep fall in June numbers.

What happened:

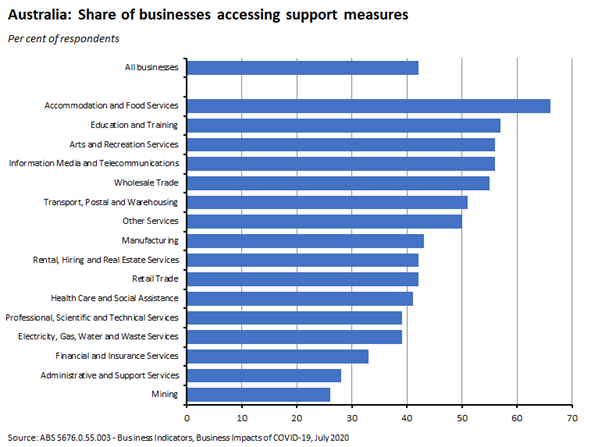

The ABS published the results of its sixth survey covering the business impacts of COVID-19. July’s survey topics included developments in business revenue, operating expenses and employment, government support measures used by businesses and the expected actions firms will take when they are no longer available, and workforce difficulties experienced by employing businesses.

According to the survey, 70 per cent of all Australian businesses are still operating under modified conditions, with that share rising from 69 per cent of small businesses to 83 per cent of medium and large businesses. The Bureau reported that 42 per cent of Australian businesses are currently accessing at least one of a range of support measures including wage subsidies, deferred loan repayments and renegotiated rental or lease arrangements, to manage the impacts of the COVID-19 pandemic, with 53 per cent of medium businesses accessing support measures, compared to 42 per cent of small businesses and 38 per cent of large businesses.

By sector, the share of businesses accessing support ranged from 66 per cent of businesses in accommodation and food services to 26 per cent of mining businesses.

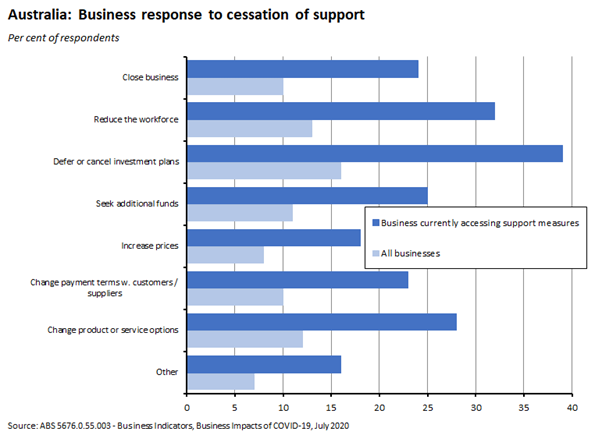

The survey also investigated the potential impact of the cessation of this support, finding that of those businesses currently receiving some form of support, 32 per cent said they would reduce their workforce when support ceased, 39 per cent would defer or cancel investment plans and 24 per cent said they would close their business.

Why it matters:

Last week’s note discussed the government’s plans to extend some elements of the COVID-19 support package, in particular JobKeeper. This week’s ABS business survey is another reminder that a significant share of the economy remains dependent on one or more of the current support measures and therefore when that support is wound back there are likely to be significant consequences in terms of business closures and job losses.

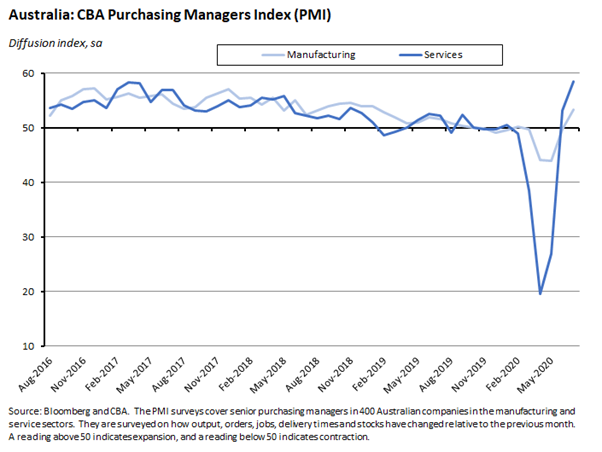

What happened:

