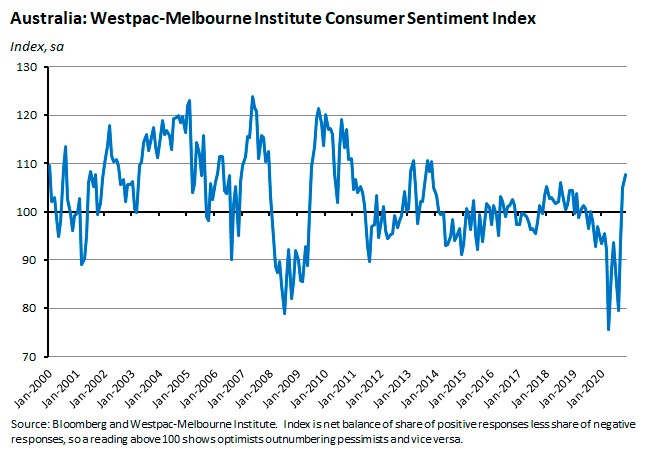

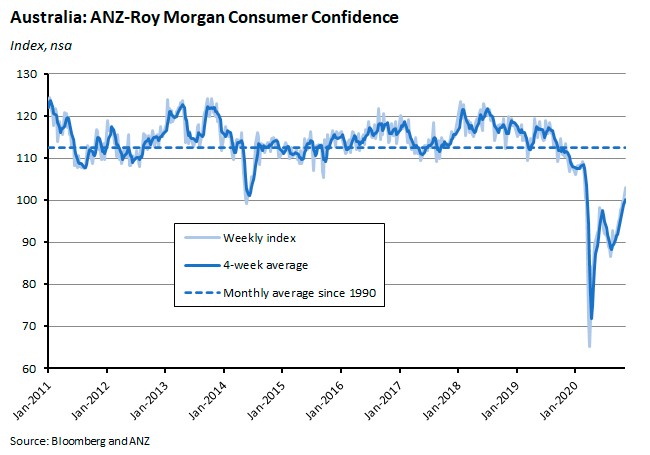

The monthly Westpac-Melbourne Institute Index of Consumer Sentiment rose to a seven-year high in November, while the weekly ANZ-Roy Morgan Consumer Confidence Index recorded a tenth consecutive increase to return to positive territory for the first time this year.

