Belligerent behaviour from the White House might take up most of the bandwidth, but the steady rise of China proceeds apace in the background.

When surveying recent international developments, it has been hard to look past the US. Since the 2024 US election, the Trump administration’s efforts to break and then remake the global order have monopolised global headlines. From April 2025’s “Liberation Day” assault on the world trading system to this February’s Supreme Court decision striking down many of those same tariffs, to the disruption of the global security order delivered by the activation of the “Donroe Doctrine” in Venezuela, the Greenland furore, and then the outbreak of war with Iran, Washington’s actions have been dictating the pace of global events. But for all the sound and fury, the US is far from the only big story Australia needs to watch.

Consider, for example, the world’s other superpower. China was one of the few countries able to stare down Washington’s tariff threats. By weaponising its overwhelming role in the production of critical minerals, Beijing forced an effective truce in the trade war at the Busan summit last October. Since then, a run of Western leaders have made the pilgrimage to Zhongnanhai (Chinese Communist Party headquarters) in search of closer economic ties. Another sign of expanding international influence has been 2025’s record US$213.5b spending on the Belt and Road initiative.

Meanwhile, China is now the world’s renewable energy superpower. Chinese firms supply more than 90 per cent of the world’s solar panels and dominate batteries, electric vehicles and wind turbines. US firms may be setting the pace in AI, but their closest competitors are Chinese companies like DeepSeek, Alibaba and Moonshot.

Granted, it’s not all positive news. On some metrics, China’s economy navigated 2025’s trade turmoil in decent shape. A record trade surplus of nearly US$1.2 trillion and a real GDP growth rate of five per cent demonstrated Beijing’s resilience in the face of US pressure. But external strength was mirrored by internal weakness.

Chinese policymakers still struggle to manage the protracted downturn in the domestic property sector. The toxic fallout from “involution” — the hyper-competition, excess capacity and deflationary pressures that are the flip side of the country’s export engine — continues to distort domestic and international economics. Then there is the opacity of political developments in Beijing, which remain an ongoing source of uncertainty. Not all of January’s drama came from Washington. The same month saw the culmination of the most sweeping purge in the history of the People’s Liberation Army.

