For an organisation to pursue its purpose it must set clear goals and timeframes within which they are to be achieved and measure its progress in achieving them. The board must work with organisation’s staff, if any, to identify these goals, make resources available to achieve them and oversee the appropriate use of these resources.

Supporting Practices

6.1 The board oversees appropriate use of the organisation’s resources

6.2 The board approves an annual budget for the organisation

6.3 The board receives and considers measures which evaluate performance against the strategy

6.4 The board oversees the performance of the CEO

6.5 The board monitors the solvency of the organisation

Oversight of resources

Resources are the tools that organisations use to achieve their goals. Resources can generally be grouped under four categories:

- Financial (such as cash reserves, credit and investments);

- Physical (such as real estate, equipment and vehicles);

- Human (such as employees, volunteers and their skills); and

- Intellectual (such as copyrights, brands and data).

Directors have an important role to play in overseeing the proper use of these resources. The board must understand what resources the organisation has access to and make them available, with appropriate controls, for the achievement of the organisation’s goals.

NFPs have a special obligation under the law to only apply their resources for their purpose and not for the private benefit of the people involved with the organisation.

It is common for boards to oversee the development of policies that set out how resources must be properly used and maintained. For example, most boards will establish a policy about who can spend the organisation’s financial resources and under what circumstances they can be spent. It is common for organisations to establish policies concerning appropriate use of technology, management of intellectual property and human resources.

Beyond focusing on the appropriate use of resources, boards should also consider whether resources are being used efficiently. One of the key ways the board does this is through defining performance targets, often called key performance indicators (KPIs). These targets help the board to monitor progress against defined measures, which should be aligned to the organisation’s goals.

Budgeting

Budgeting is an important annual process that helps organisations to identify and plan for future needs, and to allocate resources accordingly. Budgets generally last for a 12-month period and are focused on forecasting revenue and expenses, though may include consideration of other resources and measures. It is common for management to develop the budget and for this to be approved by the board, but boards may take a more active role in this process in some circumstances.

The purpose of the budget is to align an organisation’s resources to its goals and to set parameters around how resources will be used across a year. For example, the board may authorise management to spend the organisation’s financial resources within the budget but may require approval for any expenditure outside the approved allocations or above a certain amount.

Boards will generally review the organisation’s performance against its budget at regular intervals using ‘management accounts.’ These are internal documents that track performance against the budget.

Measuring performance

For an organisation to know what it is doing and how its activities contribute to achieving its purpose, it must define and evaluate its performance against defined measures. There are a wide range of performance measures that are used across the NFP sector. Boards should select a mix of both financial and non-financial performance measures to help it develop a more complete picture of the organisation’s performance.

Generally, performance measures should be:

- Meaningful to the organisation;

- Capable of being measured and acted upon;

- Timely;

- Cost effective to produce;

- Comparable; and

- Simple (where possible).

One of the ways the board can align the work of the organisation to its purpose is through defining performance measures that support the organisation’s purpose. Defining and overseeing these measures enables the board to develop accountability – both in its reporting to external stakeholders and in holding management to account. This is discussed in greater detail in Principle 7: Transparency and Accountability.

Performance of the CEO

As part of providing oversight of the CEO, the board should define and evaluate performance measures for the CEO which are aligned to the organisation’s purpose and the strategy. This way the board can keep the CEO accountable for their performance. Generally, the CEO will use their own performance measures to inform the measures for other staff. This helps align the activities of everyone involved in the organisation with the purpose.

Boards should be careful in the development of these performance measures. People will naturally orient themselves to work towards meeting their performance targets (especially if there is an incentive for doing so) and so the form these measures take can significantly influence the way that the people in the organisation behave. This is discussed in greater detail in Principle 10: Culture.

The board should provide regular and honest feedback to the CEO on performance including the board’s expectations. The CEO also has a responsibility to keep the board informed about progress against performance measures by providing regular reports. This will help the board form an opinion about the CEO’s performance and inform the feedback they provide.

Financial information

Directors are required to read and understand financial information so they can play their part in monitoring the organisation’s financial health and performance. This is part of the duty of directors to act with care and diligence which is discussed in greater detail in Principle 2: Roles and responsibilities.

Importantly, every director has a responsibility to understand the organisation’s finances and to contribute to appropriate financial oversight. This is not the sole remit of the treasurer, nor can this responsibility be outsourced to an organisation’s accountants or external advisers.

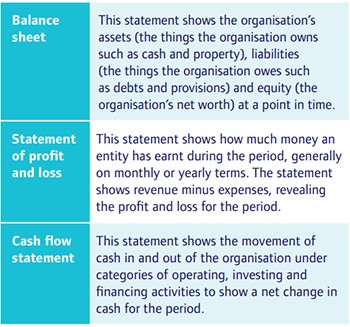

The board should work with management to determine how best to communicate information about the organisation’s financial position. Information produced for this purpose is referred to as ‘management accounts.’