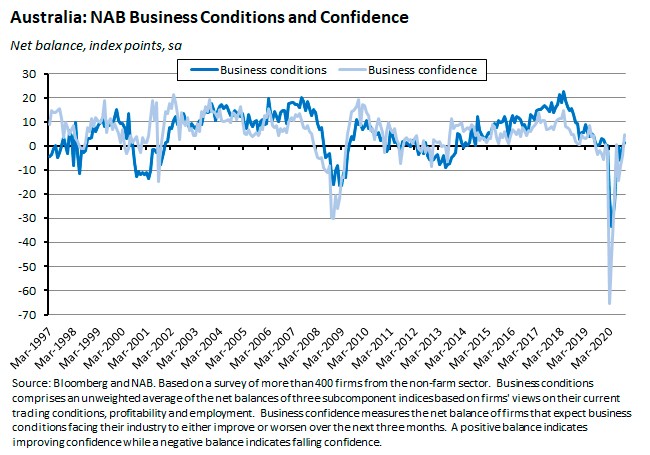

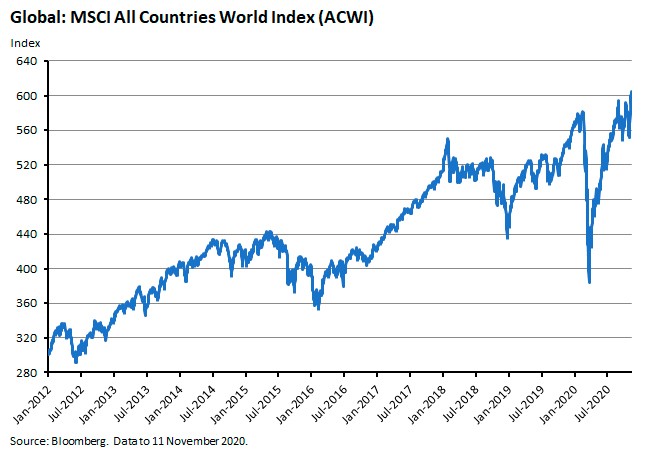

And the NAB monthly business survey for October reported that business confidence is now at its highest level since mid-2019. Last Friday’s release of the November Statement on Monetary Policy from the RBA showed that the central bank has also become more positive on the outlook, with upgrades to its forecasts for growth and employment. The general sense of optimism has also been furthered by this week’s good news on the prospects for a vaccine against COVID-19 – which has pushed global share prices up to a record high. Meanwhile, however, rising case numbers and renewed lockdowns are pulling down economic activity in several major economies.

This week’s readings include the challenges facing Australia-China trade, the excessive costs of mega-projects, a symposium on economics and epidemiology, lessons from the 1932 Hoover-Roosevelt presidential transition, four scenarios for a post-pandemic world, and the top ten emerging technologies of 2020.

What I’ve been following in Australia . . .

What happened:

The Westpac-Melbourne Institute Index of Consumer Sentiment climbed 2.5 per cent to an index level of 107.7 in November.

By subcomponent, the biggest increases over the month were an 8.4 per cent bounce in the ‘economy, next 12 months’ subindex and a 6.7 per cent gain in the ‘time to buy a major item’ subindex.

Sentiment surged by nine per cent in Victoria following the relaxation of restrictions across the state and the reopening of the Victoria-New South Wales border.

Separately, the ‘time to buy a dwelling’ index rose eight per cent to 132, marking its highest reading since November 2013.

Why it matters:

Although November’s 2.5 per cent rise in the sentiment index was a relatively modest gain following an 18 per cent jump in September and an almost 12 per cent rise in October, the cumulative increases have now taken the index back to its highest level since November 2013, marking a seven-year high. Fiscal largesse, easy money and good news on the public health front have all supported consumer sentiment over the past three months. At the same time, the big increase in the ‘time to buy a dwelling’ index is also consistent with the recent run of strong housing market indicators we discussed in the previous Weekly.

Note that the November survey was conducted over 2–8 November, and therefore before the second round of easing restrictions had been announced for Melbourne (and, of course, this week’s good news on a vaccine) but during the week that the RBA announced another cut to the cash rate and the start of its new program of asset purchases. That suggests scope for a further gain in sentiment next month.

What happened:

The ANZ Roy Morgan weekly consumer confidence index rose 3.2 per cent to an index level of 103.1 on 7/8 November.

The main driver of this latest weekly rise was a ten per cent jump in the ‘time to buy a major household item’ subindex.

Why it matters:

Consumer confidence has now risen for ten consecutive weeks and is back in positive territory for the first time since March this year with the highest weekly reading in more than eight months.

Also worth noting: last week’s sharp drop in the ‘current financial conditions’ subindex, which had raised some concern that cutbacks to payments under the JobKeeper and JobSeeker programs might have have started to undermine consumer finances, was reversed this week with a rise in the subindex.

What happened:

The NAB Monthly Business Survey showed business confidence in October jumping by nine points to a reading of plus five index points. Business conditions rose by one point to plus one index point.

According to NAB, business confidence improved in the eastern states, led by gains in Victoria, but declined across Western Australia, Tasmania and South Australia. In trend terms, however, confidence remains most favourable in Western Australia and weakest in Victoria.

Business conditions rose sharply in Victoria and there were also increases in New South Wales and Tasmania while Western Australia, South Australia and Queensland all saw conditions weaken in October. Despite the big monthly gain, conditions in Victoria remain the weakest in trend terms, while conditions are strongest in Tasmania and Western Australia.