Trade ties that bind

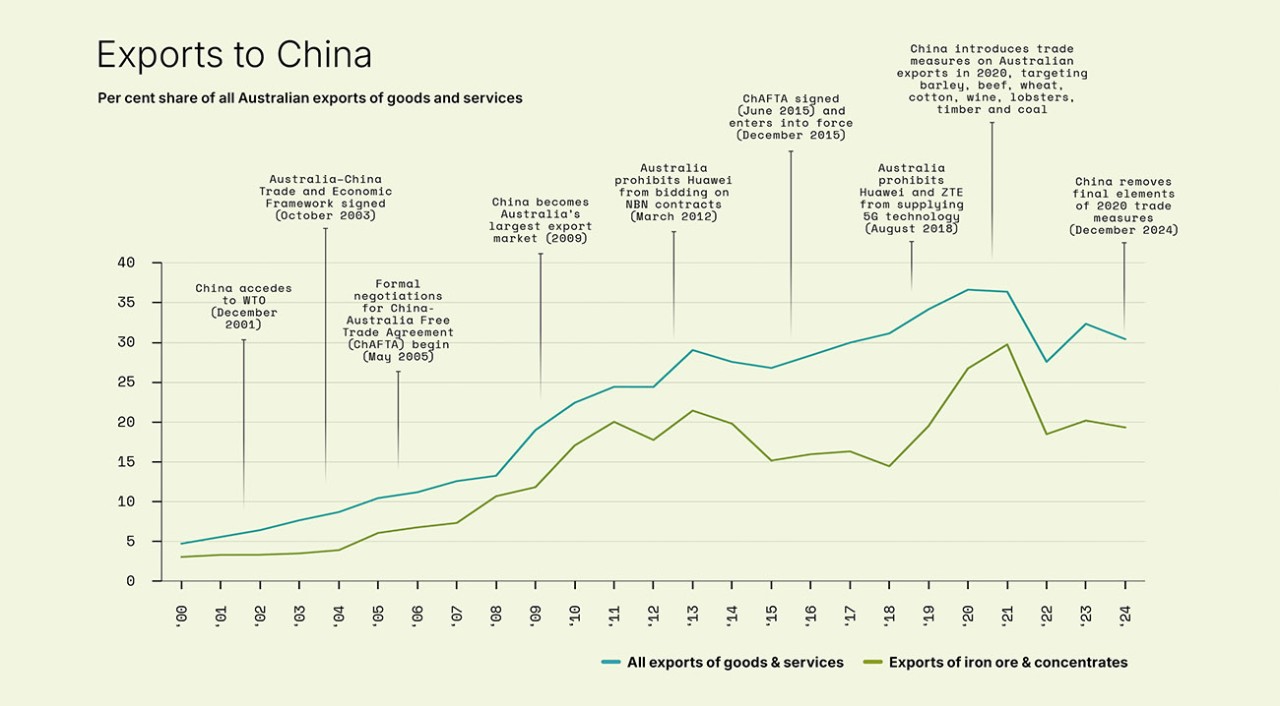

There is, then, plenty to track for Australian policymakers and businesses. Indeed, Beijing gave Canberra a not-so-subtle reminder in February last year, when it sent its navy south to circumnavigate Australia. Live fire exercises in the Tasman Sea aside, there are sound economic reasons for paying attention, not least China’s status as our largest trading partner.

As of 2024, two-way trade was worth almost $312b, comprising 25 per cent of total trade. China’s relative importance as an export market was even greater, accounting for over 30 per cent of Australia’s exports of goods and services. China’s import dominance isn’t as great, but it is still our largest supplier, accounting for more than $115b of goods and services, approaching 19 per cent of the total.

We know Beijing is willing to treat this trade relationship as geo-economic leverage. When China demonstrated its displeasure with Australia’s political leadership in 2020, it rolled out punitive measures from tariffs and quotas to de facto bans targeting Australian exports, including beef, barley, wheat, cotton, wine, lobsters, timber and coal.

Many of those exports proved resilient, partly because some exporters found alternative markets. The timing also proved fortuitous, as events like the post-pandemic rebound in global activity and the Russian invasion of Ukraine lifted commodity prices, boosting Australia’s terms of trade. So, this was a largely unsuccessful example of economic coercion. Even so, according to the Productivity Commission, “some businesses paid a heavy price”. It wasn’t until December 2024 that Beijing finally removed the last of its measures.

Geo-economics and geopolitics remain prominent in the bilateral relationship. Four current examples stand out.

Bones of contention

First, since last year, some of Australia’s big iron ore exporters have been locked in combative talks with the China Mineral Resources Group (CMRG), now the most powerful buyer in the global iron ore market. Along with pressing for lower, more stable prices, CMRG wants more trade to be priced in yuan. Export bans have reportedly been deployed as a policy tool, albeit on a small scale. Looming in the background are China’s investments in Guinea’s Simandou mine, the “Pilbara killer”.

Secondly, Australia’s efforts to develop a greater domestic critical minerals capability have been both complicated and enabled by China, which has simultaneously been a key customer, a strategic market actor in squeezing out potential competition, and a spur for other countries to invest in an Australian-based diversification play. Hence, the US-Australia deal last October, before the Trump-Xi meeting in Busan.

Then there is the ramped-up competition for influence in the South Pacific, where Canberra’s moves have included 2024 treaties with Tuvalu and Nauru, and last October’s security “Pukpuk Treaty” with PNG, all aimed at giving Australia effective veto rights over future deals with Beijing.

Finally, the Port of Darwin, over which China’s Landbridge Group secured a 99-year lease in 2015 from the NT government. raising concerns from Australian security agencies and the US. During the 2025 election campaign, Labor and the Coalition pledged to return the asset to Australian control, but in January, the Chinese ambassador warned a forced sale would have adverse consequences for the relationship.

This article first appeared under the title 'We need to think about China' in the April/May 2026 Issue of Company Director Magazine.

Latest news

Already a member?

Login to view this content