As the discussion around executive remuneration continues, leading directors discuss different approaches to incentivising, rewarding and retaining top teams. David Walker writes.

One of the big headaches for directors is deciding how to pay the people who run their companies. Pushed this way and that, boards are devoting “a huge amount of time” to the issue, says board remuneration consultant Michael Robinson MAICD of Guerdon Associates. “Boards spend a huge amount of time trying to get it right,” agrees John M Green FAICD, deputy chair of QBE.

The sheer quantum of pay often grabs the headlines, but it’s the mix that takes the most time — fixed versus variable, short-term versus long-term, cash versus equity, and more. There is no definitive evidence on what works. Robinson sees “a dearth of research” in the executive pay field. Researchers such as Professor Xavier Baeten of Belgium’s Vlerick Business School agree. Researchers in the field often fail to find a link between long-term company performance and high pay.

Many other stakeholders also focus on executive pay. The banking Royal Commission, Australian Prudential Regulation Authority (APRA), Australian Securities and Investments Commission (ASIC) and government attribute various social and corporate ills to high or misconfigured pay. “Remuneration both affects and reflects culture,” banking Royal Commissioner Kenneth Hayne AC said in his final report. He recommended all financial services entities should review at least annually the design and implementation of their remuneration systems for frontline staff to ensure they focus not only on what staff do, but also how they do it.

Most large investors want executives paid in a more transparent way, with pay linked to performance. Griffith Research polling suggests more than 75 per cent of Australians think most chief executives are simply overpaid. Yet many directors lack in-depth knowledge of human behavioural issues. So executive pay becomes “all about belief systems,” says Robinson. “Everyone has their particular beliefs about how pay should be delivered.”

An Australia Institute study published in 2018 found that while average earnings have less than doubled since 2000, NAB and CBA CEO pay more than tripled. Average CEO pay for the largest 100 Australian companies declined from $5.5m pre- global financial crisis (GFC) to $4.7m in 2011, but has since increased steadily back to $5.2m. Similarly, Australia’s highest reported CEO salary peaked pre-GFC at $33.5m, declined to $11.8m in 2011 before bouncing back to $21.6m in 2017.

The issue is global in nature. The High Pay Centre, a UK independent non-party think tank that focuses on pay at the top of the income scale, released new figures in August 2019 showing the median pay for UK chief executives fell by 13 per cent in 2017–18. However, the median CEO salary (£3.46m a year) is still more than 117 times that of the median UK full-time worker (£29,574). The High Pay Centre claims the fall in pay is likely to be due to a combination of factors including: the possibility of greater restraint on high pay and less money being awarded through long-term incentive plans (LTIP) due to variable corporate performance and the cyclical nature of payouts, which sees a temporary spike in CEO reward every few years.

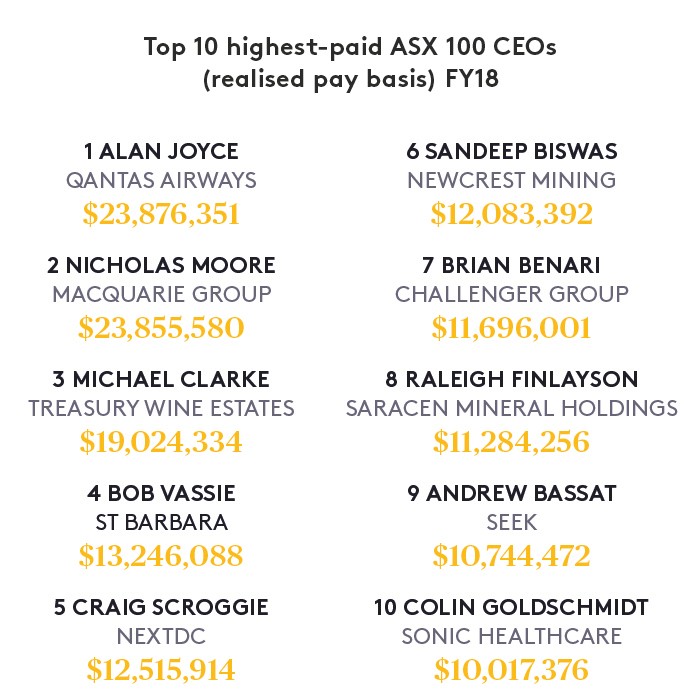

In FY18 the median ASX 100 CEO realised pay rose to $4.5m according to the Australian Council of Superannuation Investors (ACSI) — 68.5 times the average full-time annual earnings.