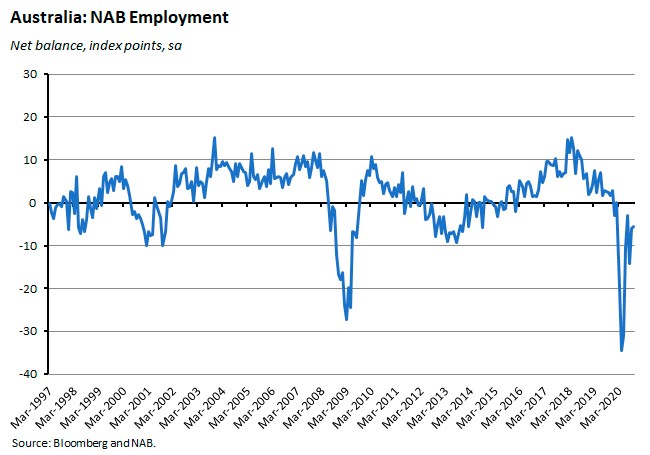

The NAB employment index remained in negative territory at minus five index points in October, edging up from minus six points in September.

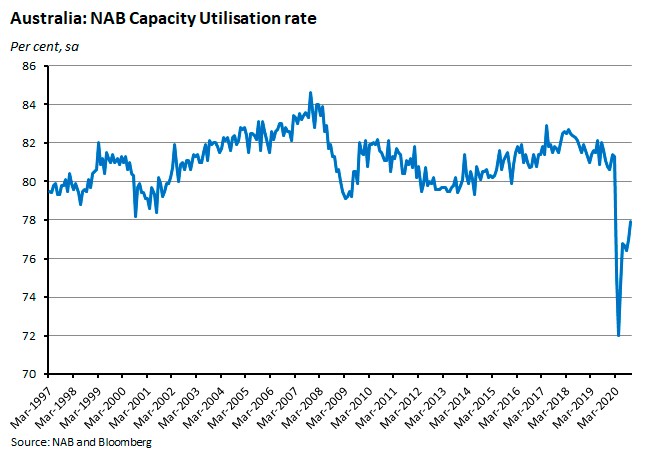

The rate of capacity utilisation rose from 77 per cent in September to 77.9 per cent in October.

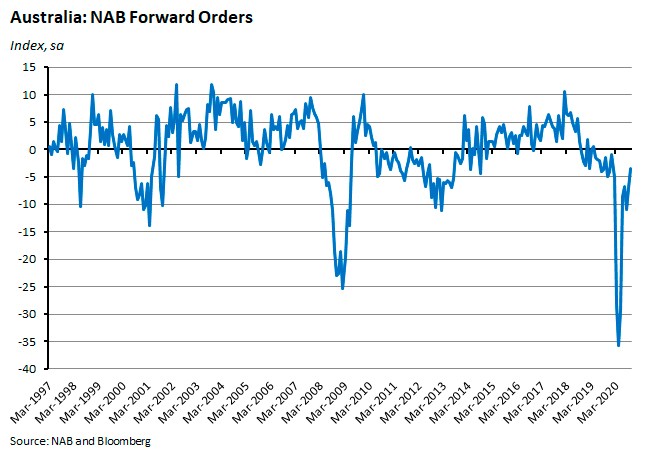

Forward orders rose from minus seven index points in September to minus four index points in October.

Why it matters:

October’s survey results showed business confidence and conditions both strengthening as the economy entered the final quarter of 2020. Indeed, business confidence is now at its highest level since mid-2019, driven this month by large gains in Victoria, likely reflecting falling case numbers and the approaching end of lockdown. While the monthly improvement in business conditions was more modest, that indicator too is now in positive territory, with October’s rise likewise reflecting another large gain in Victoria.

The readings on employment (suggesting continued job-shedding), capacity utilisation (still below pre-pandemic levels) and forward orders (still in negative territory) all suggest that we’re still some way off from a full recovery, however.

What happened:

Last Friday, the RBA published the November Statement on Monetary Policy (SoMP), including its updated forecasts for the Australian economy. According to the central bank, the ‘baseline scenario for GDP growth has been upgraded a little relative to the August Statement. This reflects stronger-than-expected household consumption and additional policy support (including that announced in the Australian Government Budget), though a downward revision to resource exports has partly offset the firmer outlook for domestic demand.’