Management accounts usually include the following three types of financial statements:

Figure 5: Types of financial statements

The numbers in these statements are intrinsically linked. Organisations can make use of accounting software that links the data in these statements to provide greater integrity in financial reporting, but directors should carefully review whether these statements are correct.

Together, these three financial reports present the overall picture of the organisation’s financial health at a point in time.

Where a financial report is presented to members and other stakeholders, laws and regulations may require them to be presented in accordance with Australian Accounting Standards.

Financial health

Evaluating the organisation’s financial health is an important part of the role of the board.

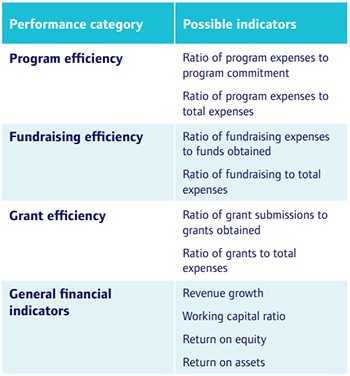

In doing so, the board must identify what the financial goals of the organisation are. This includes determining matters such as the required level of reserves, an appropriate diversity of revenue streams and the right asset mix to maintain. Boards will generally look closely at their budget, management accounts and financial reports to evaluate performance against these goals.

There are several standard indicators that organisations can use to assess financial performance:

Figure 6: Examples of financial performance measures

There is a perception among some NFPs that they should not set and achieve ambitious profit goals because this may be viewed poorly by stakeholders. However, aiming to achieve long-term financial sustainability should be a core goal of all organisations so that they can achieve their purpose now and into the future. This involves making smart financial decisions and aiming not only to get by, but to build and maintain financial strength.

Being an NFP does not mean that you cannot make a profit (sometimes called a ‘surplus’). NFPs can make a profit provided it is used to further its purpose.

While it is important to plan for financial strength, NFPs should not pursue profit at the expense of delivering their purpose or be perceived to be doing so by stakeholders. Boards play an important role in determining a financial vision for the organisation and communicating it to stakeholders.

For example, if an NFP is seeking donations while at the same time making a large profit so that it can pay for a new piece of equipment, it is important that this is understood by stakeholders. The board should make sure that the intention of their financial decisions is communicated to members so that they can understand how the organisation’s resources are being used to further the organisation’s purpose.

This also applies to an organisation’s reserves. Having adequate reserves is important to support financial health and can play an important role in managing risk. Determining the right level of reserves is a matter for the board and should include consideration of the organisation’s operational context (such as its operations, staffing, funding landscape, liabilities and the external market) to help assess current and future financial needs.

It is important that the board takes a considered approach to the management of its reserves. It is a good idea to develop a policy that sets out the board’s intentions around the maintenance and use of reserves. This policy can also help the board to communicate with stakeholders about how they are managing the organisation’s financial resources.

Monitoring solvency

Solvency refers to an organisation’s ability to pay its debts as and when they are due. This means that an organisation must have access to enough cash (or assets that can be quickly converted to cash) to pay for any debts it may have. Monitoring solvency is a key responsibility of each director.

One of the ways a board can do this is by monitoring the organisation’s cash flow. If more money is consistently going out than is coming in, this may be an indication that the organisation is heading towards insolvency. Estimating future cash flow needs and monitoring the working capital ratio (which shows the relative proportion of the organisation’s current assets to its current liabilities) can also provide insight into an organisation’s solvency. It is generally considered good practice for an NFP to have a working capital ratio of 1.5 or greater, meaning that current assets should be 1.5 times greater than current liabilities. Where this is not the case, this should be prompt inquries from directors.

Most organisations will be subject to legal requirements about being and remaining solvent. Directors may be personally liable for any debts incurred if an organisation continues to trade after it becomes insolvent.

Faced with the prospect of insolvency, many boards choose to shut up shop and call in an administrator or liquidator. However, directors may be able to rely on a ‘safe harbour’ defence if they begin a course of action that is reasonably likely to lead to a better outcome for the organisation than the appointment of an administrator or liquidator.

Insolvency is a complex and serious issue, and directors should take swift action if they are concerned that the organisation is, or may become, insolvent. Often this will include seeking expert, professional advice.

Non-financial performance

The performance of an NFP should not be evaluated in financial terms alone. To build a complete picture of an NFP’s performance, it is also important to use non-financial performance measures.

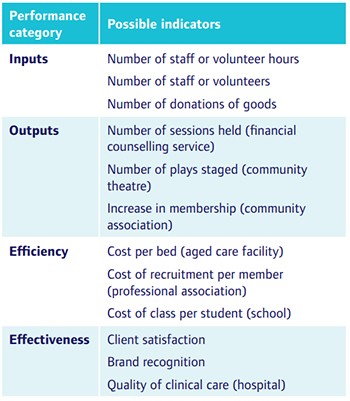

For example, an organisation established with the purpose of providing high-quality care and accommodation to older Australians cannot know whether it is achieving its purpose solely by looking at its profit for the year. It will be relevant to evaluate factors such as standards of clinical care and the health and wellbeing outcomes of clients. These are called non-financial performance measures.