Formulas and rules

Robinson is one expert who believes that by varying pay with results, boards can wring better performance from their executives. Julius Caesar’s chief engineer received a share of Rome’s war profits, he says. “If you look at Elizabethan times, Francis Drake got a share of the bounty. Incentives have been in the pay systems for 2000 years.”

More boards are working at encouraging this. And the quest for a more appropriate executive pay formula has made some advances in the past four decades.

Pay first exploded in the 1980s and 1990s as company sizes ballooned and some academics argued executives needed better incentives to manage companies well. In an attempt to align the interests of managers and owners, stock options were placed in many packages. A rising share market then pushed up the value of the stocks. That made many executives richer than in any previous generation, and fuelled new public dissatisfaction on the issue.

After the 2008–09 GFC, executive pay entered another phase. Stung by claims that incentives had helped create the crisis, corporate boards around the world reined in pay rises, especially short-term incentives. Stock options fell from favour. Now that pay is rebounding in many parts of the world, from Bridge Street to Wall Street, the debate is growing more heated and more public.

The five goals of pay

For remuneration to influence behaviour, psychologist and remuneration adviser Michael Robinson cites five requirements — all of them psychological fundamentals known for at least 60 years.

- The subject must be able to exert control over the outcome

- The remuneration must be seen to be valuable

- The remuneration must be seen as achievable

- The outcome must be measurable

- Constant and regular feedback must be provided so people can adjust behaviour to reach that outcome

Ask whether an incentive plan ticks these five boxes, says Robinson, and the answer is that many don’t. For instance, pay based on comparing total shareholder returns with industry peers (relative TSR) will generally fail this test. Among other things, executives generally will not know what returns competitors are generating so cannot get feedback on their own relative performance.

Fenced in

As pay rebounds, despite conduct and compliance failures, many believe boards have not done enough to hold executives to account by adjusting down remuneration outcomes. “Our boards have dealt poorly over two decades with pay,” says Australian EY partner and executive pay specialist Rohan Connors. In the early 2000s, several high-profile pay misjudgements led to a requirement for companies to report top executives’ pay.

One result has been the regulation of executive pay. In 2004, after the HIH collapse, Australia’s government told public companies to start publicly reporting executive pay. That may have worsened the overpayment problem. Connors, like most observers of Australia’s approach to executive remuneration, believes that has fuelled an inflationary pay spiral in the country’s corner offices.

In 2011, Australia initiated a “two strikes” rule. If more than a quarter of shareholder votes were cast against a company’s remuneration report for two years in a row, shareholders vote on whether to spill the board. In 2018, Australia’s new Banking Executive Accountability Regime (BEAR) required bankers to have a proportion of their pay deferred.

Now, further constraints are being discussed. ACSI wants to see annual election of directors and a binding vote on pay every three years, says Ed John, its executive manager of governance, engagement and policy. The US and the UK have annual director elections, and the UK also has a binding vote on pay. Such policies make companies listen more carefully to their owners, he says.

ACSI would also like companies to disclose the ratio of a CEO’s pay to that of the company’s median worker. Management theorist Peter Drucker asserted that CEO pay should not exceed 20 times that of the average worker — anything more, he said, would “sap morale”. In the UK, the Labour Party’s Jeremy Corbyn would make 20:1 a legal maximum.

Responding to Hayne's final report, APRA is consulting on a new prudential standard on remuneration that includes prescriptive requirements (including a 50 per cent cap on the use of financial metrics in variable remuneration) — a significant step by the regulator and without precedent. Many experts expect that will also influence how other sectors pay Australian executives. Hayne also looked at the two strikes rule — seemingly acknowledging the problems it can pose for boards — but deemed formally making a review on it beyond his mandate.

Rise of long-term incentives

As executive pay has evolved, the biggest and most durable trend has been the rise of the LTIP. Even before the GFC, much of executive remuneration growth was in incentive-based pay. Today, LTIPs make up about half of executive pay in very large companies. In Australia, one company stands out: Macquarie Bank, which the Hayne Royal Commission noted paid a much higher proportion of variable remuneration than other banks.