As a result, the RBA now thinks that, after contracting by four per cent over 2020 as a whole, real GDP will average three per cent over 2021 and four per cent over 2022. The upgrade to the growth forecast next year implies that GDP will be back at its end-2019 level by the end of 2021 (although that would still leave output well short of the path expected prior to the outbreak of the pandemic). The RBA also continues to warn that ‘the recovery can be expected to be bumpy and uneven, and highly sensitive to further virus outbreaks.’

Source: RBA Statement on Monetary Policy November 2020.

The stronger forecast profile for economic growth is accompanied by a more positive outlook for unemployment. Instead of hitting ten per cent in December 2020, the unemployment rate is now predicted to peak at a little below eight per cent before gradually declining to six per cent by the end of 2022. In addition, the RBA also judges that ‘[s]ubstantial spare capacity, including high underemployment, is likely to keep wages growth and inflation low for a considerable period’ with the annual rate of increase in the Wage Price Index (WPI) expected to still be less than two per cent by end 2022. As a result, the RBA’s forecasts for inflation are little changed relative to those included in the August SoMP, with both underlying and headline inflation expected to rise only gradually, reaching an annual rate of just 1.5 per cent by end 2022.

As has become recent practice in response to the uncertainty triggered by COVID-19, the RBA again reported two alternative scenarios to accompany its baseline projections. The baseline numbers are underpinned by the assumption that there are no large additional outbreaks (plus accompanying strict containment measures) in Australia, allowing a continued, gradual easing of national restrictions while restrictions on international travel are assumed to stay in place until around the end of next year. In contrast, the RBA’s downside scenario involves Australia suffering from further major outbreaks of COVID-19 while there is also a loss of control of the virus in other economies. That leads to renewed lockdowns and additional delays in international opening, with adverse consequences for confidence. As a result, the recovery is much slower than in the baseline forecast and the unemployment rate peaks at around nine per cent in late 2021 before declining only modestly in 2022. More positively, the RBA’s upside scenario notes that a stronger economic recovery than that presented in the baseline is also possible, conditional on further progress in the medical treatment and control of the virus leading to a more rapid withdrawal of containment measures. In this scenario, the unemployment rate could peak at 7.5 per cent before declining to 5.5 per cent by the end of 2021.

The November SoMP also reinforces the RBA’s recent messaging around the future trajectory of monetary policy, making three key points:

- ‘The Board is not contemplating a further reduction in interest rates…interest rates have been lowered as far as it makes sense to do so in the current environment. The Board considers that there is little to be gained from short-term interest rates moving into negative territory and continues to view a negative policy rate as extraordinarily unlikely.’

- ‘The Board has committed not to increase the cash rate target until actual inflation is sustainably within the target range of two–three per cent. This will require a period of strong employment growth and a return to a tight labour market.’

- ‘The focus over the period ahead will be the government bond purchase program. If the circumstances require, the Board is prepared to do more and undertake additional purchases.’

These points echo the messages delivered in recent RBA communications.

Why it matters:

November’s SoMP came hot on the heels of the RBA’s latest package of policy measures and reveals how the decision to cut the cash rate and yield target to just 0.1 per cent while embarking on a $100 billion program of QE relates to the central bank’s economic outlook.

Here, the good news is that the RBA thinks the current combination of fiscal and monetary stimulus along with the relaxation of public health restrictions in Melbourne mean that the economy is on track to do better than it was expecting back at the time of the August SoMP. Year-end ‘growth’ in the December quarter of this year is now expected to be minus four per cent instead of minus six per cent and the RBA has also sliced two percentage points off its forecast for the average unemployment rate across the same quarter.

The not-so-good news is that even with the benefit of all this policy largesse, the economy will not return to its 2019 level of output until the end of next year, unemployment will remain elevated, and inflation and wage growth will still be subdued. Granted, better-than-expected news on the health front could see an improvement on that performance and this week’s news on a vaccine does improve the odds of a better outcome (see story below). But it’s also the case that in the meantime, the economy will remain vulnerable to setbacks, whether in the form of COVID-19 or due to other adverse external shocks.

What happened:

The government said that it would extend the Coronavirus Supplement to JobSeeker through to the end of March next year. However, the rate of payment of the supplement will be cut from its current level of $250/fortnight to $150/fortnight.

The extension of the reduced supplement payment over the additional three months is estimated to cost $3.2 billion.