There are several standard indicators that organisations can use to assess non-financial performance:

Figure 7: Examples of non-financial performance measures

Efficiency measures demonstrate how well an organisation turns its inputs (e.g. financial resources) into outputs (e.g. meals). For example, a soup kitchen can determine the efficiency of its operations by calculating the number of meals it provides and the total cost of providing them to work out the cost of each meal.

Effectiveness measures demonstrate how well an organisation is achieving its objectives. These measures can be more difficult to determine because they are generally not as easy to quantify and may involve more subjective judgement. For example, a school might evaluate its effectiveness based on how well students perform against standardised tests. These measures are sometimes referred to as ‘outcomes measures.’

In selecting non-financial performance measures, it is a good idea to consider a balance of efficiency and effectiveness measures to establish a more complete picture of performance.

Some organisations may have legal or contractual obligations to report on certain measures as part of funding, contractual, regulatory or accreditation requirements.

It is also important for organisations to assess how well they are performing against the expectations for their conduct (or behaviour) set by themselves and others such as government authorities, accreditation bodies and selfregulatory agencies. This is discussed in greater detail in Principle 9: Conduct and compliance.

Measuring impact

All NFPs exist for a purpose, but it can be challenging to evaluate precisely how well an NFP is working towards achieving its purpose. Some NFPs will have a purpose that is very difficult to evaluate such as eradicating poverty, or which may be ongoing such as cancer research.

Impact measurement refers to the process of evaluating how much change an organisation has achieved through its activities. For example, an organisation that provides employment services to deaf people might measure impact based on factors such as the workforce participation of their clients. To do this, an organisation might compare their clients against the broader workforce, against a control group of deaf people who are not their clients, or against the impact of their competitors.

Measuring impact is challenging and may require significant resources to do effectively. However, if possible, impact measurement is a valuable way to demonstrate an organisation’s success in achieving their purpose, and can be useful in attracting donations and funding.

Reporting to the board

For the board to monitor the organisation’s performance, and to make decisions that will help drive performance, they must have access to timely and relevant information. The main way this is achieved is through reporting to the board. Reports received by the board should be aligned to the strategy and include consideration of any defined performance measures.

The nature of this reporting will depend on the organisation’s circumstances. The board should work with management to establish a reporting framework that provides access to the information they need, when they need it and in an appropriate format.

While it is important this information is provided to the board, directors should also actively seek more information if required as part of their duty of care and diligence. This is discussed in greater detail in Principle 2: Roles and responsibilities.

Questions for Directors

- Is the board satisfied that the organisation's resources are protected from misuse?

- Is there an agreed definition of success for this organisation?

- How well is financial and non-financial performance evaluated?

- Do financial performance targets contribute to long-term organisational sustainability?

- How does the board use performance information in its decision making?

Case Studies

HelpfulCare

HelpfulCare has established a resource management framework that sets out how the organisation’s resources are to be used. As part of this they have developed specific policies around matters such as vehicle maintenance and acceptable use of technology

The board undertakes an annual budgeting process which sets ambitious targets for profit and growth. HelpfulCare uses a zero-based budgeting model through which all expenses are justified for each new period and a revised budget is developed at the half-year mark in response to changes in the operational environment.

As part of their strategic plan, HelpfulCare have identified five key strategic goals which are supported by a series of measures. The board receives regular reports from management on the organisation’s performance against these measures.

The board also receives regular financial reports which help them to monitor and reach an informed opinion on the organisation’s financial health – including its solvency. Financial reports are prepared by management and reviewed by the board.

The board sets short, medium and long-term objectives for the CEO which are defined in an annual performance agreement. The CEO receives an annual appraisal as part of a process lead by the chair and reports at quarterly intervals to the board against defined criteria.

The Friendlies

The Friendlies maintain an annual budget which is developed by the board with the assistance of the coordinator. The budget remains substantively the same each year but is adjusted based on new membership figures or to accommodate specific projects.

Within the budget, only the coordinator is authorised to spend money on behalf of the Friendlies. For expenditure outside the approved budget or above a certain amount, the coordinator is required to seek the authority of the board.

The Friendlies have a five-year strategic plan which includes key targets towards which the organisation is working including growing their membership and saving money for community projects. Reports against these targets are provided by the coordinator at all board meetings. The board also reviews standard management accounts produced by the Friendlies’ accounting software to consider how they are performing against their budget and to monitor solvency.

The coordinator’s goals are the same as the organisation’s strategic objectives. Every year the chair and two board members meet to review the coordinator’s performance and to provide feedback.

Latest news

Already a member?

Login to view this content