“It’s clear to me that Macquarie's success has been hugely influential with regulators, including Hayne,” says Green.

LTIPs aim to give executives a better incentive than just salary, but also to reward a long-term mindset and avoid the quick gains of bonuses. They typically vest over several years, conditional on hitting targets, with downwards adjustments (even to zero) for poor risk outcomes. Many observers suggest that by encouraging long-term thinking, the right LTIP can stop finance executives making many of the mistakes that led to the GFC.

Other firms have moved more gradually towards LTIPs. A BDO report shows that even in the country’s largest companies, LTIPs are typically less than half of total pay. Concerns about the quantum of short-term pay have been reinforced by shareholder votes targeted at companies such as Westpac. Chair Lindsay Maxsted FAICD acknowledged that a 64 per cent vote against the bank’s remuneration report in late 2018 was probably triggered by the generosity of the company’s short-term variable pay for executives.

Getting the balance right

The rise of the LTIP has sparked yet another debate — this time over the right metrics for awarding them. Investors worldwide are increasingly keen for executives to be judged against clear metrics, rather than vague, non-financial criteria.

In Australia, that problem hit the Commonwealth Bank in 2016. The CBA board wanted executive LTIPs to reflect progress in improving diversity, inclusion, sustainability and culture. In the new LTIPs, total shareholder returns (TSR) governed just 50 per cent of the package. Investors rebelled. Just as Institutional Shareholder Services worried about JP Morgan CEO James Dimon’s vague metrics, CBA shareholders felt the proposed LTIPs lacked rigour, as well as being complex, opaque and too reliant on board discretion.

APPRA is leading a counter push for inclusion of more non-financial metrics — for example, addressing conduct and compliance, customer outcomes, reputation and alignment with strategy and values — in response to the banking Royal Commission. The proposal to cap financial metrics at 50 per cent in particular is controversial, given the perspectives of different stakeholders on the issue.

Guerdon’s Michael Robinson says APRA “has arguably gone too far and been too prescriptive on how an incentive plan should be designed”.

Green argues the sheer numbers of executives who will be covered risks encouraging people away from the sector.

Macquarie Business School’s Professor Elizabeth Sheedy says the mix of financial and non-financial measures “sounds all very plausible in theory”. But the non-financial metrics are so hard to measure well, she says, “you’re basically wasting your time”.

A clearer connection

EY’s Connors is one of many who wants boards to focus on building a clear connection between pay and performance. He wants boards to drive executive pay decisions from their purpose and strategies, and from customer interests, rather than obsessing about the expectations of outside stakeholders. He also worries that executives too often are rewarded for financial performance despite poor non-financial performance, as the Hayne Royal Commission and APRA’s inquiry into CBA both found. Providing high pay for high performance is easy — the hard part is cutting pay when executives underperform.

Andrew Fraser GAICD (above), the former Queensland treasurer now chairing Sunsuper, has been seeking a new CEO to replace the retiring Scott Hartley, whose final-year pay was a relatively modest (by Australian standards) $560,000.

Fraser’s key requirement is to align the new CEO's pay with members’ interests. He says it’s evident that properly designed incentive pay schemes help drive executive performance. Fraser says incentive pay regulations are already having effects. “Things like BEAR in the banking environment, which will very soon translate into other sectors in the financial services industry, are driving that behaviour,” he says. Sunsuper is “certainly moving to increase our deferral term and quantum”.

The pay changes are not all to executives’ benefit. Macquarie and some other companies have now added “malus” — the opposite of bonus — and clawback provisions to their packages. Malus clauses (now required by BEAR) let boards retract awards before they vest. Clawback, more problematically, lets entities sue for repayment even after the executive has pay or shares in hand, but often creates tricky employment law complexities. Given a boost by the GFC, these provisions aim to inhibit executives from making decisions for short-term gain where they might cause long-term carnage.

The doubts about incentives

Even the effectiveness of incentive pay is still up for debate. Frank Cooper AO FAICD (above) is a director at Woodside and South32. Like most directors, he wants well-designed schemes that clearly connect pay to performance, including long-term incentives. He says his boards work hard to identify “a model that will appropriately recognise, reward and challenge our executive teams for acting in the best interest of the company and delivering the best results they can”.