Why it matters:

Back when it was originally introduced early in the pandemic, the Coronavirus Supplement to JobSeeker was set at an additional $500/fortnight with effect from 27 April. This payment was later lowered to $250/fortnight with effect from 24 September and he government said that the new, lower payment would run only until the end of this year, although Canberra also said that it was minded to extend some element of additional support into 2021. This week’s announcement combines the promised extension of support with a reduction in the generosity of the payment.

By providing a substantial cash injection to Australians with a high propensity to consume, the Coronavirus Supplement (together with the JobKeeper program) has acted both as a significant anti-poverty weapon and as an important source of economic stimulus that has helped buttress consumer spending. There had been some concern that with the supplement due to expire in December, both of these effects would be unwound. This week’s announcement means that those fears have now been partially offset.

The announcement provided no insight into the longer-term future of the level of JobSeeker payment, however. Here, there is a longstanding case for a more generous level of support, as the pre-pandemic level of payments under JobSeeker and its predecessor Newstart have failed to keep pace with the general rise in Australian living standards for about a quarter of a century. That has resulted in the value of the payment declining relative to the median wage, the minimum wage and the age pension.

. . . and what I’ve been following in the global economy

What happened:

Global markets surged to a record high earlier this week on news that Pfizer and BioNTech had announced that their COVID-19 vaccine was more than 90 per cent effective in preventing COVID in its phase three trail, the final stage before commercial licensing (by way of comparison, the annual flu shot is typically put at around 40 per cent to 60 per cent effectiveness in a given year). Press reports suggested that the vaccine could be submitted to authorities for emergency approval later this month. Pfizer and BioNTech said that up to 50 million doses of the vaccine could be manufactured this year and a further 1.3 billion doses in 2021.

The initial market reaction was to push up the price of sectors and industries that have suffered most from the pandemic (airlines, hotels, hospitality and aircraft manufacturers all gained, along with energy and financial groups) while businesses that have been relative winners from COVID-19 (meal delivery firms, videoconferencing services and other technology businesses) saw significant profit taking and price drops.

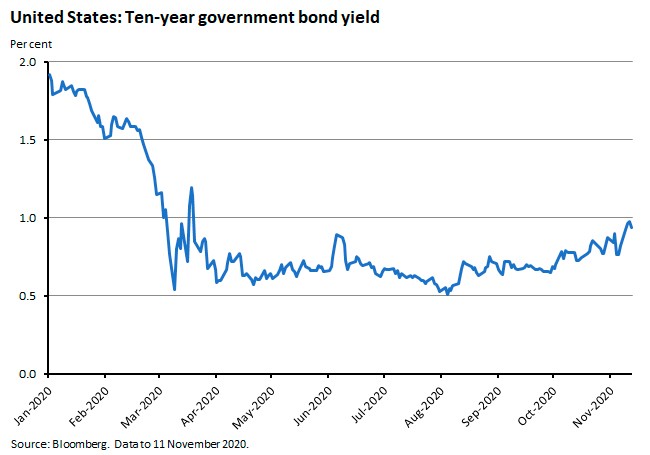

The news also prompted a sharp rise in the ten-year US Treasury yield as bond markets priced in a greater chance of a sustained economic recovery.

Why it matters:

The prospect of significant progress in controlling the pandemic via a successful vaccine has provided a major boost to market confidence, prompting investors to begin pricing in a return to something that looks a bit more like pre-COVID normality. With high levels of uncertainty around the trajectory of the pandemic and the consequent risk of a series of ‘stop-go’ mini-economic cycles driven by the threat of repeated voluntary and involuntary closing and re-opening of economies as case numbers waxed and waned, a vaccine offers the global economy the best prospect of a sustained economic recovery.

Of course, final authorisation of the vaccine is still pending and even then there remain significant unknowns around the timing and impact, not least related to the breadth and speed of any roll out, which will play a large role around determining how quickly any successful vaccine will slow the pandemic.