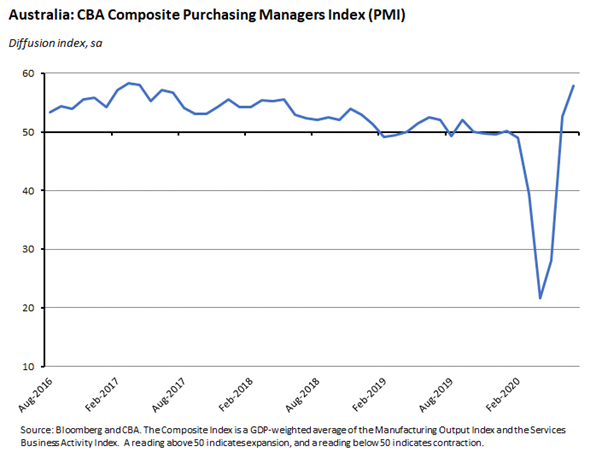

Last Friday, CBA said that its ‘Flash’ Purchasing Managers Index (PMI) for July rose to 57.9, up from 52.7 in June. (The ‘Flash’ PMI is a preliminary result based on around 85 per cent of final survey responses).

Sitting behind the composite index, the Services Business Activity Index jumped 5.4 points to 58.5 while the Manufacturing PMI rose 2.2 points to 53.4.

Why it matters:

The sizeable increase seen in July’s preliminary PMI reading suggests that overall business activity continued to strengthen in July, with services activity again leading the way with a second big consecutive monthly rise. That in turn implies that the lifting of restrictions on activity across the rest of Australia has so far outweighed the adverse consequences of renewed lockdown in Victoria. That’s good news, although as CBA’s economics team notes (and as we stressed with last month’s results) it’s also important to remember that the PMI survey is a measure of the monthly change in activity, not its level, and that the large falls in activity in April and May mean that even after the strong results we’ve seen in June and July, the current level of activity is still below pre-COVID levels.

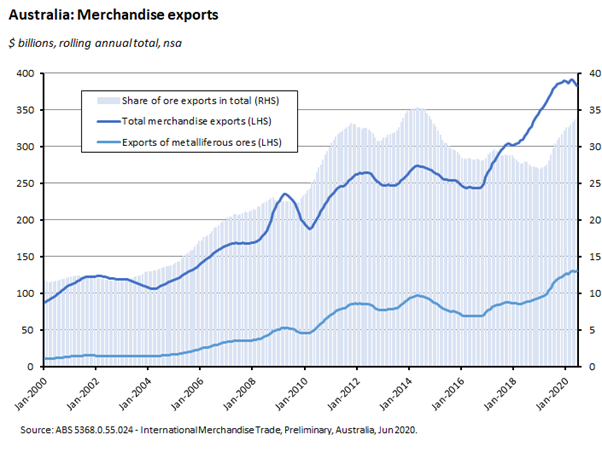

What happened:

At the end of last week, the ABS released preliminary estimates for merchandise trade in June. The numbers show the value of exports and imports of goods both increased last month, with exports up eight per cent over the month (but down 10 per cent relative to June 2019) and imports up six per cent in monthly terms (but down two per cent over the year).

That eight per cent increase in June exports followed two months of falling export values and was driven by a combination of stronger exports of non-rural goods (up six per cent), rural goods (up one per cent) and a 67 per cent jump in the value of exports of non-monetary gold. The main driver of the monthly rise in dollar terms was exports of metalliferous ores, which were up $1.2 billion (11 per cent) to hit a record high export value of $12.5 billion. For the 2019-20 financial year, the value of ore exports exceeded $130 billion, of which more than $100 billion was accounted for by iron ore.

The monthly rise in imports was driven by increase in imports of consumption goods (up 13 per cent), intermediate and other goods (up eight per cent) and capital goods (up four per cent).

By direction of trade, China was once again Australia’s most important trading partner in 2019-20, the destination for 39 per cent of our exports and the source of 27 per cent of our imports.

Why it matters:

The preliminary results for 2019-20 serve as useful reminder of the continued and interlinked importance of iron ore and China in Australia’s merchandise export portfolio. At more than $100 billion, exports of iron ore accounted for more than a quarter of Australia’s total goods export last financial year, of which China was the destination for 87 per cent, as well as for 39 per cent of all goods exports.