Cooper acknowledges the challenges involved in setting variable remuneration. Typically, he finds, a good executive team “rises above the data of the KPIs in the remuneration model and works in the best interests of the organisation”.

Surveys of executives indicate that sentiment is widely shared. In a 2012 PwC study, fewer than half the executives thought their LTIP was an effective incentive and most disliked the complex rules that increasingly govern their pay. Research also suggests that executives heavily discount LTIPs — Australian executives more than most. One executive told PwC, “I don't assign any value to my share allocations. I consider them in the same way as a company lottery ticket.”

Indeed, when Cooper has asked executives whether they work any harder for variable pay, the answer has been no. The one exception, says Cooper, was a not-for-profit CEO who said his team did work more effectively because of variable remuneration. The pay made them focus on the areas where he wanted focus, he said. Then Cooper asked if that might be because the CEO had finally communicated his needs clearly. “He couldn’t answer that question,” he recalls.

As far as short-term incentives (STI) go, Cooper says much of the market does not understand that a portion of most STIs will be paid simply for delivering against expectations, with more paid for outperformance.

“That is often described as getting paid to come into work and then just delivering against what's expected of you,” he says. “A number of people seem to have the perspective that any STI is intended to be for outperformance.” He also says there is “a very strong argument that the size of STIs should be significantly reduced”.

Should fixed pay rise?

Cooper would like to see the balance shift back to fixed pay — a move he says has support from many executives and some directors.

Research backs these doubts about incentives. Xavier Baeten says that in Belgium bigger firms pay more, but LTIPs are not changing performance. Long-term outperformers “pay their executives relatively less, which proves that a lot of directors are wrong when they assume you have to pay top level”. Outperforming firms also pay a lower proportion of variable pay, he adds, and have a lower difference between target and maximum bonus. Kym Sheehan, a senior lecturer in law at the University of Sydney, also warns that in most circumstances, pay’s biggest effect may be to create perverse incentives. “It’s not so much about trying to get it right,” she suggests, “but about trying to get it not wrong.”

At worst, the proliferation of mechanisms within pay packages can be a device for obscuring pay. But boards continue to hope that pay can help them get more out of executive teams. With investors and regulators keen for LTIPs, those mechanisms will almost certainly grow more popular. Baeten’s research suggests that LTIPs actually breed better stakeholder relationships — and most boards want happy shareholders.

Case studies: Macquarie Bank

John M Green FAICD, a former Macquarie Bank executive, now deputy chair at QBE, believes Macquarie’s packages are particularly well structured. The bank aims to align employees with the business through grants of stock and Macquarie fund units, but executives’ units and stock are locked for a period of up to seven years. It awards its own performance share units to executives, and they take four years to fully vest.

Such a system means Macquarie executives “are actually very long-term focused,” says Green. “They say, ‘Wow, I want to make a short-term profit and get a bonus this year, but I’m going to hold this stock for seven years, and that means I need to make sure things don’t go wrong. So I’m not going to make super-short-term decisions that will visit back in a negative way next year, or the next year, or the next year.’”

Seek

Unlike many companies, Seek doesn’t have short-term incentives for its executives. Instead, the organisation only has a long-term incentive structure based on the company’s absolute share-price rather than the more common measure of total shareholder return.

The straightforward approach to remuneration was adopted in 2013 and has caused concern for some proxy advisers. However, Seek chair Graham Goldsmith FAICD says some proxy advisers rely on formulaic models that don’t take account of history or particular circumstances.

Seek does not try to drive culture with its remuneration system, in part because cultural measures are often built into short-term incentives. “We are very focused on, and rely on, the performance management process generally to ensure the right culture and the actions are being taken — rather than [focusing] specifically on remuneration,” says Goldsmith. “The remuneration system is set up to come up with appropriate rewards for continuing to advance the company. It’s very focused on the long term and on trying to align the team with the outcomes with shareholders’ experience.”

This is in contrast to Goldsmith's view in the banking Royal Commission report, in which he drew a close link between remuneration and conduct. “It’s incumbent on companies to take a step back and try to work out what is the right structure for that company, given what their strategy is and given what they are trying to achieve as a company,” said Goldsmith.

By Christopher Niesche

Latest news

Already a member?

Login to view this content