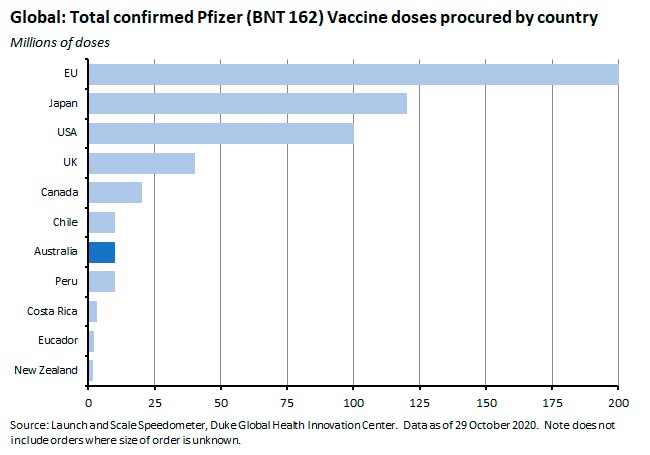

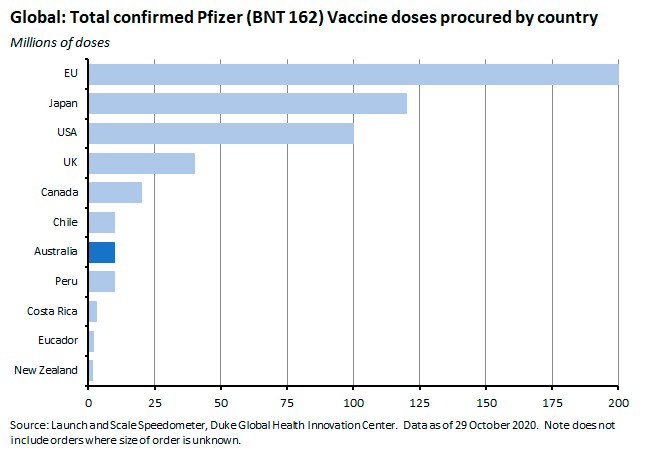

Here, it’s worth noting that several economies, including Australia, have already ordered large quantities of several of the vaccines currently under development around the world. For example, the Duke Global Health Innovation Center estimates that a subset of countries have pre-ordered around 3.8 billion doses of vaccine, with a further five billion doses either under negotiation or reserved as optional expansions of existing deals. But the Center also estimates that coverage of the global population will not be possible until around 2024.

In the specific case of the Pfizer and BioNTech vaccine, countries and regions with significant advanced purchases include the EU, Japan, the United States, the United Kingdom, Canada and Australia.

Given the uncertainty around timing, even under the best case scenario, the new vaccine will not arrive in time to make a significant dent in the (northern) winter wave of coronavirus infections currently sweeping through Europe and the United States, and which is already acting as a substantial drag on activity in some advanced economies (see next story). In the meantime, though, it’s possible that the optimism generated by news of the vaccine will help lift business and household confidence and therefore have positive economic effects beyond the share market rally.

What does the improved likelihood of a vaccine mean for economic forecasts for Australia such as the RBA projections discussed above and the assumptions underpinning Budget 2020-21?

As noted in the story on November’s SoMP, the RBA’s baseline forecast assumes that there are no large additional virus outbreaks (and therefore no accompanying strict containment measures), allowing a continued, gradual easing of national restrictions, while the upside scenario allows for further progress in the medical treatment and control of the virus and therefore a faster withdrawal of containment measures. Treasury’s view as set out in the budget papers was that a ‘population-wide Australian COVID-19 vaccination program is assumed to be fully in place by late 2021’ while the upside scenario notes that an ‘earlier roll-out of a vaccine from 1 July 2021 would provide certainty for both households and businesses, helping support stronger consumption and investment.’

This week’s news tells us that the odds of Australia enjoying something that looks more like the RBA and Treasury upside scenarios have increased, although a cautious reading of the likely timeline for a significant deployment of the vaccine would suggest that the baseline scenarios remain the more likely outcome.