What I’ve been reading:

Treasury Secretary Stephen Kennedy appeared before the Senate Select Committee on COVID-19 this week. His opening statement is here. Dr Kennedy argued that, ‘The management of the pandemic from a health perspective will continue to underpin economic recovery and the effectiveness of economic policy responses…with falls in travel and public activities typically preceding government decisions to increase restrictions [emphasis added].’ He also built on the message delivered by RBA Governor Lowe in his speech last week (and discussed in detail in last week’s note), setting out the case for a relatively greater reliance on fiscal policy given current conditions. The Treasury Secretary said that, ‘While actions taken by the RBA are assisting the economy, they are not providing anywhere near the amount of support that they have in the past… From a fiscal perspective, this means more is going to be expected of governments and fiscal policy in managing economic cycles…fiscal policy will be more powerful in these settings. It is highly likely that fiscal multipliers are larger when interest rates are near zero and are expected to remain there for the foreseeable future. In other words, the usual crowding out features of fiscal policy are much less pronounced.’

Related, the Treasurer gave a speech to the National Press Club last Friday.

Also related, Rob Nicholl, CEO of the Australian Office of Financial Management (AOFM) set out what the AOFM has learnt from the past few months and how it is responding to new circumstances. Nicholl notes that in the space of less than six months, the AOFM has gone from ‘rationing issuance to best manage a market maintenance objective’ to doing ‘little more than mull plans to accommodate the complete opposite.’ The current plan is for gross Treasury Bond issuance this year of around $240 billion, comprising about $50 billion to fund maturing debt and $190 billion of net new issuance.

From last Friday, a helpful graphical summary (pdf) from the Parliamentary Budget Office on the July Economic and Fiscal Outlook.

The ABS has released the eighth in its series of surveys on the impact of COVID-19 on Australian households. Findings this time include: almost one in five Australians expect it will take over a year before life returns to normal while one in eleven think it will never return to normal (note: the ABS says that the definition of ‘normal’ was left to the respondent although if asked, the interviewer gave examples such as "your life before COVID-19" or "before the 1st March"); roughly one in 13 Australians are unsure how long it will take for life to return to normal but that share rises to one in six for Victorians; and only one in 50 people in Victoria reported life had either already returned to normal or had not changed compared to more than one in five for the rest of Australia.

Assistant RBA Governor Chris Kent spoke on the Reserve Bank's Operations – Liquidity, Market Function and Funding.

This week’s AUSMIN meeting has produced a flow of commentary. Here is Geoffrey Barker’s take for ASPI’s The Strategist, here is Hugh White in the AFR, and here are Ashley Townshend and Brendan Thomas-Noone for the US Studies Centre.

Related, Heath Baker in the Lowy Interpreter on how Australia should think about managing China economic risk.

This paper in the BIS bulletin series looks at how COVID-19 has produced some dramatic shifts in the key drivers of inflation and created an increase in inflation tail risks.

On using real-time scanner data to track (UK) consumer goods inflation: the data show ‘an unprecedented inflationary spike’ between March and April.

Greg Ip in the WSJ considers how the United States might learn to live with COVID-19.

Also from the WSJ, Ruchir Sharma argues that easy money and government bailouts are ‘ruining capitalism’ by distorting the price signals required for the efficient operation of free markets.

A different take on the same issue: in the FT Robin Harding makes the case that central bankers are being unfairly blamed for a range of pathologies (unaffordable house prices, zombie companies, booming stock markets, growing inequality, terrible returns on savings) including many of those cited by Sharma, when the real culprit behind the low interest rates that drive many of these developments is a fall in the natural rate of interest, likely due to demographic and productivity trends.

A couple of VoxEU pieces on sick leave and pandemics. Adam Tooze in the LRB ponders whose century is it? Nouriel Roubini revisits his ‘White Swans of 2020’.

This is from last month, but I only just came across it: The International Institute of Forecasters put together a debate between John P. Ioannidis and Nassim N. Taleb on COVID-19. The page includes links to both the blog posts and the supporting papers. I found this because Taleb was also the guest on the latest edition of the EconTalk podcast, where he talks about probability and the pandemic.

Another late discovery: I’m a longstanding fan of the Talking Politics podcast. But I’ve only recently binge-listened (is that a thing?) David Runciman’s History of Ideas. All the episodes are interesting, but if you don’t want to work through everything, I’d suggest listening to the opening podcast on Hobbes and the final one on Fukuyama, with (my bias showing now) possibly Hayek and Marx ‘n Engels as chasers.

Latest news

Already a member?

Login to view this content