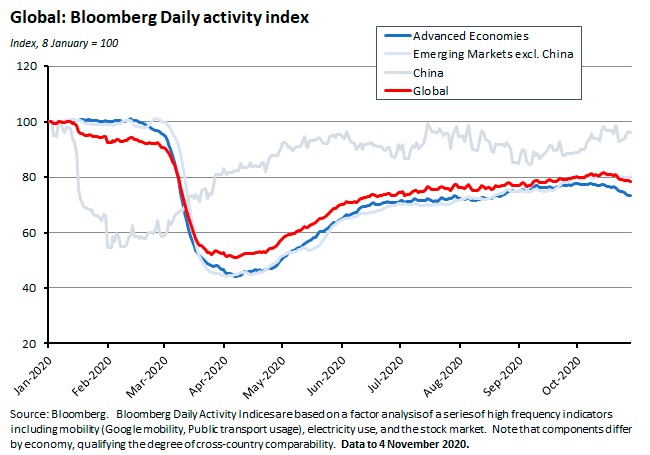

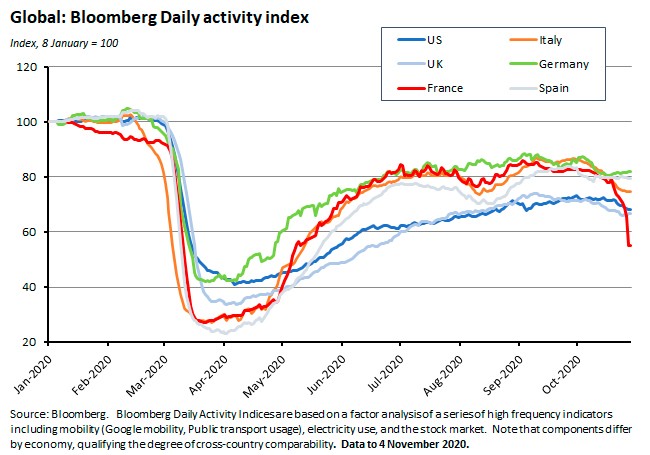

What happened:

Alternative data produced by Bloomberg Economics suggest that several major advanced economies have seen activity slow from around mid-October as coronavirus case numbers have risen and new lockdowns have been imposed.

There has been a particularly large decline in the daily activity index for France along with a marked downturn in Italy, while other advanced economies have also suffered some loss of momentum.

Why it matters:

As we’ve noted before, one of the features of the post-pandemic economic landscape has been an increased focus on so-called alternative data to provide a more contemporary read on economic developments than that offered by more traditional economic statistics. Bloomberg Economics have compiled a series of these alternative indicators for more than 20 of the world’s largest economies and created a daily activity index. These new estimates come with some health warnings attached, however: the relatively high reliance on transport and mobility indicators means that the index likely overweights the importance of mobility, for example, while cross-country comparisons are limited by (1) the likelihood that different economies will have different relationships between mobility and activity and (2) the fact that different national indices use different indicators, partly reflecting different data availability. Even so, statistical back testing by Bloomberg suggests that their indicators have done a decent job in capturing the developments that subsequently appeared in official Q2 and Q3 GDP readings.

The latest batch of activity index readings based on these alternative data sources suggest that the combination of more COVID-19 cases and more national lockdowns has started to drag down mobility and overall activity in several key advanced economies, and that this in turn is pulling down overall global activity.

Finally, note the different message here compared with last week’s relatively upbeat results from the composite global PMI. The latter had hit a 26-month high in October, signalling the fastest rise in global activity in more than two years. The alternative data are sending a rather different signal, flagging the risk of a downturn in the final quarter of this year (a COVID winter in the Northern Hemisphere) following what had been a relatively strong third quarter. Part of this may reflect differences in timing, with the alternative data showing the slowdown in activity starting from the middle of last month.

What I’ve been reading . . .

Treasury Secretary Stephen Kennedy’s speech last week on policy and the evolution of uncertainty noted the shift of responsibility for stimulus from monetary policy to fiscal policy, acknowledging that while ‘the RBA’s actions will provide important additional support, the scope for these policies to provide sufficient stimulus is limited and has necessitated the large levels of fiscal support both at the onset of the pandemic and in the Budget.’ He also characterised the nature of the fiscal response to date as the introduction of ‘temporary automatic stabilisers’ and suggested that one important cause for Australia’s productivity slowdown has been declining competition, citing Treasury estimates suggesting that ‘reduced competition can account for at least one-fifth of the slowdown in labour productivity growth in the private non-financial sector in Australia that occurred between the 2000s and the mid-2010s.’

The Parliamentary Budget Office (PBO) has released its September 2020 quarter assessment (pdf) of government finances. The PBO reports that the underlying cash balance for the period July 2020 to September 2020 was a deficit of $80.9 billion, well up on the September quarter 2019 deficit of $13.9 billion. Government expenses were $202.7 billion in Q3 this year, up from $125.8 billion in Q3:2019 (the PBO notes that the increase is more than annual Commonwealth spending on defence and Medicare combined). Revenue in the September quarter of 2020 was similar to that for the same period in 2019, while normally it would be higher. And net debt at the end of the quarter had risen to $580.8 billion, or almost $160 billion above its pre-pandemic level.

Two pieces from ASPI’s The Strategist blog on Australia-China trade. Michael Shoebridge argues that ‘the temporary but highly profitable China market boom for Australia’s commodity and services exports that has run since 2014 is ending—and probably pretty quickly.’ And David Uren estimates that ‘Australia has no realistic alternative market to China for a third of its exports and no viable source but China for almost a fifth of its imports.’

Grattan has published a new report on the cost blowouts associated with government ‘mega’ projects in the transport sector. According to the report, the past 20 years has seen Australian governments spent $34 billion more on transport infrastructure than they originally estimated. Big projects turn out to be particularly risky in this regard, with more than one third of overruns since 2001 due to just seven big projects.

The Centre for Public Integrity is pretty scathing about the Government’s Commonwealth Integrity Commission Bill.

The Fall 2020 edition of the excellent Journal of Economic Perspectives (JEP) is now available including a symposium on income and wealth inequality and another on economics and epidemiology. Timothy Taylor (editor of the JEP) takes a look at the latter here, asking what happened to those early estimates of very high death tolls.

Tyler Cowen lists his winners and losers from the US November elections. His winners include Californian libertarianism and drug decriminalisation, and his losers include money in politics and lockdowns.

Barry Eichengreen’s thoughts on what Joe Biden might learn from the 1932 Hoover-Roosevelt Presidential Transition.

Brookings updates its calculations of the US GDP split by vote. Back in 2016, Clinton-voting counties accounted for about 64 per cent of US GDP while Trump-voting counties accounted for 36 per cent. Its initial estimates for 2020 show Biden-voting countries with 70 per cent of US GDP with Trump-voting counties accounting for 29 per cent (based on unofficial results from 96 per cent of counties).

The Economist has an interesting piece on ‘problems with the plumbing’ in the world’s most important asset market – the US Treasury market. The essay points out that the market has now malfunctioned twice over the past year or so, a worrying sign given its centrality in the global financial system.

The IISS presents four scenarios looking at how COVID-19 could change the global political, economic and military balance of power over the next five years: Silver Linings imagines a world characterised by a swift economic recovery and a return to international cooperation; Downfall is based around a slow and incomplete economic recovery, domestic fragility and a fragmented international system characterised by a serious chance of Great Power war; Lost in Transition sees a relatively stable domestic political situation but international fragility; and Home Alone sees disrupted globalisation alongside increasing state fragility.

Our World in Data explores the discrepancy between US health spending and life expectancy outcomes.

A VoxEU column on the political consequences of COVID-19 claims that the early evidence suggests that governments that placed more weight on health outcomes versus short-term economic outcomes gained political support.

A World Economic Forum list of the top ten emerging technologies of 2020.

EY looks at how lessons from behavioural economics might help businesses reopen by deploying trust to combat disinformation, drawing on social norms to encourage good behaviour and utilising default settings to fight ‘behavioural fatigue.’

Another one from VoxEU, this time offering a survey of the evidence on capital taxation and arguing that while personal capital income, property, and corporate income should all be taxed, wealth should not be taxed and the case for taxing inheritances is ambiguous.

Russ Roberts of Econtalk has an entertaining conversation with Steven Levitt of Freakonomics fame.

Latest news

Already a member?

Login to view this content